Electric Cars of the East, Part 4: A Difference in Drivers

Electric Cars of the East, Part 4: A Difference in Drivers

A closer look at what drove the numbers up in China and what keeps the numbers down in India

In Part 1 of this series, we took a quick tour around the automotive history of China and India, in Part 2, we looked at factors underscoring their “growth stories”, and in Part 3, we understood better the actual impact of EVs in the landscape and what an “EV” meant in these parts. In this Part, we’ll flesh out the landscape further and the factors from the perspective of the main drivers of this monumental change.

In 2015, both China and India ratified their commitment to the Paris Agreement under the United Nations Framework Convention on Climate Change, now simply known as the Paris Agreement. This agreement was meant to secure commitment from the signatories that they will work on reduce greenhouse gas emissions and enhance environmental protections. Both nations had good reason to.

China overtook the U.S. as the single largest emitter of greenhouse gases somewhere by the end of the noughties. While India’s growing economic might has led to an increase in emissions too, it bears noting the India’s emissions per capita is one of the lowest within the G20.

Both nations have evolved deep policies regarding EV adoptions but they don’t necessarily come from a sense of urgency due to climate change. The best reason is perhaps the most strategic: both nations are heavily dependent on oil imports to keep their people’s vehicles running. Both nations recognize that this wrecks their balance of imports and forces an uncomfortable choke hold on their strategic position in the world.

China: All About the Benjamins?

To incentivize its citizens towards EV ownership, the Chinese government instituted the Electric Vehicle Subsidy Scheme (EVSS), a complex interlaced system of subsidies at Central, provincial and local government levels, in 2009. These were further tweaked in 2012 and 2013 - years when the EV purchasing frenzy truly began.

Under the scheme’s terms, China’s Central Government pays anywhere between ¥ 20,000 - 44,000 per EV, with virtually every local government adding around 15-50% to that amount. Also included is a sales tax exemption for EVs.

The subsidies aren’t just limited to the financial: many cities give a push for EVs with assurances such as the guarantee of a vehicle license and increased access to carpool lanes to EV purchasers. For example, the city of Beijing caps the number of vehicle licenses issued each month. There generally used to be as many as 3 million applications for the 3,000 available new vehicle licenses every month with the remainder going into a lottery pool. Buyers of EVs, however, are exempt from this process and assured of receiving a license. Similarly, in Shanghai, the cost of registering a vehicle is around ¥60,000 - 80,000; but an EV is registered for free. In 2017, when Chinese government ran a fiscal deficit of $460 billion, it was estimated that China’s central and state governments gave out about $7.7 billion in subsidies to EV purchasers alone.

Moreover, subsidies were not just limited to purchasers: virtually every provincial government provided vast sums of money to manufacturers to set up shop and begin production. This ranged from cheap or free land to set up factories, tax exemptions to corporations, capital or investments made by an entity similar to a sovereign wealth fund representing a provincial or city government - to the sum of undisclosed number of billions of dollars. Unsurprisingly, the number of “registered” EV manufacturers was reported to be around 487 in 2018.

Obviously, all is not what it seems here: an industry-wide investigation launched by regulators in late 2016 found that automakers employed a range of tricks to qualify for state support, including falsifying vehicle sales. Furthermore, the Chinese government announced in May 2018 that 1,882 models from dozens of foreign and domestic EV makers - ranging from bus-maker Nanjing Golden Dragon Bus Co. to EV carmaker BYD Co. Ltd. - will no longer qualify for tax reduction since they either hadn’t gone into production or have yet to be imported into China.

Traditional carmakers such as the “Big 4”, BAIC and GAC were first movers in receiving the benefits from subsidies and government investments: they announced and formulated plans for building EV production capacity and capabilities. But it is the upstart or “smaller” EV makers whose ambitions have drawn capital and interest from global enterprises and some of the mainland’s tech giants like Tencent and Alibaba. In a number of cases - such as BYD, Arcfox and NIO - this has paid off. On the other hand, hundreds of “smaller” EV manufacturers that had received vast amounts in funds from local and provincial governments have been missing their sales targets for some reason. *wink, wink*

Almost as if confirming these suspicions, the Chinese government announced plans to modify its subsidies in March 2019. Under the new terms, any EV with a range less than 250 km will not be receiving any more subsidies. Furthermore, BEVs with a range of 400 km and above will receive only ¥25,000 as opposed to ¥50,000. The Chinese government further went on to say that they will appeal to local and provincial governments to remove subsidies on EV purchases after a three-month grace period.

For illustration of scale, it was estimated that the net effect of these announcements on a BEV with a range of 400 km or above would be a reduction by 67% of the total subsidy amount.

Beijing planned to end subsidies entirely by December 2020 and started rolling them back in June 2019, claiming that production had gotten cheap enough to no longer warrant State support. EVs with a range of 250 - 400 km now began to receive ¥18,000 (reduced to ¥16,200 in 2020) of subsidies while EVs with a range greater than 400 km received ¥25,000 (which remained unchanged in 2020). PHEVs received a subsidy of ¥8,500. Local and provincial governments were directed to spend on improving infrastructure for NEVs.

However, on the back of declining EV sales immediately after this announcement as well as the stalling of purchases due to the COVID-19 pandemic, Beijing extended subsidy support for two years in 2020, setting a new phase-out date of 2022. In line with this new phase-out date, subsides for BEVs with a range of 300 - 400 km declined to ¥13,000 and subsidies for PHEVs declined to ¥6,800.

There is another quirk to the subsidy structure: it typically applies only to EVs priced under ¥300,000, with vehicles built around battery-swapping technology - wherein the EV purchaser simply replaces the car’s battery once it runs dead - exempted from such a price limit.

NIO used to be an interesting beneficiary of this subsidy: while a “premium” carmaker, it uses the government subsidies as an additional enticement. Its EC6, for example, costs upwards of ¥368,000 but the purchaser was eligible to receive ¥22,500 in subsidies in 2020 - making the effective price ¥345,500. The China-specific Model Y is priced at ¥440,700 and receives no subsidies.

In 2021 - after the government slashed subsidies by 20% - the purchaser would now receive ¥18,000, making the EC6’s effective price ¥350,000. Tesla slashed the Model Y’s price by 30% to ¥339,000, thus turning the tables on the Chinese carmaker.

On October 27, 2020, the Chinese Ministry of Industry and Information Technology announced that 20% of all vehicles sold in 2025 will be EVs and expects this to ramp up to 50% in 2035. The other half is expected to be conventional hybrids, which run entirely on fossil fuels.

In recent times, the government also seems to have reverted to rescuing EV carmakers in order to prevent top-line EV carmakers from collapsing altogether in the face of current events:

Luchi Motor, one of China's earliest EV startups, sold a controlling stake to the investment arm of Henan province in March 2020 after it failed to deliver EVs as per schedule.

NIO, on the verge of bankruptcy, secured a ¥7 billion investment from state-controlled investors in April 2020.

WM Motor, another EV start-up backed by Baidu and Tencent, raised ¥10 billion yuan in Series D funding led by a Shanghai-based state-owned investor group that included SAIC Motor in September 2020.

XPeng, an EV carmaker accused being sued Tesla of stealing its IP (until yesterday!), received a ¥4 billion investment from the Guangzhou city government in September 2020, a credit line of ¥12.8 billion from major state-owned banks in January 2021 and a further ¥500 million from Guangdong provincial government (the capital of which is Guangzhou).

India: Adapt or Be Bulldozed!

As of 2012, the Indian economy was largely powered by coal. By 2017, India had made significant steps towards adopting solar energy and had scrapped 13.7 GW of planned coal power projects. The rising availability of electricity compelled the NITI Aayog, the government’s policy think tank, to suggest that EVs would find greater acceptance across the nation, if planned well.

Elements within the Indian auto manufacturing ecosystem had kept a close eye on China’s EVSS and began to raise demands for subsidies a la EVSS along with state funding. In response, Ministers Nitin Gadkari and Piyush Goyal, then in charge of Road Transport & Highways and Power respectively, at the Society of Indian Automobile Manufacturers’ convention in 2017 warned representatives of auto manufacturers to work on switching to alternative non-polluting technologies or be “bulldozed”.

After much back-and-forth between carmakers and government advisors, the Faster Adoption and Manufacturing of Hybrid and Electric vehicles in India (FAME) scheme was launched in 2015, with a budget of ₹ 795 crores (Note: a “crore” is 10 million). The incentives under FAME Phase I was offered on purchase of hybrid and electric cars, 2-wheelers and 3-wheelers. In 2017, “mild hybrids”* were removed from this list after 111,897 vehicles received benefits from this scheme between period April 1, 2015 and February 28, 2017, with mild hybrid 4-wheelers accounting for 73,633 of these. “Strong hybrid” cars accounted for a mere 1.7% and BEVs only 1% of subidy recipients. The remainder of the benefits were received by 2-wheelers and 3-wheelers.

”Mild Hybrid” cars (also known as “battery-assisted hybrid vehicles” or BAHVs) only use their electric motors to support the engine during acceleration and cruising – the electric motor cannot power the car on its own. “Full Hybrid” cars (or “strong hybrids”) can run on just the engine, just the batteries, or a combination of thereof.

The country’s largest carmaker Maruti Suzuki’s Ciaz sedan and Ertiga MPV as well as Mahindra’s Scorpio was the most impacted models after the withdrawal, since the latest iterations were touted as being equipped with “hybrid technology”. However, advocacy group Centre for Science and Environment (CSE) welcomed the move stating that mild hybrids have blocked the scaling up of strong hybrids and BEVs. This is because, although regarded as “hybrids”, these vehicles do not offer a comparable level of fuel and emissions reduction as “full hybrids”.

In 2017, Nagpur – Minister Gadkari’s constituency and in the state of Maharashtra which houses a large percentage of the nation’s automobile manufacturing facilities – flagged off a pilot project to transform the city’s mass transit program with 200 electric buses, taxis and 3-wheelers. Taxi aggregator Ola invested in charging infrastructure with 50-plus charging points across four locations. Mahindra Electric Mobility’s e2o mini cars received the bulk of the contract for taxis while the rest were slated to be distributed across other OEMs such as Tata Motors, Kinetic Motors and TVS Motors, with China-based BYD* and SAIC also evincing interest in the same. In addition, the state of Maharashtra waived Value Added Tax, road tax, and registration charges for all electric vehicles in the state.

*BYD doesn’t secure the contract initially but its venture with Megha Engineering India Limited-owned Olectra to produce electric buses eventually goes on to secure over $100 million in orders from state-owned bus operators in different parts of the country, including in Nagpur during the second and third rounds of vehicle purchases.

Going as per the NITI Aayog’s report that India can conservatively save up to 64% of anticipated passenger mobility-related energy demand and 37% of carbon emissions by 2030, the Energy Efficiency Services Limited (EESL), the world's largest public energy services company and a 100% state-owned concern – was created to transform government vehicle fleets across the nation by switching to EVs. With an estimated fleet size of 500,000 cars, this was conceived to assuage Indian carmakers’ concerns about initial market demand and to lay the groundwork for EV-building capacity.

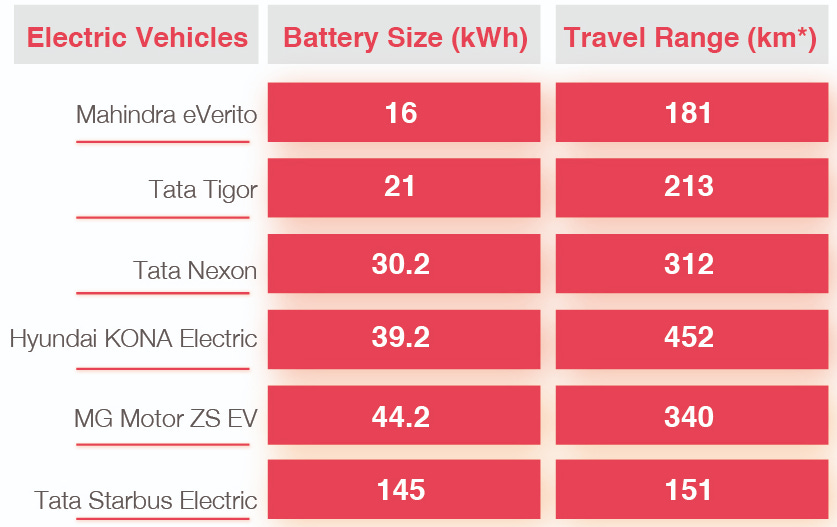

An initial tender for 10,000 cars was floated in August 2017 by EESL; bids from Tata Motors and Mahindra qualified; both companies supplied about 1,500 electric cars to EESL by January 2020 before the company decided to close the tender due to resistance from government officials assigned these EVs. The resistance was due to performance issues: these EVs delivered an “on-road” range of 85 km against an NECD-derived range of 130 km. Experts also noted that the battery pack was of 18 kW while the global standard is 25-35kW, which also impacted performance. EVs with a battery pack of around 30 kW are expected to have a range of at least 250 km*. The final portion of the now-heavily-reduced tender was fulfilled by China-based MG Motor, which delivered the first batch of its new ZS electric SUVs to fulfill its obligations (and thus officially entering the Indian market).

*Both Tata Motors and Mahindra stated in the aftermath that they learned a lot from this experience: large-scale orders like this taught them how to evaluate EV performance and gave them data on how to improve this segment for better marketability

A second tender for 10,000 vehicles floated by EESL in April 2018 had to be scrapped as the auto industry demanded clarification on specifications for chargers which would have allowed foreign high-end luxury automakers to come into the picture: Indian carmakers had earlier agreed to abide by Government specifications titled Bharat EV Charger AC-001 and Bharat EV Charger DC-001* for AC and DC charging respectively while high-end European and Japanese manufacturers employ Combined Charging System (CCS) and CHAdeMO, which are not entirely compatible with the proposed Indian system. Thus, Indian manufacturers contended that European and Japanese companies should not be eligible for consideration.

*There’s a whole mess of technical information regarding the Bharat Charger. Look here, dear reader, to find out what they are.

The Indian government proceeded with FAME Phase II (or FAME-2) in August 2018, with an outlay of around ₹ 10,000 crore spanning over 3 years to subsidize the purchase of 1 million electric 2-wheelers, 7,000 electric buses and 55,000 electric and hybrid passenger cars in the three-year period starting April 2019. However, only vehicles with over 50% localisation (i.e. at least 50% by vehicle must be built in India) and equipped with lithium-ion batteries were eligible for the subsidy. For 2-wheelers, there were the additional requirements of a maximum speed of at least 40 kmph and a range of 80 km per charge.

In FY19, 70,486 electric 2-wheelers of the 126,000 units sold received subsidies. In FY20, only 13,490 two-wheelers of 152,000 units sold received subsidies. The director general of the Society of Manufacturers of Electric Vehicles (SMEV) - who also happens to be the global Chief Executive of 2-wheeler manufacturer Hero Electric - contended the market was only ready for low-speed, electric 2-wheelers on account of its cost-efficiency. He did concede, however, that the government’s intention to disincentivize EV makers from simply importing kits from China and instead create a domestic supply chain was “right but premature”.

In addition to 2-wheelers, around 2,300 electric cars and 600 electric buses also received subsidies.

In October 2019, the Indian Ministry of Power issued guidelines to quash the squabble over charging standards by ruling that:

Private charging at residences/offices shall be permitted and power distribution companies (DISCOMs) may facilitate the same;

Setting up of Public Charging Stations (PCS) shall be a de-licensed activity and any individual/entity is free to set them up, as long as they adhere to tariffs prescribed;

PCS owners have the freedom to install any charger - be it CCS, CHAdeMO, Type-2 AC, Bharat AC-001 or any other - as per market requirements

The government also stated a core goal to have at least one charging station available in every 3 square km grid in cities and one charging station every 25 km on both sides of intra-city highways. All major cities (and expressways connected to these cities) are to be taken up for coverage in the first phase and other big cities are to be taken up in the second phase. For inter-city travel, fast-charging stations will be installed at every 100 km at least.

In June 2020, the Ministry determined that the tariff charged at PCS shall not be more than the average cost of supply (ACS) plus 15%. ACS is the average of the rates at which a state supplies electricity to all consumers — domestic, commercial, industrial, and agriculture. All-India ACS was reported at ₹ 5.48/kWh in FY 2017-18. As of 2020, the tentative charging cost at a PCS based on usage patterns was estimated at around ₹ 160-200 to fully charge a 39 kWh Hyundai Kona. Other metrics point to an average cost of ₹ 0.8-1.5 per km of range.

One key element of difference between China and India is taxes. While the “standard” vehicle sales tax is around 10% in China (with some models of EVs exempted), the Goods and Service Tax (GST) on “standard” cars is far more brutal in India: mid-size cars are 45%, large cars are 48% on large cars SUVs are 50%. Used car sales were initially fixed at the same levels until the government softened its stance and reduced it to 18% under those 3 categories. For comparison, the vehicle tax for used car sales is 2%. This gives additional colour for the explosion of vehicle sales in China, relative to India’s… relaxed… growth, over the past two decades. Road taxes (or license plate taxes in China) in both countries are determined on a state/provincial basis and vary widely.

Until 2019, the GST on electric cars was fixed at 12%. In 2019, the government cut the GST on BEVs to 5%, while hybrid vehicles continue to be taxed at 43% (28% GST plus cess). This, dear reader, is the reason why HEVs - be they “mild” or “strong - don’t feature in EV sales statistics (I hope you remember the mystery in the Indian EV sales statistics we looked at near the end of Part 3). Indian BEV majors Hyundai Motor India Ltd, Tata Motors Ltd and Mahindra vigorously oppose any move to introduce a reduction in GST for “hybrids” which would benefit Japanese automakers, who have been hybrid vehicle champions for years.

Other notable developments in terms of infrastructure and policy are:

In 2019, Indian exploration agency ISRO licensed its indigenously-developed low-cost Lithium-ion battery manufacturing technology to Tata Chemicals, on a non-exclusive basis, to manufacture cells of varying capacity, size, energy density and power density. 15 other Indian companies were shortlisted later that year and their suitability is under evaluation.

Regulations such as the 2nd phase of Corporate Average Fuel Efficiency (CAFE 2) and Real-time Driving Emission Tests (RDE) will be introduced in 2022 and 2023 respectively that will make it necessary for all automakers operating in India to include BEVs and HEVs in their product portfolio.

A mandatory vehicle scrappage policy for all government vehicles older than 15 years to be replaced by EVs was approved in January 2021 and will be coming into effect from April 2022. A similar policy for private-owned vehicles - with adequate compensation and incentives - is being mulled and contested in the country’s courts.

In January 2021, the Ministry of Road Transport and Highways approved a proposal for Green Tax on commercial vehicles (CVs) older than eight years at the rate of 10-25% of road tax. Vehicles used for farming (tractors, harvesters, tillers, etc), “strong hybrids”, BEVs and vehicles using alternative fuels (CNG, ethanol and LPG) will be exempt.

By the end of 2020, MG Motor and Tata Power had installed 15 60 kW Superfast EV charging stations - compatible with the CCS fast-charging standard - across 10 cities. Tata Power, on its own, has gone to establish an EV Charging ecosystem with over 200 charging points in 24 cities under the “EZ Charge” brand that is continuously looking to recruit franchisees.

In FY 2019-20, EESL set up around 207 charging stations across India. In FY20-21, the company announced plans to set up 500 more. Eventually, it plans to set up 10,000 charging stations by FY 2023-24.

This is a Lot, Kaminohikari-Sensei, But What Does it Mean?

An interesting trend worms its way through Chinese sales data: the preponderance of strong foreign vehicle sales in both EVs and conventional categories. Given the oh-so-many pieces by “journalists” about the sheer weight of Chinese firms, wouldn’t local firms have held sway if all else was equal?

It’s simply not right to dismiss this as an example of Chinese people’s preference for “branded” (read: foreign) goods. The source of this marked preference was likely due to well-developed EV systems in foreign carmakers’ products, which proved to be more efficient than the offerings of most local carmakers. In 2019, during the first round of cuts in subsidies, the government outright said that EV manufacturers are encouraged to rely on innovation rather than government assistance. Serving almost as a lead-up to this assertion, Ian Zhu - managing director of NIO-backed venture capital fund Nio Capital - warned in late 2018 that only 1% of China’s EV startups will be able to survive in an industry that requires significant investment in technology.

The generous subsidies paid out until 2019 comprehensively blinded most casual observers of the fact that owning an EV simply meant a Chinese purchaser had a set of cheap wheels that - ultimately - didn’t perform very well in the mid-to-long run. This is what spurred ownership of foreign brands in China; it’s better to pay more to own a decent vehicle and China’s low interest rates helped many citizens do exactly that.

However, I wouldn’t consider it a complete failure in policy: a number of high-quality EV carmakers - Arcfox, NIO, BYD, et al - have arisen from this glorious mess and will likely have a role to play in the near future. This is likely why the Chinese government resorted to doling out financial assistance to select firms in this past year.

While all of this was unfolding, the Indian government and its advisors were likely quietly watching and analyzing events. This is why the Indian government has been so ruthless with regard to subsidies: it’s oh-so-easy to start a EV company, import “kits” from China, put them together, sell them to the public and call it a “startup success story”. Given the issues with increasing range and speed, EVs that can actually be a viable and equivalent (and better) alternative to “standard” cars in all positive aspects such as performance are needed. It’s not quantity that’s important, dear journalists with your short lead times to make copy (which I totally understand and sympathize with), but quality.

A failure to dole out subsidies because of stringent conditions in place is not a failure of policy to promote EVs. A namby-pamby sop for just any thing passing off as an “EV” is not just a waste of public funds. While the subsidies for a sub-par product comes out of the tax coffers, the balance is taken from the citizen’s bank account in exchange for a sub-par product. That’s a huge disservice to (and loss for) the citizen. That was likely a valuable lesson learned by the Chinese government - and the Indian government and its policy experts learned it too just by watching events unfold. That also explains the Indian government’s course corrections. “Mild hybrids” and low-cost 2-wheelers that the “market is ready for” (to quote the Global Chief Executive of Hero Electric) are not the way forward to building a strong EV ecosystem.

Sure, that means that a bunch of “journalists” don’t write reams of newsprint about your “exotic” country and go “Whoooooa!” while doing so. But meh, what do they know? Size doesn’t matter….

… Or does it?

That last question brings us to the end of Part 4. I’ve danced around talking up the big elephant in the EV room - name starts with a “T” and ends with a “sla” - for a reason. Its success in China wasn’t just because it’s a “brand” and it’s fortunes in India won’t be just because it’s a “brand”. In Part 5, we see how “size” relates to said EV elephant in India. Stay tuned and hit “Subscribe” here if you haven’t already!