Adani vs Market Manipulators: Lessons for Korea from India

On July 23, I supplied some commentary to “Chosun Ilbo” (조선일보, lit. ‘Korea Daily Newspaper’) - South Korea’s oldest daily newspaper of record with a total circulation of over 5 million readers (digital and print) - in the wake of a number of product launches by my firm. Among other topics, I discussed Korea’s ongoing short-selling ban and drew some parallels with the recent actions on Adani’s stock, which India’s market regulator is investigating. Here is my commentary, with some updated data and expansions.

How do you evaluate the Korean stock market?

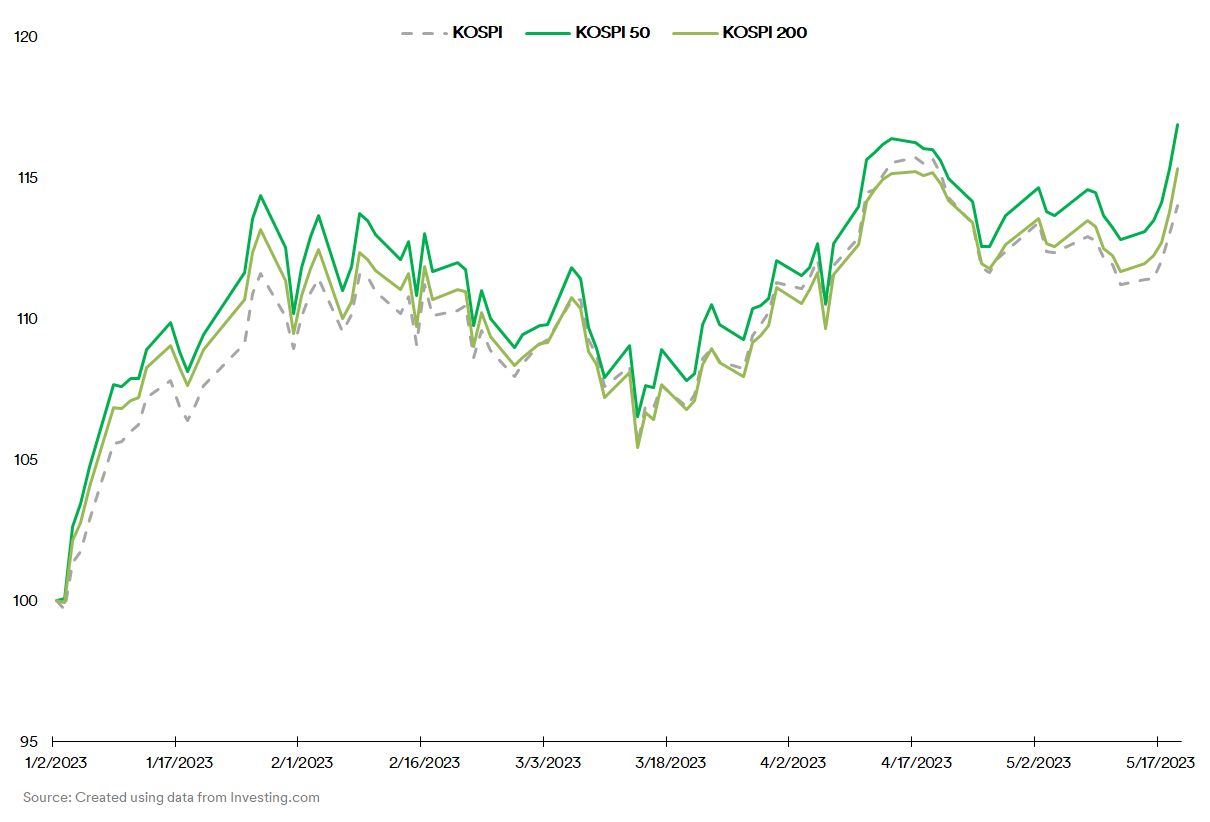

The Korean market is a very interesting study. The KOSPI (which represents the total market) is up 14% in the YTD till May 19. In the same period, the KOSPI 50 (which represents the 50 largest Korean stocks) is up nearly 17% while KOSPI 200 (which represents the small and midcap segments) is up 15%.

Meanwhile, the U.S.’ S&P 500 is up 9%, the S&P 400 (Midcap) is up nearly 2% while the S&P 600 (Smallcap) is down almost 1% for the same period.

The U.S. market, in light of macroeconomic factors, is logical in that the market imputes a higher survivability to bigger companies than the ones that are smaller. For example: within the S&P 500, the FAANG+ basket, which could be constructed out of 10 top tech companies in equal proportions, is up nearly 52%. The overwhelming consensus is that global tech giants are far too entrenched and ubiquitous to be easily replaceable and hence more robust in survivability.

The aforementioned macroeconomic factors are both local and global; they have far-reaching consequences, given how the Western Hemisphere is the prime consumer of goods and services in the world. If consumption falters in the West falters, it affects the world’s top companies as well.

While top Korean companies have a global footprint, they’re also heavily reliant on Western consumption. There should be a more pronounced variation in performance in the large-, mid- and small-cap segments. The present market performance can be attributed to a number of inter-related reasons:

Firstly, many fund managers proclaimed “global diversification” in their portfolio predominantly filled with U.S. tickers by simply buying a preponderance of Chinese stocks (and a handful of top-performing stocks from other Emerging Markets companies). As tensions between the U.S. and China increase, they are now being compelled to expend resources in identifying targets to achieve a truer form of diversification: Korean stocks are an easy beneficiary on account of Korean companies’ brand recall.

Secondly, a substantial amount of activity has been seen in the ETF space, wherein a rule-based approach is followed in portfolio construction. This distributes buying activity across the segment as opposed to a particular set of stocks. This is also attractive to foreign fund managers: buying a set of Korean ETFs would meet “global diversification” requirements handily.

Third, the prohibition of short-selling in Korean markets – the world’s longest ban of its type – skews market trajectories in light of the aforementioned two reasons.

How do you view the situation in the Korean stock market where short selling is prohibited?

The short-selling prohibition severely inhibits “price discovery”. This is a key phenomenon that fills in the periods between earnings reports and other substantial events or disclosures. In a nutshell, if an investor deems a stock to be overvalued, they will adopt a short position. If more investors agree, the short holder’s position is validated and they ultimately emerge the winner. If more investors don’t, the holder loses. Most short sellers don’t make money most of the time. However, their perspective is important; at times, they can be the voice of reason in the market. Negotiation is an observable and prominent cornerstone of modern commerce, after all.

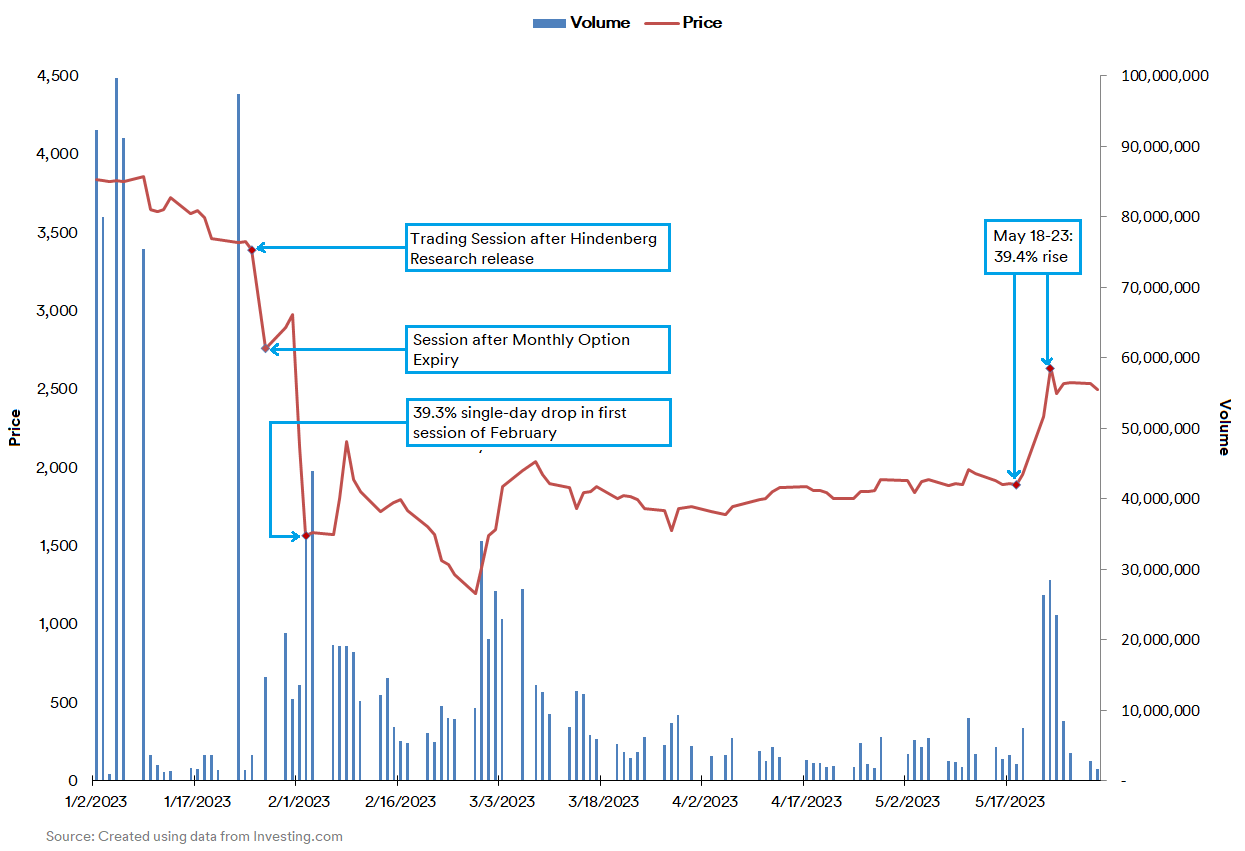

On the other hand, unfettered short-selling in a globally-connected market can throw a curveball to this principle. For a prime example of this: we need to look to India. On May 22, the Indian conglomerate Adani Group’s stock (NSE: ADEL) rose 19% in a single day, with all other Group entities rising massively as well. The stock was embattled after an adverse report by Hindenberg Research, a U.S.-based stock seller who claimed that the company’s cash flows and business structure were fraudulent. Adani had originally responded that Hindenberg’s allegations were already presented as facts in its disclosure prior to its listing and that the allegations on the cash flows were severely misrepresented. Nonetheless, as soon as the Hindenberg report was released, the company’s various stocks took a precipitous nosedive and lost over $100 billion in value.

Market regulator SEBI and Adani both approached India’s foremost legal authority – the Supreme Court – to adjudicate on whether the former failed in regulating the market and whether the latter misrepresented facts. The Supreme Court-appointed committee saw no regulatory failure by SEBI on May 20.

The committee also noted that the Hindenberg report used data available in the public domain to form misleading inferences. The short seller had disclosed that it itself held short positions in Adani companies and non-Indian-traded derivatives. This disclosure, in itself, is a complicated matter since Indian laws forbids the short selling of domestic stocks outside of the country unless they’re listed on an exchange. Thus, Hindenberg’s position was made via Structured Product Derivatives (SPDs) wherein clients in tax havens that are habitually unresponsive to foreign regulators are constructed by large foreign brokers whose associates register as Foreign Portfolio Investors (FPIs) in India and then hedge their bets via local brokerages. The purpose of the law is to make the party behind such a position apparent to the regulator and to leave a clear trail of inquiry if needed. In this case, SEBI asserts that a “Bear Cartel” led by 6 entities (including 4 FPIs), a corporate body and an individual – and which potentially includes 13 overseas entities who received contributions from 42 other entities in seven jurisdictions unresponsive to the regulator’s inquiries – targeted Adani’s shares just days ahead of the publication of the Hindenburg report and then squared off their positions with a huge profit amidst the panic. The regulator has asked for the Supreme Court’s permission to extend its investigation into the identity of these entities and subsequent legal action. The Court has granted time till August 14.

If the regulator’s investigation has merit, it will be likely that the Indian government will apply diplomatic pressure on non-responsive jurisdictions. The availability of SPDs was made possible by an amendment of the law in 2018 which required that brokers collect information on the ultimate beneficiary of any transaction by a foreign entity. In theory, absent manipulative actions, this would have been (and has provably been) a net benefit to principled investors eager to enter the Indian market.

In reality – if or when the regulator and its various allied investigative units uncover the identities of the “Bear Cartel” – it also opened the door to predators who exploited the sentiments of low-information market players via a mechanism originally meant to enable price discovery for their personal profit. The fact that Hindenberg – a well-regarded short seller who had exposed the likes of electric carmaker Nikola in the past with telling effect – could have potentially leveraged its reputation with no real merit in its arguments for the sake of filling its coffers or for the benefit of parties as yet unknown shows that no institution is sacrosanct. Institutions are people and people are fallible.

Ordinarily, in the days of high-information human traders shouting out quotes in an exchange’s trading pits, it would have been impossible for Adani’s stock to have such a sustained rout. Such a narrative would have been dismissed within a day or two. With electronic trading, trades were manually entered in a matter of seconds. With algorithmic trading systems, trades were entered in tens of milliseconds. Now, with AI/machine learning techniques framing decision-making with a degree of autonomy, the potential for routs increase even further.

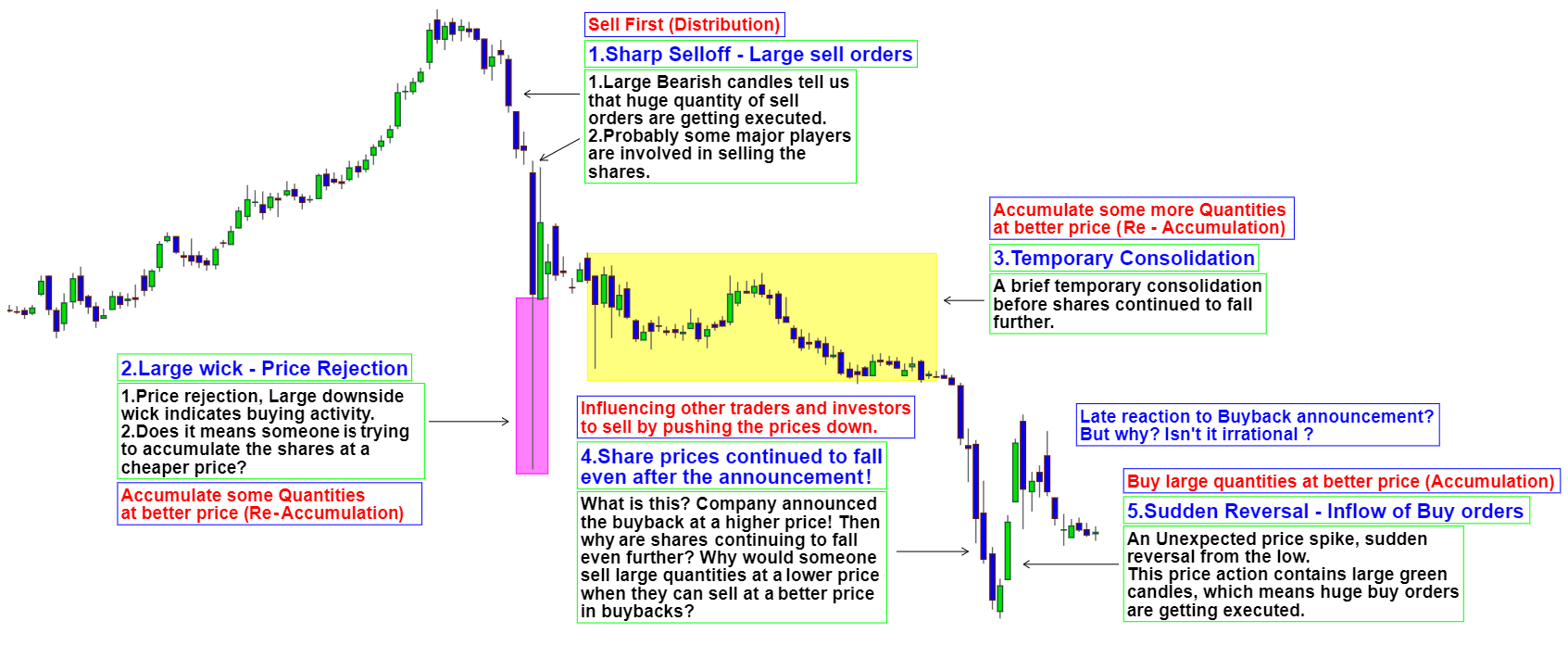

Assume a stock with a bullish outlook in its mid- to long-term trajectory is priced at X at this moment. Absent any new information, an “unprincipled” short-seller imputes a price of A (A < X) on the stock. If the short-seller does this enough number of times, trend-capturing algorithms (TCAs) begin to impute the possibility that the price is supposed to be close to A and starts to sell. Other TCAs, following the data feed, follow suit. Soon, the stock’s price is at B (B < A). At this point, the “unprincipled” short-seller buys into the stock. The stock ends the day at C. If (C – B) > (X – A), the short-seller has returned to their original position at a profit. But it’s now very likely that C < X. Either the same short-seller or another repeats the same set of actions the next day and the day after. The future trajectory of the stock is now substantially altered.

In the YTD till May 19, the NIFTY 50 (representing the “Large Cap”) was essentially flat. The NIFTY MidCap 150 was up about 2%, and the NIFTY SmallCap 100 was up about 1%. Fuelled by a strong rise in domestic consumption, lowering poverty rates, rising global trade, increasing competitiveness of its enterprises in the global arena and enhanced geopolitical status, various macroeconomic forecasts had already established near the close of 2022 that India will have the highest economic growth relative to virtually every other nation for at least the next two years. Given the correlation between macroeconomics and historical market dynamics, the YTD figures are highly suspect.

As it turns out, many experts have hypothesized that algorithmic systems have a higher net involvement in the Indian stock market than in the U.S. stock markets, where institutional investors with mid- to long-term portfolios and retail investors with high convictions have held sway. If one were to conjoin the Indian regulators’ investigations into “unprincipled players” with this high-tech trading dynamic, this would help shape the regulators’ convictions even further. While domestic retail and institutional investors have been strongly bullish on the Indian stock market, nearly every single trading session sees a prevailing bearish sentiment prevalent for portions of the time, following which stock trajectories show signs of recovery.

Here again, SEBI has been proving to be far more innovative in regulatory ruminations than its counterparts in the West. For almost a decade now, the regulator has drafted annual “Consultative Papers” wherein it invites market players to contribute towards its considerations on the question of “algos”. Over the years, it has involved from considering restricting time intervals between and price limits for algorithmic trades to reviewing each and every algorithm before being allowed to run. In more recent times, it has evolved to considerations of a move that is simultaneously audacious and innovative: “ring-fencing” all algorithmic activity away from regular electronic/human-driven trading activity. While this means that potentially each instrument could have two prices at any given time, it arguably deters algorithmic fallout from “unprincipled” players, as possibly seen in Adani’s case.

Unlike in science fiction, algorithms aren’t necessarily evil. In reality, its effects are shaped by its user, much the same way as a hammer wasn’t designed to be a weapon. If it can happen to India, it can happen to Korea. In fact, in the event that India shuts out “unprincipled” algo plays altogether and given rising investor interest in Korea, it could be a given that such attention will intensify in Korea.

The solution isn’t to melt all hammers, as is the case presently. Instead, one should observe the action of those who wield them. Prescriptive measures are necessary to ensure its fair usage. In this regard, it would likely be very useful if Korean and Indian regulators ruminate together and lend each other their respective competencies to arrive at the optimum measure for the modern age.

Do you think inverse products for single stocks offer individuals the same investment opportunities as short selling?

Inverse products, especially when traded on the exchange, offers investors numerous benefits. The first is that exchange-traded products tend to be cheaper than the underlying. The second is that holding an exchange-traded product doesn’t require margin maintenance. The third is that losses are limited to invested amounts only, unlike with holding a short position.

It could be argued by some that the downside is the paying of fees which are “baked” into the product. However, given that they offer substantial benefits and make short-selling more widely available to a greater swathe of investors, it could be argued that the fees are a small price to pay to be able to participate in one’s convictions. Given that these products have to stay competitive relative to shorts themselves, it’s almost a given that the fees will in fact remain small.

Do you have any advice for retail investors in Korea?

Technology is both ally and adversary. It’s relatively easy to set up news alerts to receive updates about one’s chosen stocks. At the same time, it’s also very easy to receive low-quality information. Therefore, discernment is key. Brokerage apps coupled with high conviction, the patience to sift through data and demanding a high level of quality from sources providing information can bring great benefits. It’s also important to stay informed and involved in framing one’s convictions. If done well, these steps have substantial scope for securing one’s financial future.