Chinese Homebuyers in the U.S. To Increase in Volume and Value

Chinese Homebuyers in the U.S. To Increase in Volume and Value

With an uncertain domestic economy, a large proportion of Chinese investments overseas in real estate aren't estimated to be "investments"

Towards the end of September, a senior reporter from Fox Business asked for my thoughts on any possible trends in Chinese real estate investments in the U.S. Overall, foreign buyer purchasing activity is a small fraction of total real estate transactions. I also had a conversation with Robert Bowman at SupplyChainBrain (SCB) about the Chinese economy. While it’s unknown (as of now) if my commentary will feature in a Fox publication, Chinese buyers’ trends are quite interesting in and of itself and interlinked to my commentary in SCB, which is published here (with a portion also ending up in Canada-based Baystreet). Read on!

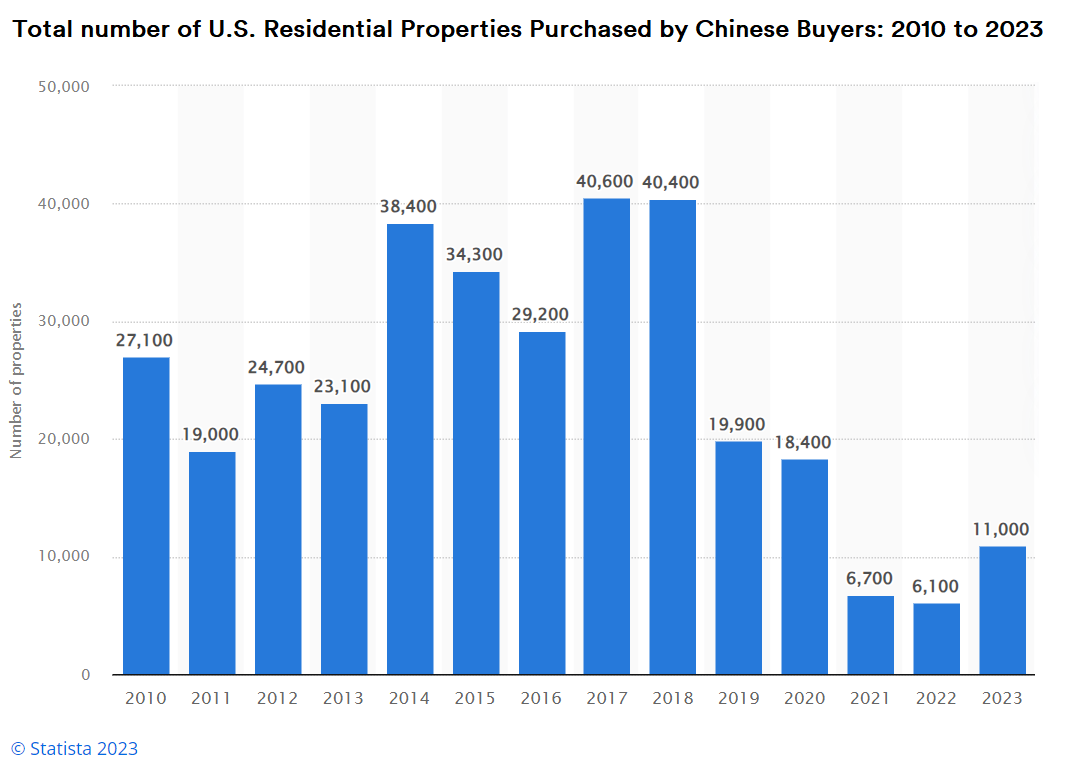

As of August, the number of U.S. properties purchased by Chinese buyers is down almost 70% relative to calendar years 2017 and 2018 (from 40,000+ to 11,000+).

Purchase volumes in 2021 and 2022 were a little over a seventh of 2017/2018 highs and is generally attributed to travel restrictions, possibly since Chinese buyers tend to scout for properties prior to purchase. For the current year, trends don't indicate that the purchase volumes will be brought up to par with pre-pandemic levels in Q4 for the calendar year. However, there are indications that there will be an uptick over the next 12 months.

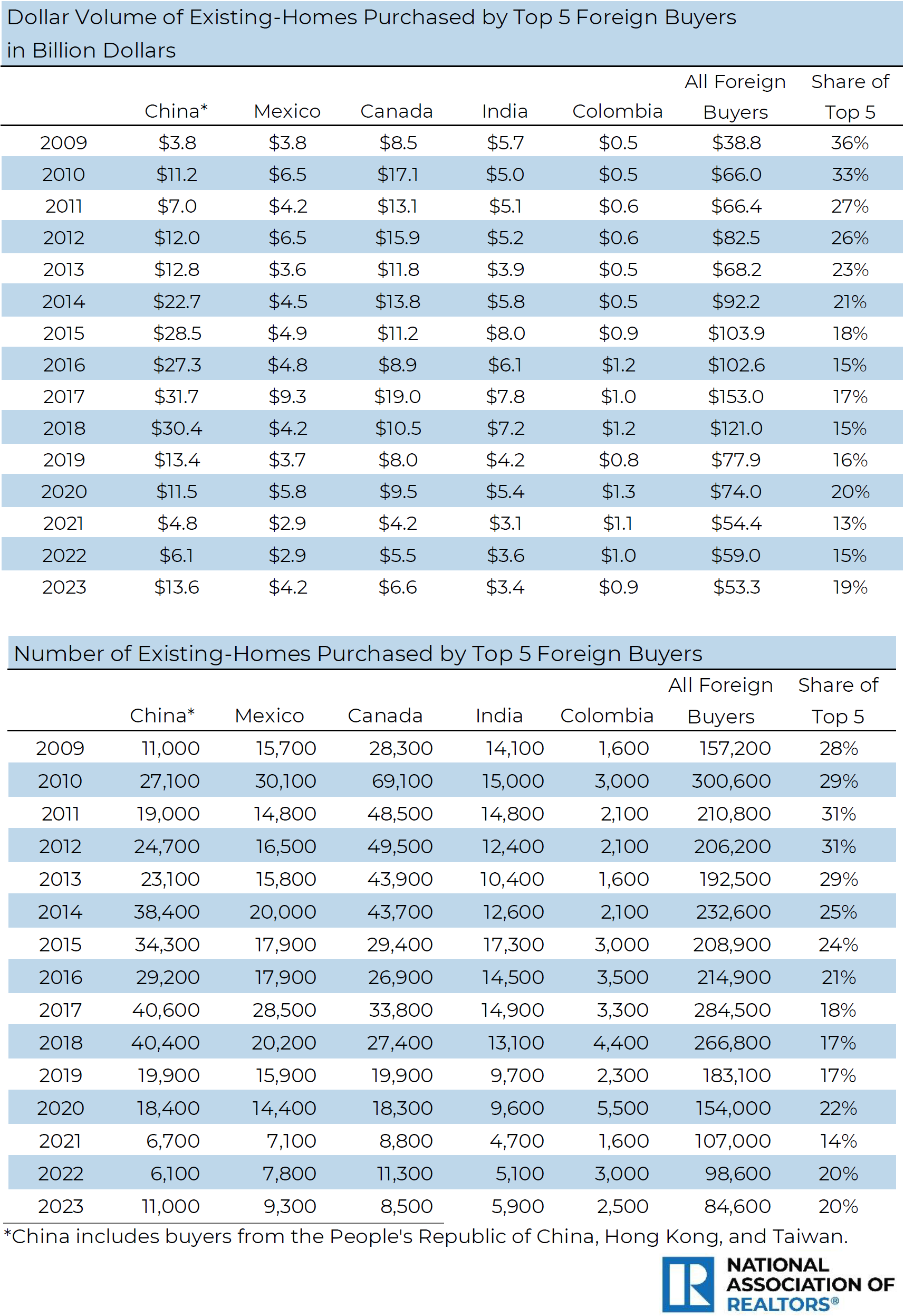

Chinese purchasing trends in the U.S. tend to lie higher on the spectrum: in the year ending March 2023, about 49% of foreign buyers were non-residents; the rest were visa holders or recent immigrants. Chinese and Mexican citizens accounted for 13% and 11% of all foreign buyers respectively

However, the average spend by Chinese buyers was a staggering 174% greater than that of the average Mexican buyer and 115% greater than that of the average Indian buyer (who account for 7% of all foreign buyers).

The trends are highly suggestive that non-residents are the primary driver of Chinese trends: the average Chinese and Indian visa holder/immigrant tend to buy at par with each other as they typically work in similar occupations.

Overall, California has been unseated as the top destination for foreign buyers. Over the past couple of years till the present, the top destination has been Florida with California and Texas now running neck-and-neck. Chinese buyers — on the other hand — remain fixated on California (33%), with 16% buying in Florida, 8% in Texas and 6% in New York.

The median spend by Chinese buyers is almost double that of an American buyer and predominantly in the form of a holiday home or primary residence. However, only about a tenth of the purchase volume can be considered as an “investment purchase”, which is another massive shift in trend over the past decade. Given that the bulk of the purchasing trends are in California where property values remain elevated despite a net resident outflow, this purchase preference mostly explains the disparity in average/median purchase prices between Chinese, Mexican and Indian buyers.

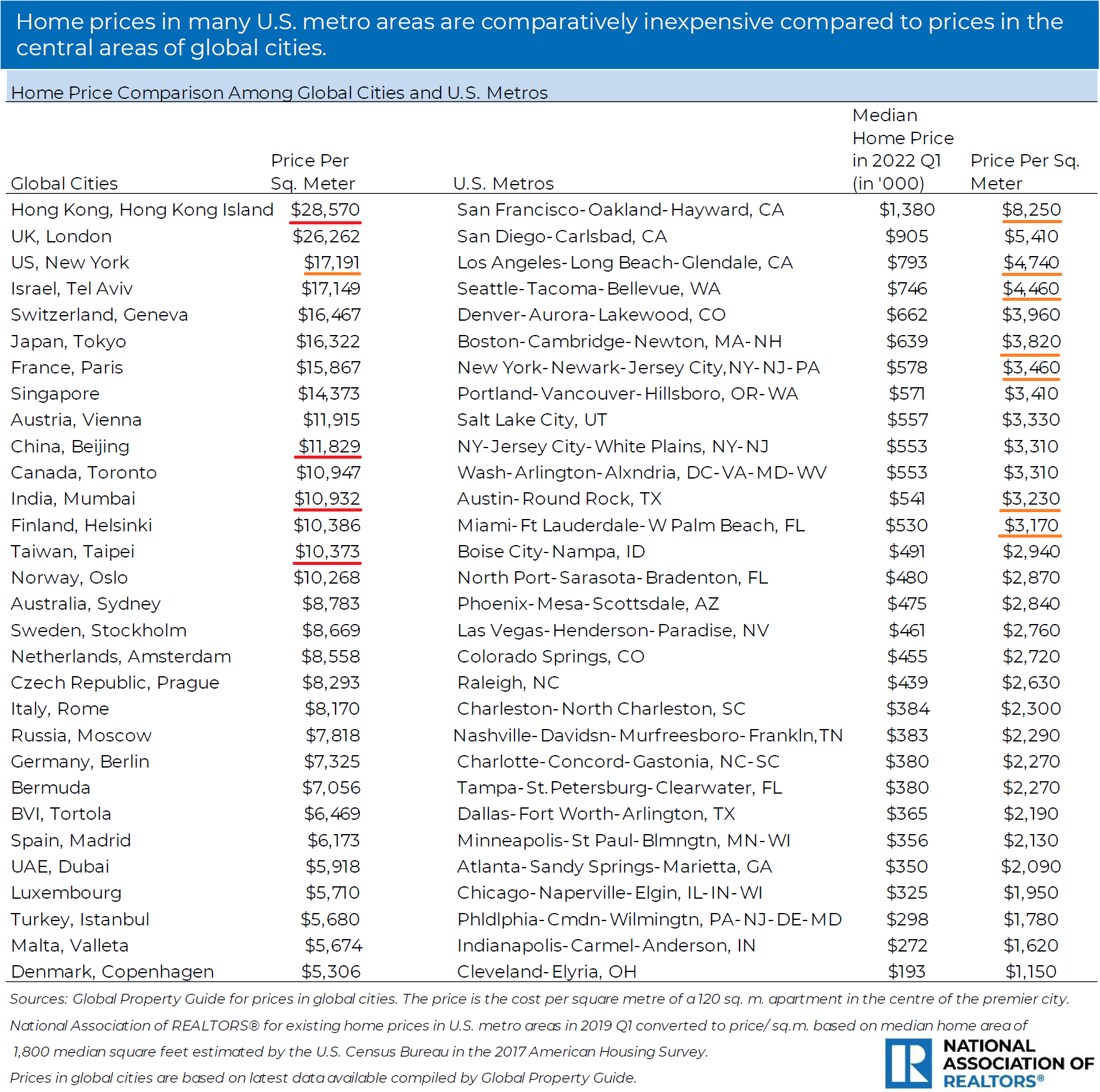

In addition, various reports suggest that Hong Kongers have been queueing up to either depart or diversify from their home base. U.S. property prices have certainly been attractive for wealthy buyers: the average price (per square meter) in Beijing (and Mumbai, for that matter) runs nearly on par with San Francisco and nearly twice that of New York but Hong Kong (and even London, for that matter) is 3.5 times that of San Francisco. Therefore, a primary home buy (with the possibility of long-term residency being secured eventually) has been an attractive option for non-resident “creamy layer” buyers from both mainland China and Hong Kong.

To sum up: Chinese visa holders/recent immigrants tend to be buying in U.S. cities proximate to their work but non-resident Chinese buyers tend to be buying in regions of historical significance for the Chinese diaspora (such as California). The average price in their region of preference biases overall trends but it could also be observed that the property "quality" generally tends to be higher — which suggests a “creamy layer” of buyers are making purchases to establish themselves in the U.S. over doubling/tripling down in (say) Beijing, Shanghai or Hong Kong. As it stands, the average price of a home in most “prime” American cities is lower than that in “prime” cities elsewhere —even in China and India.

Now, while “ultra-high-net-worth” Chinese citizens might be looking to cost-effectively close deals on large spreads in “prime” territories, “affluent” citizens from China (a catch-all term for subsequent tiers of wealth till the “salaried middle-class” tier) have been turning away from the domestic real estate market as well. As the commentary proffered to Nikkei Business Asia in September indicated, prices for new housing, secondhand listings, rent and land in China’s Top 100 cities — except for Beijing, Shanghai and Shenzhen — have been bearish throughout the year, including at the present.

“Affluent” Chinese citizens are increasingly turning away from real estate investments and now pursuing other means of wealth preservation overseas while navigating numerous curbs by Beijing. Up to $50 billion in cash per month — which nearly matches the trade surpluses China has with its trading partners — have been moved out of the country by households and private-sector companies for much of the year. The resulting downward pressure on the renminbi (人民币) helps sustain Chinese exports in turn. While the government has banned overseas investments in hotels, malls et al, “affluent” citizens are instead — as per the New York Times on the 28th of November — buying the likes of gold bars (which trades for a higher price in the mainland than in Hong Kong), apartments in Tokyo (with an intention to rent out and then secure investment visas for buyers’ families to move in), and insurance products in Hong Kong that resemble certificates of deposits while also figuring out circuitous ways of converting “renminbi assets” to “dollar-adjacent” assets.

If sufficient volumes of dollars are accrued and/or a pipeline of sorts established to ensure a steady conversion of domestic assets to U.S. dollars, it can be assumed that a number of “affluent” Chinese citizens will continue establishing themselves in major American cities and beyond via the purchase of homes. At this point, it’s uncertain if these purchases can be deemed as “investments” or “catastrophe planning”.

Both China and India have been covered a number of times in the current year. Click here for a list of all articles ever published.

For a “Big Read” on other matters, the ever-popular “Dharma” series traces the evolution of Eastern faith and philosophy. Here’s Part 1, Part 2, Part 3, Part 4 and Part 5, followed by the ancillary Part 6 and Part 7 discussing Malaysia’s and Indonesia’s spiritual history.