Countdown to EV Industry Consolidation

Countdown to EV Industry Consolidation

Multiple factors ripen the industry for large-scale M&A

While working on this article, I had conversations about America’s EV industry with reporters from Investing.com and CNN . The Investing.com article featuring my commentary is here while my conversation with CNN senior writer Peter Valdes-Dapena (which centered around Rivian’s new R2 and R3 vis-à-vis its positioning in the market) can be read here. Laid out below is the basis for my commentary in its entirety. Read on!

Consolidation vs Consumption in the U.S.

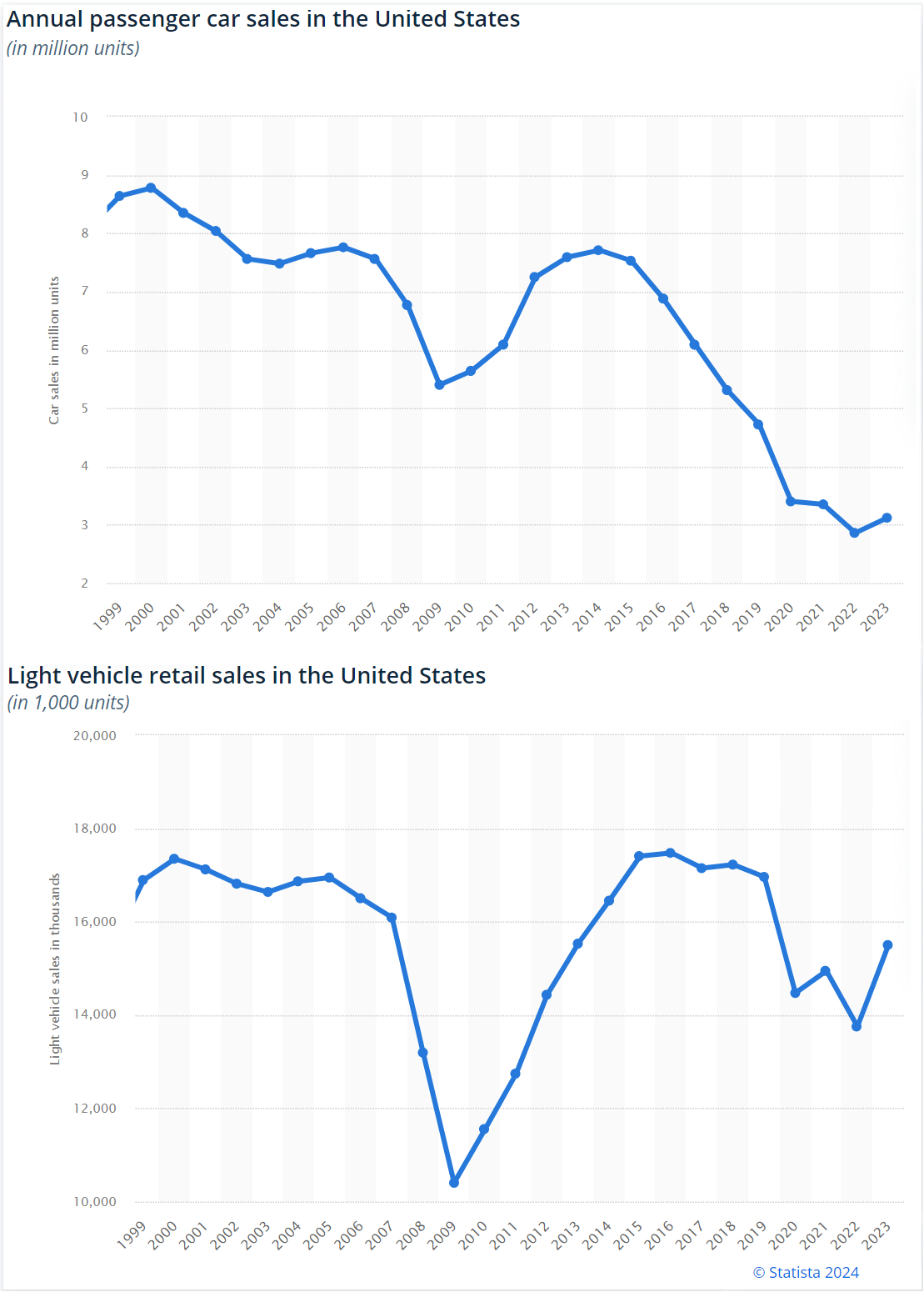

Total auto sales in the Western Hemisphere have, on average, been trending downwards over the past decade or so. This is particularly true in the United States, which forms the vast bulk of net consumption for this region.

Over the course of this century wherein “Light Trucks” (LT) — which count pickup trucks and SUVs among them — started in 1999 by leading 2:1 in total sales over Passenger Cars (PC), the ratio of LT:PC sales was at 5:1 by the end of 2023. Passenger Cars tend to be cheaper than Light Trucks; the increasing skew in the ratio thus implies that the purchase of vehicles are progressively less affordable to the average American buyer. While Passenger Car sales did witness a 9% Year-on-Year (YoY) jump in 2023, Light Trucks witnessed a 14% YoY jump. In both cases, this could be attributed to “pent-up spending” over the past couple of years. After accounting for that, Passenger Car Sales have had a resilient downtrend since 2014 whereas the downtrend begins in 2018 for Light Trucks.

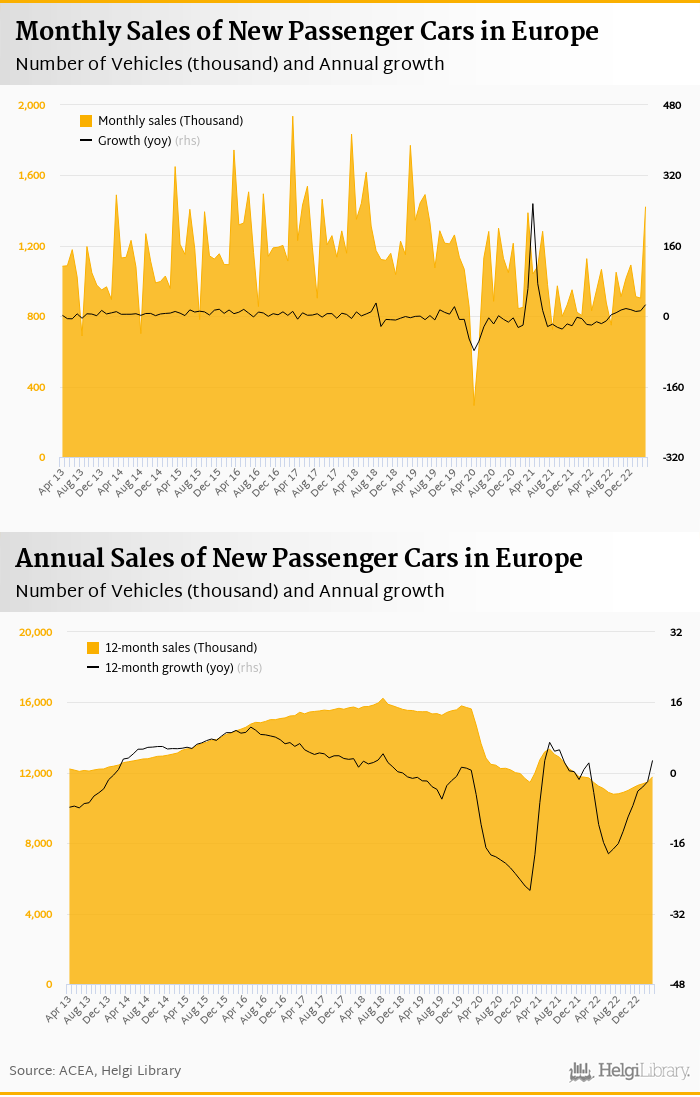

Overall trends across the European Union, however, has been relatively flat. Over the past 10 years, annual sales have been in the 12-16 million range with a relatively heavy downtrend in recent years.

The introduction of EVs does little to ameliorate the “inelasticity of reach” to low- to middle-income income segments particularly in the U.S. Historically, the average retail price of a new EV made it accessible to buyers in the "middle-to-high" income segment. These buyers are now over-catered by both “pure play” EV upstarts and multi-generational legacy carmakers who have been entering the EV space.

This divide is palpable even in the positioning of EV models slated for (or released) in 2023-2024. Only about 18% of all models slated for release cost less than $50,000, with 61% of the models being for the “middle income” segment by being in the $50-100,000 range.

Note: EV models are differentiated by model year, brand, model name, version (battery or drive type) and wheel size in inches. The final price used to derive the matrix includes the effect of Federal tax credits which are evolving.

The price matrix indicates the inherent difficulty faced by “pure play” EV makers in accessing a wide swathe of buyers. Meanwhile, legacy carmakers have extensive dealer networks to cater to buyers of all stripes without substantial capital investment and built-up brand equity to make a convincing case to buy. Given these circumstances, consolidation within the EV industry across the Western Hemisphere (particularly in the U.S.) is entirely logical. Given that Lordstown has already filed for bankruptcy, Lucid is likely to be the most vulnerable company. Since Lucid is already majority-owned by the Saudi government, it will be a reasonable measure for the latter to unload its stake to a larger carmaker in exchange for shares, cash or both.

Depending on the state of R&D in these carmakers and production facility, an acquisition would likely help cut some of the lead time for the launch of the “next generation” of EVs that the acquirer will look to capitalize on. Of course, not every “small” carmaker would have such a monetizable edge.

Current conditions are ideal for a takeover provided the acquirer has access to large cash reserves. It's unlikely that there will be a significant number of bidders making competing offers despite valuation of targets generally being depressed. If conditions were to improve, however, the acquirer wouldn't be as unconcerned but might be able to offer up a bigger price via cheaper debt issuances.

Meanwhile in China…

China is littered with a massive number of EV carmakers, often with varying levels of investment from provincial and state government bodies. So prevalent is the supply of EVs that one can be purchased via Alibaba, China’s “retail-to-wholesale” equivalent of the Amazon shopping platform.

While non-Chinese EV component makers are (arguably) dominant in the production of base parts needed for production, the market remains relatively fragmented. Most of these component makers run at least a portion of their production lines out of China, which helps ameliorate costs for Chinese EV adoption and drives an edge towards China’s burgeoning share of the world’s EV production ecosystem.

Where China does dominate, however, is in the production of batteries — arguably the single largest cost factor for EV manufacturing outside of labour and margins.

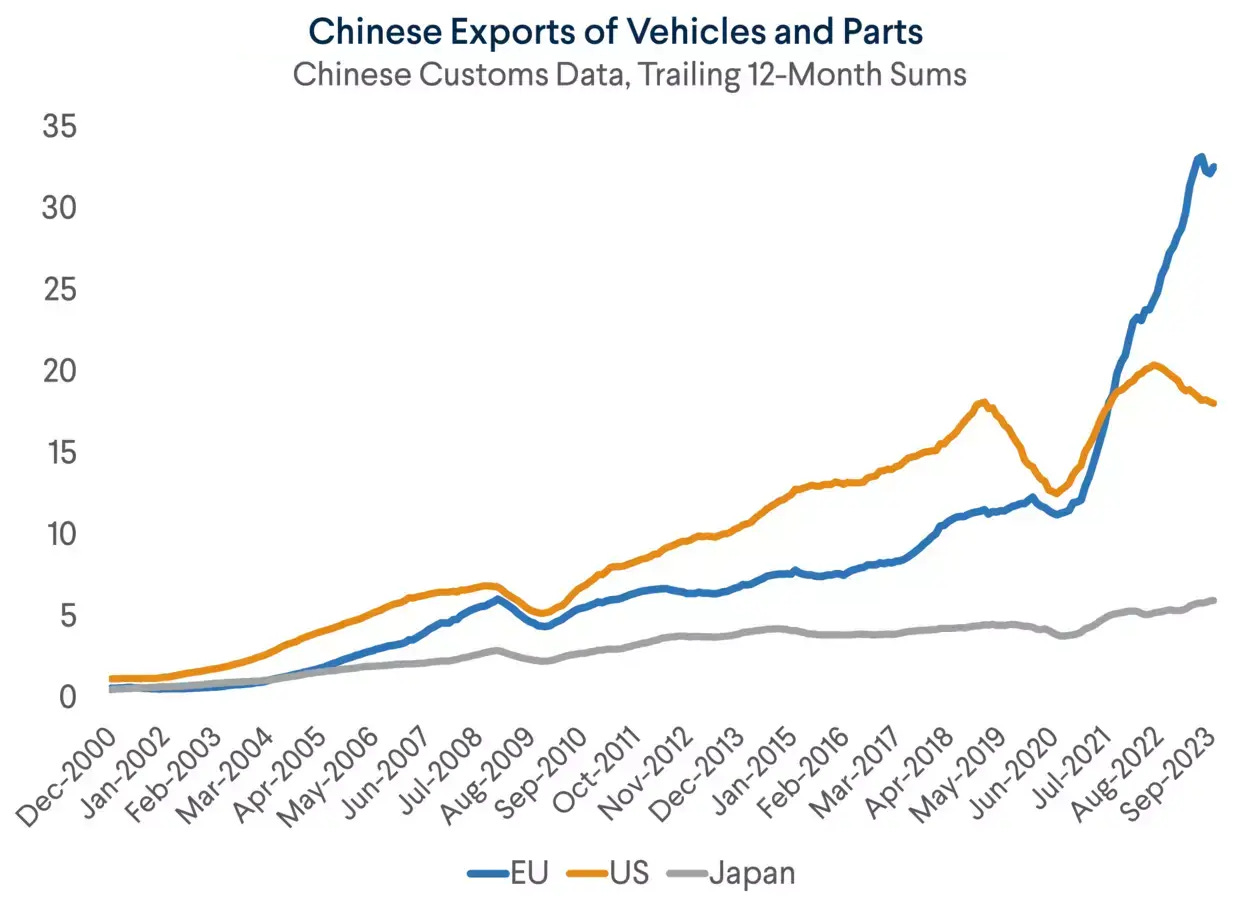

So attractive are the overall cost efficiencies wrought by manufacturing in China, both before and after margins, that exports of Chinese vehicle parts to the U.S. went up by 50% from mid-2020 to mid-2022, with Europe receiving nearly double that volume. While cooling demand for vehicles in the U.S. tightened net exports from China in the period since, the steady-to-slightly-rising sales of vehicles in Europe increased its dependence on China.

A substantial driver of the boom in Europe’s EV market can at least partially attributable to the fact that European sellers can leverage cost efficiencies offered by China’s EV manufacturing ecosystem. As a result, Europe has traditionally constituted the largest chunk of China’s EV exports worldwide.

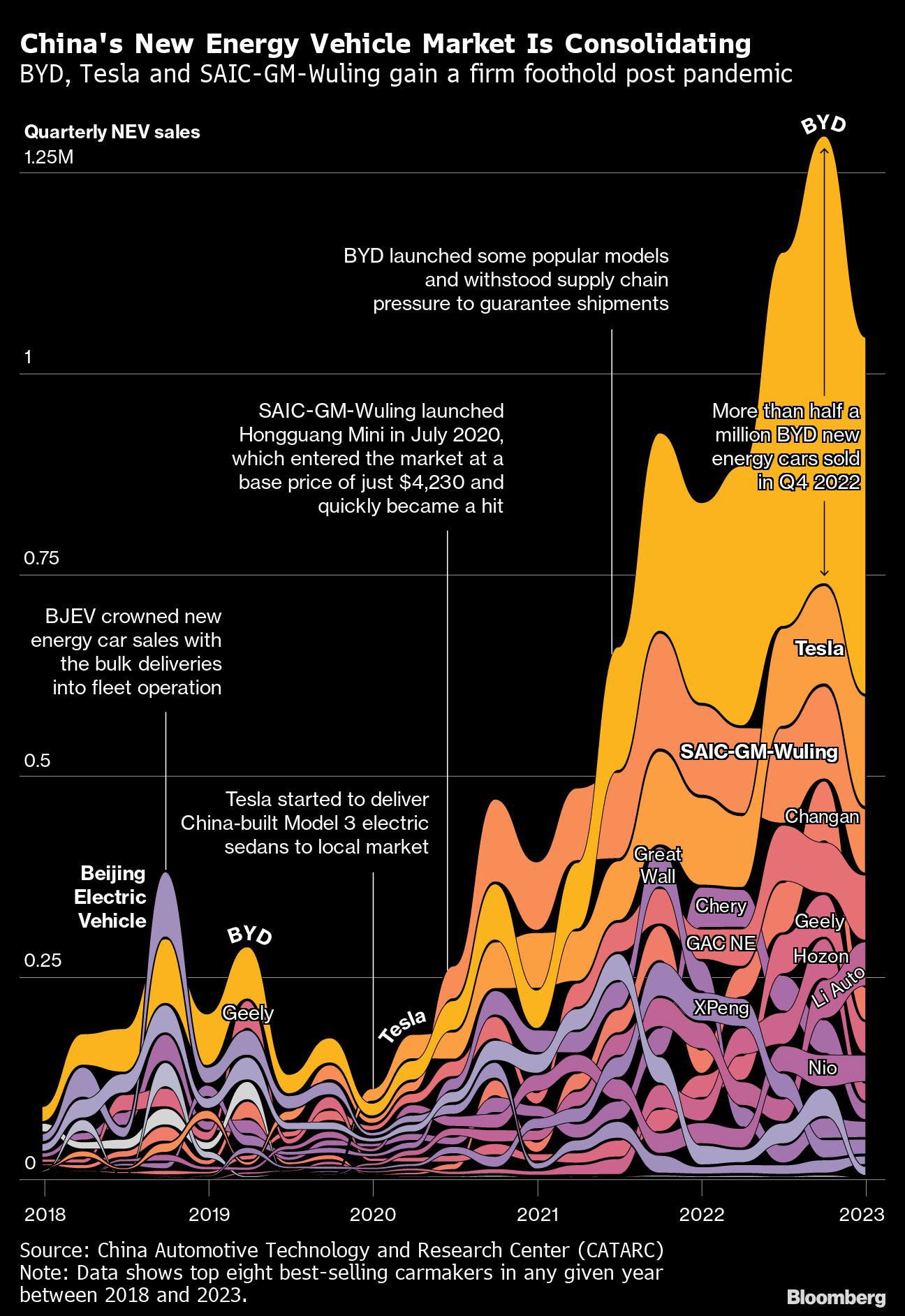

Over on the carmaker level, a large number of Chinese carmakers have little to show by way of strong market share trends. As 2023 ended, consumers were heavily leaning towards a select few names over all others.

The consolidation over here, however, will be a more subtle exercise.

Advantage: Tesla? (or) Who’s Buying Cars in America?

Despite Giga Berlin burning cash to little effect in European market share, Tesla has more than enough wherewithal to continue to retain leaderboard position for a few more years to come, despite market share sharply dwindling in YoY terms in 2023. It is, however, unlikely to attempt to boost market share by buying some beleaguered EV startup/upstart; instead, it will likely attempt to expand its brand equity by launching new premium models in the future.

As it stands, the average age of a “new car” buyer has been trending higher year-on-year (as have this demographic’s share in home purchases, long vacations, et al) while younger demographics have shown substantially less adhesion towards making “large purchases” and have been shifting ever so slightly year-on-year towards purchasing premium goods such as electronics and “experiences” (i.e. concert tickets, et al). Given that Tesla is currently poised to emerge as the only truly independent “upstart” still left standing in America’s EV Race, a shift towards a premium base is entirely logical.

Note: Commentary made to CNN also featured later in WSIL (southern Illinois), ABC12 (across the country), WRAL (Raleigh, North Carolina), the Albany Herald, News+ (Lee Enterprises), and AOL. Said commentary also featured in Business 2 Community.

UPDATE: Commentary relating to Tesla based on my reasoning here was also featured in Investing.com on the 19th of March, i.e. after the Substack post went live.

The “Dharma” series — which traces the evolution of Eastern faith and philosophy — continues to draw attention in the year so far. Here’s Part 1, Part 2, Part 3, Part 4 and Part 5, followed by the ancillary Part 6 and Part 7 discussing Malaysia’s and Indonesia’s spiritual history.

Also, click here for a list of all articles ever published.