America's Banking Crisis Runs Deep

"It's sort of like having kids. Either they all are special or none are special."

On May 3rd, I had a conversation with MarketWatch about the special assistance being rendered to depositors at collapsing regional banks. I contended the crisis is neither transitory nor a panic. While key elements of my stance could be found in the MarketWatch article (also available here on Morningstar), here is the background for my arguments. I typically don’t post twice in a day but these observations are rather timely.

On March 15th of this year, as Silicon Valley Bank (SVB) folded, I offered the following thoughts to MarketWatch (also available here on Morningstar):

The SVB crisis unearths concerns about the reported book value for banks since U.S. institutions are the dominant holders of U.S. debt. In addition to "older" bonds issued earlier being built at near-zero interest rates, they're now also (provably) not very marketable. Thus, the reported MTM ("Mark to Market") value that, in turn, shapes the banks' book value is entirely suspect. So many questions can be raised on incurred cost of capital for investments delivering near-zero returns, resource allocation in light of long-term trends of inflation making rate hikes a tangible probability, investment management's ability to foresee adverse events, and so forth.

Pretty much every bank holding U.S. debt faces both the valuation conundrum and these questions. It's a system-wide issue that should - ideally - be addressed via appropriate levels of markdowns. The current situation's a warning that there's no such thing as free money. Sooner or later, someone's gotta pay.

A little under two months later, despite many market commentators stating that the crisis is over, First Republic Bank - a major regional bank - has folded, despite being given $30 billion in deposits by a conglomerate of 11 major banks.

First Republic Bank's failure can be attributable to two factors. The first factor was that the bank was built on the back of large loans made to residential properties. A substantial proportion of these loans were made at a time when real estate prices were heavily bullish. However, given that real estate prices have been tumbling across most of America and the loans themselves were made at discounted rates, these kinds of loans will be a millstone for nearly anyone to offload. It isn’t a coincidence that JPMorgan’s acquisition of First Republic comes with a loss-share agreement with the Federal Deposit Insurance Corporation (FDIC) that covers some home mortgages and business loans. First Republic's “loan problem” is now going to be JPMorgan's problem, despite the loss-share agreement. While JPMorgan arguably has a more diversified (but not entirely risk-free) debt portfolio, pretty much every existing real estate loan being serviced can be considered a loss to some degree in paper terms.

Commercial real estate isn't a very attractive portfolio either, given high national average vacancy rates. Some high-value locations hitherto deemed to be “in demand” had reached nearly 50% in the first week of April.

Over the past couple of years, regional banks have emerged as major holders of Commercial Real Estate (CRE) debt.

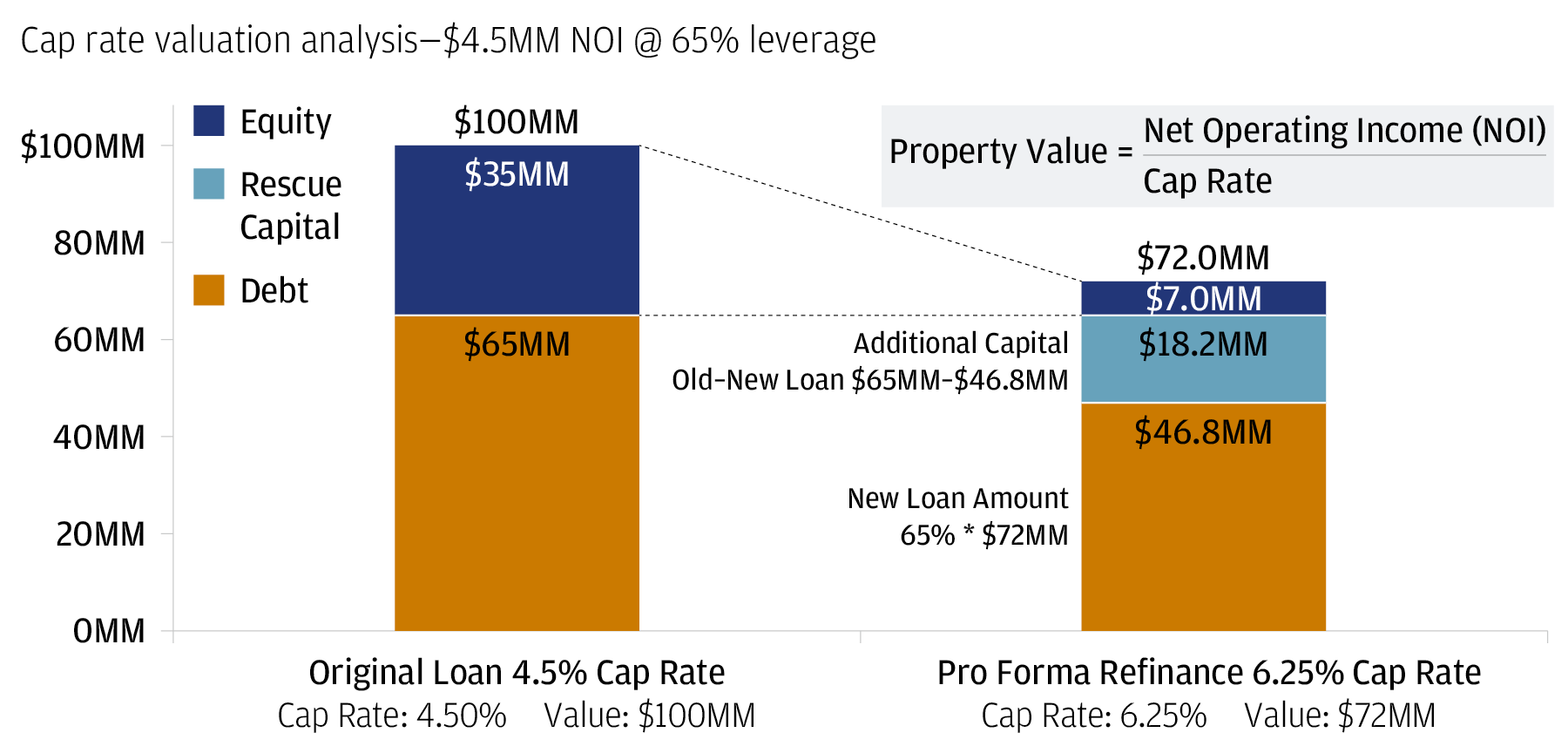

JP Morgan itself has highlighted the stress on CRE due to rates via the commercial property’s capitalization rate (or cap rate) - which measures a property’s net operating income (NOI), revenue less operating expenses, divided by its market value. The value of a hypothetical $100 million office building would decline to $72 million if cap rates were to increase from 4.5% to 6.25% (despite holding NOI constant). Therefore, if a borrower were to seek refinancing of the loan at this lower valuation while keeping the loan-to-value ratio constant, the borrower would have to contribute an additional $18 million in equity to obtain refinancing.

It isn’t entirely coincidental that the stock price of Valley National Bank - a large holder of CRE debt - dropped by as much as 15% on the 1st of May. Analyst consensus will likely continue to shift bearish as the impact of lower occupancy and rising refinancing costs ratchets up pressure on developers.

The second factor is that government-backed debt, especially long-dated debt, is nearly unmarketable now. Almost every bank stocked up on long-dated debt since it meets Basel III requirements on additional capital against the cash they set aside for trading and other "risky" activities. A cash deposit made in a customer account isn't necessarily enough so banks bought into government debt, with a preference for long-dated over near-dated. In paper terms, the pre-hike portion of the debt portfolio will now marked at increasing levels of net losses, given that the Fed rate hike cycle will result in higher yields in the Treasury's near-continual issuances.

As early as 2014, regional banks had protested that Basel III reforms hurt their businesses by increasing capital holding requirements on the loans and mortgages they hold in their books. At the same time, while a list of “Systemically Important Banks” (SIBs) for the U.S. wasn’t explicitly made, it was made implicitly by the Federal Reserve System. While the stress tests involved for this implicit qualification are more rigorous, it also brings with it a host of implicit guarantees for protection.

This implicit designation has created a two-tier systems that biases SIBs as effectively being more “survivable” than regional banks (most, if not all of whom, aren’t deemed to be SIBs). As a matter of course, SIBs have emerged with better deposit ratios. Meanwhile, the hometown banks of ordinary Americans had to resort to several perks and other forms of risky behaviour to stay afloat.

On average, regional banks' deposits represent ordinary Americans rather than all Americans. SIBs on average tend to hold the monies of high net-worth customers in greater amounts than regional banks at a time when 57% of Americans in 2023 are estimated to be unable to afford a $1,000 emergency expense. Considering the fact that this metric was variously estimated to be:

it could be extrapolated that regional banks’ deposits have been rather tenuous for a very long time.

Shortly after my conversation with MarketWatch’s Joy Wiltermuth, Federal Reserve Chairman Jerome Powell stated that the U.S. banking system is "sound and resilient" and the worst of the crisis is over. Meanwhile, the stock price of Beverly Hills-based PacWest - another regional bank with a strong California footprint - plunged 60% in extended trading while management huddled to discuss strategic options, including a sale. Much like SVB, PacWest’s differentiator was its high levels of “venture debt”. Ordinarily, this debt would pay off when ventures go public, raise capital, pay off their existing debt and/or establish a revolving line of credit for future activities. In 2023, the IPO pipeline is rather threadbare:

while the median late-stage deal size has fallen below median mid-stage size:

With 18 of the past past 20 tech IPOs now underwater, deal valuations are now deemed more risky than ever before:

First Republic's government debt problem is the entire sector’s problem. While SVB’s deposits shrank, the bank attempted to sell a portion of its U.S. Treasury portfolio to shore itself up. After several attempts, the bank managed to sell its bond portfolio with a book value of $23.97 billion at a $1.8 billion loss to Goldman Sachs. At the end of 2022, Bank of America held $3 trillion worth of debt securities, which was represented at a value of $862 billion. The bank had to record $114 billion as “unrealized losses” in its bond portfolio. Wells Fargo recorded $41 billion; JP Morgan recorded $36 billion and so forth.

Given that SIBs have significantly greater wherewithal to avail market-based “risky” activities (and the potential upsides), the residential/commercial/personal debt problem weighs heavier on regional banks. One way of shoring up this problem would be if the Federal Reserve were to reverse direction on rate hikes. However, if the Federal Reserve were to start cutting rates, inflation will regain momentum while the U.S. government prepares to spend well beyond its revenue stream yet again.

The two-tier system of denoting systemic importance creates a substantial “risk/reward skew”: SIBs - or larger institutions - receive an implicit reward by virtue of higher protection (and lower scenario risk). Regional banks are penalized due to their relatively diminutive stature; neither Basel III requirements nor Federal Reserve policy offer a carve-outs for those left behind to access opportunities for building out (or even maintain) growth and asset value without undertaking risky practices.

While the “depositor’s bailout” in excess of the FDIC limit of $250,000 ostensibly rescues the depositor, it transfers greater costs onto the entire system which will weigh heavier on regional banks’ revenues than SIBs. Thus, it’s highly likely that the financial sector will emerge from this crisis significantly less diverse than it is now: SIBs and a very small sliver of regional banks will emerge as the only survivors. As a result, the depositor will have access to far fewer venues to negotiate with and parley for their economic well-being in the future.

Over the long run, is the current course of action a good idea? While it does save a certain tranche of depositor, the lack of outcry or rumination over consequences for market, sector and customer seems to indicate all worries are being cast aside or (at best) being relegated into the future where it will likely be deemed the “new normal”.