A Mad August Appears: "AI Hype" Tested, Asian Correlations Examined

A quick summary of my commentary on Fortune, Bloomberg and others.

It’s been a messy, messy week in markets and the inbox had been a-buzzing. Late in Friday, journalist Paolo Confini and I had a chat on market sentiments about AI and semiconductor stocks, portions of which featured in his article in Fortune magazine. Read it here. Then, in the middle of this week, Journalists Abhishek Vishnoi and Winnie Hsu from Bloomberg had questions about Asian markets far in excess of the fall in U.S. markets. Check out their article here. For the full background behind my commentary in these two articles, read on!

UPDATE: Zoltan Vardai over at CoinTelegraph also included my commentary in an article published three days after this article went live. Click here to read his article.

In the midst of a “lackluster” Q2 earnings season wherein major corporations were showing mixed results in terms of “Full-Year Trends”, tech stocks — primarily led by megacaps — began to slip down. Over the past year, tech megacaps had promised that a sum total estimate of over a trillion dollars would be committed over a period of 5-7 years towards the buildout of datacentres for AI-relevant applications. When considering the total processing capacity being touted, this is orders of magnitude greater than the current capacity of the global internet which is arguably still not close to full utilization.

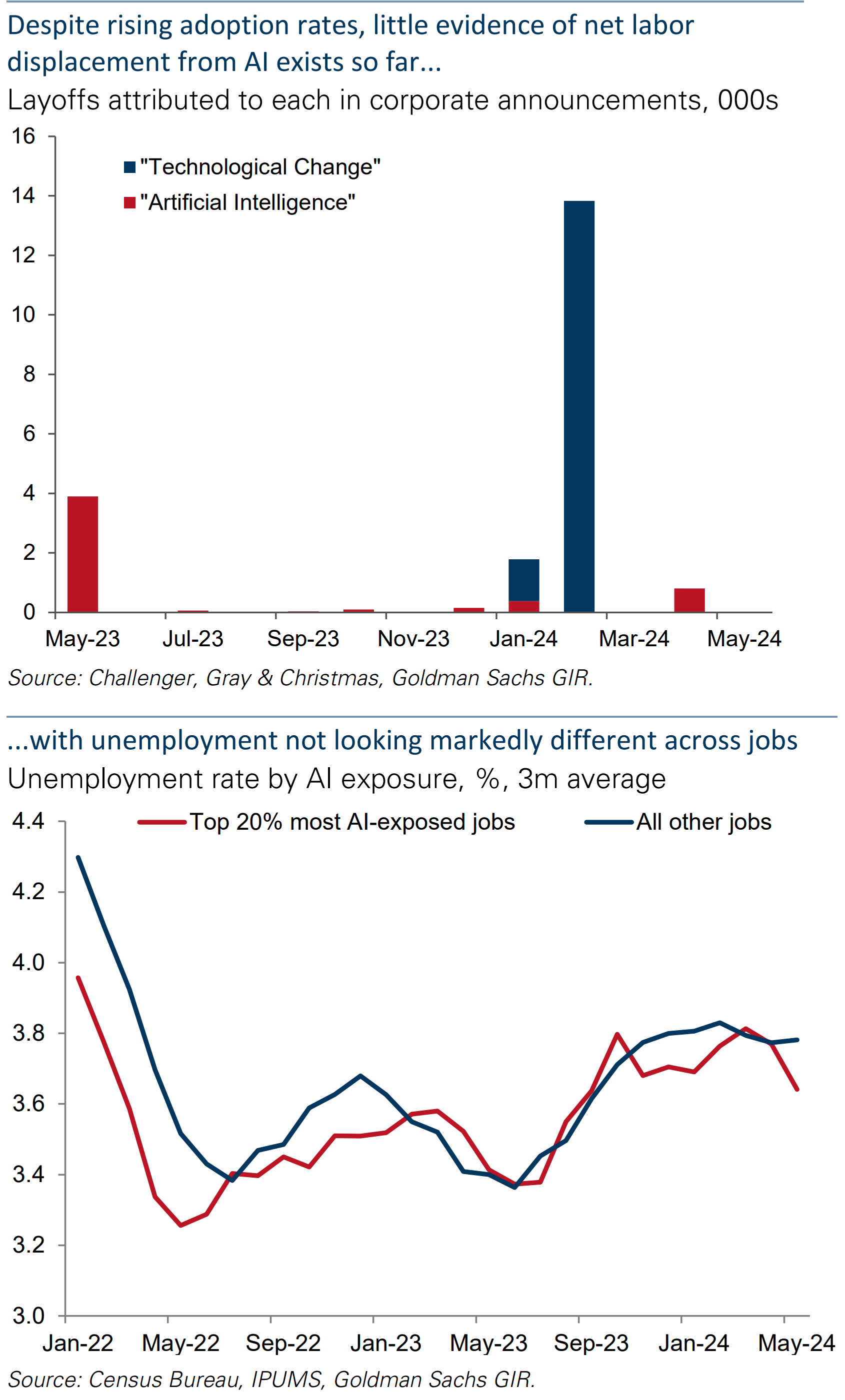

Growth investors wholly bought into the transformative hype of AI in that it would reduce the net cost of human labour required and foster a whole host of new services. Overall, outside some ostensibly higher adoption in certain industries, a little under 5% of all firms in the U.S. (for example) have adopted AI.

Even in the businesses ripest for AI substitution such as data processing or financial services, the sum total of human labour substitutions is very small.

On the generative AI front, learning models are unable to be transformative enough to enable the substitution of human-driven ingenuity for the machine-based. In economic terms, the cost of the infrastructure ostensibly required to substitute an average human worker will work out to be much, much higher than simply continuing to retain said worker.

This common-sense realization is only now beginning to sink into the investor space as FOMO (“Fear Of Missing Out”, for the uninitiated) peters out and economic considerations are being examined.

Note #1: This was covered in some detail in my article about TSMC’s earnings published on SeekingAlpha, the Tiger Brokers Community platform as well as on the Leverage Shares website.

Across the entire pack of leading semiconductor companies, Nvidia and Arm held the highest forward-looking valuations on account of their catalogue of high-performance supercomputing-level hardware designs. While Nvidia held the pole position in terms of demand versus available supply, Arm was deemed the closest competitor in terms of product complexity. If datacentre spends are rationalized going forward, these would be the most vulnerable, with Arm worse for wear since it doesn’t hold as massive a market share as Nvidia.

However, there is scope for corporate datacentre spends to be rationalized as hardware burns out with continuous usage and need to be swapped out. AMD’s products are generally cheaper and employ a balance of hardware and software optimization to meet computing demands. While datacentre spend reduction would be a concern, given that 46% of revenue in H1 was from datacentres (unlike Nvidia’s 87% as of Q1, which is likely to increase by Q2), it is still diversified enough.

Note #2: The risks for global chipmakers was the subject of a Substack article penned in June. AMD’s Q2 earnings was also covered in articles published on SeekingAlpha, the Tiger Brokers Community platform as well as on the Leverage Shares website.

TSMC is quite vulnerable in the event that datacentre spends trail off since it is the foundry of choice for Nvidia, AMD, Apple and (now) Elon Musk’s Dojo. However, CEO C.C. Wei was quite coy in the company’s recent earnings call on the matter of expanding production facilities in the face of increased demand. This prudence will likely work out in TSMC’s favour since expenses won’t spiral out of control in the event of a crash in datacentre spend on a forward-looking basis.

Outside of Nvidia, Arm and possibly AMD, the rest of the semiconductor sector is relatively reasonably valued in terms of price ratios. These three stocks are vulnerable in that order to substantial price ratio corrections in the mid- to long-term. The rest of the semiconductor sector have a potential downside of a 15-20% PE ratio correction over the next one year, which is relatively modest compared to that in Nvidia and Arm.

The semiconductor sector, as a whole, is a strategically sensitive matter to many countries on account of a concentration of design and manufacturing facilities in a handful of locations. China has long been at work on creating a domestic chipmaking industry with relatively modest success while India is showing promising signs of success in a domestic buildout, which is being supporting by strong incentives. Over a long-term basis, current valuations are varyingly overblown.

The biggest sign of an uptrend would be manifest if tech megacaps would commit further resources to continue building datacentres rather than stock repurchases to prop up their own valuations. Given the need to drive up stock valuations by repurchases and the possible cooling of datacentre demand, this is somewhat unlikely to happen. If PE Ratios reach the 15-20 level, there is scope for a 5-10% “ratio band” forming on top of them within any Fiscal Year going forward. As of now, the sector is overvalued and therefore subject to very high volatility.

On the 1st of August, the S&P 500 and the tech-heavy Nasdaq-100 closed 1.37% and 2.44% down respectively from the previous day, as markets largely reacted to official reports that the number of unemployment benefit seekers in the U.S. was far higher than expected. The 1st of August was also the day when Amazon released its Q2 earnings after markets closed. On that morning, the stock was at $190.32. Exactly 24 hours later, the stock dropped 18% to $161.26 before closing the day at $167.90, i.e. down 13.35% from the previous day’s close.

However, this massive drop wasn’t necessarily due to market conditions: while early trends for the full year indicated that AWS would grow roughly by the same rate as it did in the previous full year (i.e. 2023), the “business of buying and selling” seemed to be in doldrums, with its much-vaunted advertising services segment — which was to compete with Meta Platforms and Google — trending to be grow by an sixth of what it did in 2023 while expenses trended at par with the previous year.

Note #3: Amazon’s Q2 earnings was covered in detail in articles published on SeekingAlpha, the Tiger Brokers Community platform as well as on the Leverage Shares website.

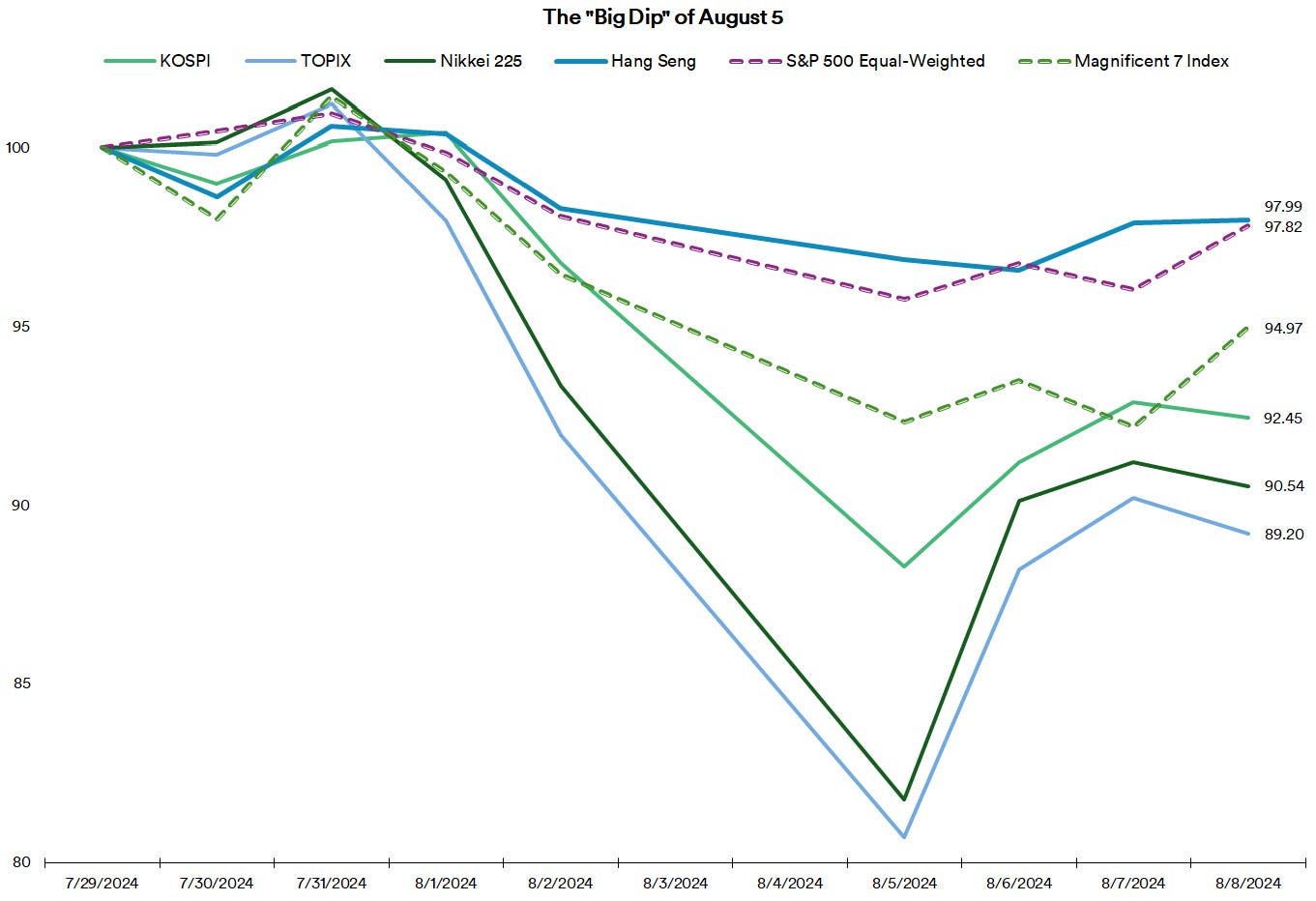

As the U.S. market slipped, so did Asian markets all the way till the “Big Dip” on the 5th of August. While markets have clawed back some of the losses as of the 8th of August, they’re still to return to end of July levels.

(Who knows, maybe they’ll do so by the end of the 9th, which is a Friday, and then lose it all again next week?)

When considering the S&P 500 Equal Weighted Index versus the Bloomberg Magnificent Seven Index, its clear that the fall and recovery of the market (as recorded by the market cap-weighted S&P 500) is predominantly being dictated by Big Tech and the Magnificent Seven. The nearly identical trajectories indicates a scramble mostly by institutions leading the majority of market participants.

Asian fund managers that are particularly high on U.S. stocks or Asian stocks of companies with a high connection to U.S. supply chain dependence will be scrambling to pare/redistribute their exposure. A series of vehicles that gave heightened exposure to Korean and Taiwanese stocks that were tapped into US supply chains have been popular for years now. This year, Japanese stocks were also being incrementally favoured on account of the yen's decline making for cheaper exports. With high-consumption societies such as Korea, Taiwan, the U.S. and Western Europe drawing down volumes and the Bank of Japan working on boosting the yen, more losses on account of unwinding overvaluation are virtually a given.

It bears noting that the vast majority of high-performance funds in Asia were far from secular: to mimic the US’ long-running tech story, many popular Asia-focused funds were substantially exposed to tech stocks and even commingled them with US tech stocks to make the funds more compelling propositions. When highly-weighted fund constituents that are also overvalued decline, the fund will have to scramble to cover their exposure. Tech funds with a high non-secular concentration of Taiwanese, Korean and Chinese/Hong Kong tech stocks are particularly vulnerable.

On the other hand, secular and regionally-weighted broad market funds will be less risky. However, there will be some "bloodletting" since Asian tech has been running at price ratio premiums for quite a while now. On that note, Warren Buffett’s Berkshire Hathaway further reducing its stake in Apple — with its previous round of “Apple-cutting” later translating to a higher stake in insurance companies and energy firms — is a classic move: financial services and energy have always been "recession favourites".

Outside of China — wherein financials are highly exposed to the moribund real estate sector — there will be a rotation out of tech and into regional energy and financials. Of course, for those asset managers who have long touted effective tech stock picking experience as their USP (“unique selling proposition”), this will not be an easy turnaround.

Note #4: Berkshire Hathaway’s first round of “Apple-cutting” was examined all the way back in May and was correctly called out as a “macro play” and not, as Mr. Buffett hinted, as being done to pay taxes. The analysis was published on SeekingAlpha, the Tiger Brokers Community platform as well as on the Leverage Shares website.

Postscript: And now we have news that Google has been found guilty of throttling the then-nascent search industry and a gigantic multi-year/decade illegal monopoly. What would this lead to? More on this next time, maybe.

China, Asia, India, markets, macroeconomics and much, much, more has been covered in the history of this Substack. For a list of all articles ever published, click here.