Electric Cars of the East, The Finale: Odds and Ends

Conclusions, Possible Strategies and the Future

Part 1 took us through the automotive history of China and India, Part 2 discussed their “growth stories”, Part 3 outlined what EVs mean in these parts, Part 4 outlined prime drivers’ actions, and Part 5 discussed Tesla’s prospects in its newest landfall: India. In this part, we’ll put them all together and bring this blessed series to a close.

The future is clear:

BEVs are both inevitable and will be the mainstream in most parts of the world in a matter of years, not decades.

This series needs to end soon.

However, I did leave out discussing battery tech till now. The reason for that is simple: battery tech innovations are in a state of constant flux with quantum improvements seemingly around the corner.

“Showdown at the Battery, Showdown at the Battery, Now”

-They Might Be Giants

The core of the EV is, of course, the battery pack. Virtually every EV uses lithium-ion batteries - which has lithium at its core. In most EVs, the battery pack accounts for about around $10,000–$12,000 of the total cost of the vehicle (not “price”, dear reader. The EV buyer pays a price; the EV carmaker incurs a cost).

Morgan Stanley reported in 2019 that global production of lithium carbonate equivalent (LCE) topped at around 380,000 tonnes in 2019, of which a third was destined for EVs. Lithium carbonate is a stable form of lithium from which the highly-reactive lithium metal is refined; it is estimate that about 5.2 tonnes of lithium carbonate is required to make a ton of lithium. Working backwards implies that about 73,000 tonnes of lithium was produced, of which a little over 24,000 ended up in EVs. In 2020, 82,000 tonnes of lithium was produced.

A typical cell within an EV battery has a couple of grams of lithium. Assuming an EV has about 5,000 battery cells, a single EV has roughly 10 kilograms of lithium. Working forward from there, it can be estimated that a ton of lithium metal is enough for about 90 EVs.

The problem is evident: there isn’t likely enough lithium mined to do a complete switch from “conventional” to EVs across the world at a rapid rate. However, the global supply of lithium has been improving: the price of lithium carbonate went from $12,000 in 2019 to $8,000 in 2020. However, with improved EV penetration in 2021, the price of lithium carbonate has been rising - which goes to prove why supply needs to improve further. It has been estimated that battery costs in EVs will be going up, with reports indicating that Tesla in China will be raising the prices of its products soon. However, the additional price incurred by the EV buyer is not expected to go beyond a few hundred dollars for some time.

To promote savings in lithium usage, solid-state batteries (SSB) have been touted for quite some time now. A SSB uses solid electrodes and a solid electrolyte, instead of the liquid or polymer gel electrolytes found in lithium-ion batteries. SSBs are estimated to deliver higher energy densities than the current “sizes” of lithium-ion batteries, which in turn means that SSB tech will mean “smaller” batteries (and thus less lithium usage).

In 2011, French conglomerate Bolloré SE launched the “BlueCar” EV in limited numbers as a showcase of its prowess in battery tech - the BlueCar utilized an early form of commercially-viable SSB tech. In 2012, Toyota and VW independently announced research into SSB tech as well. Thanks to its intensive work in developing this area, Toyota holds the most SSB-related patents relative to all other carmakers.

In 2017, even Nobel Laureate Dr. John Goodenough, the co-inventor of lithium-ion batteries, unveiled a solid-state battery with nearly 3X the energy density as lithium-ion batteries at that time, in the University of Texas at Austin.*

*This is a shout-out to an early subscriber of this newsletter.

In 2018, Volkswagen announced a $100 million investment in QuantumScape, a solid-state battery startup that spun out of Stanford University, in order to viably bring SSB tech to the market. VW also offered a very helpful example of the benefits of SSB tech, courtesy QuantumScape: a SSB would potentially increase the range of the VW E-Golf from its present stated range of 300 km to approximately 750 km.

Similar to QuantumScape, Qing Tao (Kunshan) Energy Development Co. Ltd spun out of China’s prestigious Tsinghua University with the same goals in 2018 and established an SSB manufacturing plant with a capacity of 100 MWh/year and plans to ramp this up to 700 MWh by 2020. However, in 2021, it has being estimated that China EV stalwart NIO’s supplier for its new 360 Wh/kg SSB with a 1,000 km range is either Taiwan-based Prologium or NIO’s current battery supplier China-based CATL.

In December 2020, the Indian government approved a $2.2 billion production-linked incentive (PLI) scheme for 10 “key” sectors - including advance chemistry cell (ACC) battery (a catch-all term that includes EV batteries). Soon afterwards (i.e. yesterday!), India-based Omega Seiki Pvt. Ltd. formed an alliance with US-based Charge CCCV (C4V) to avail the benefits of this scheme while introducing solid-state batteries with 400Wh/kg energy density in India that will also be cheaper than many types of lithium-based batteries. The VP of Strategic Partnerships at C4V said, “We wish to make India completely Atmanirbhar (meaning: “self-reliant”) in EVs and renewable energy ecosystem from cell and battery manufacturing. In India our industrial cluster approach going to have a complete backward integration and/or co-location with for lithium-ion cells manufacturing.”

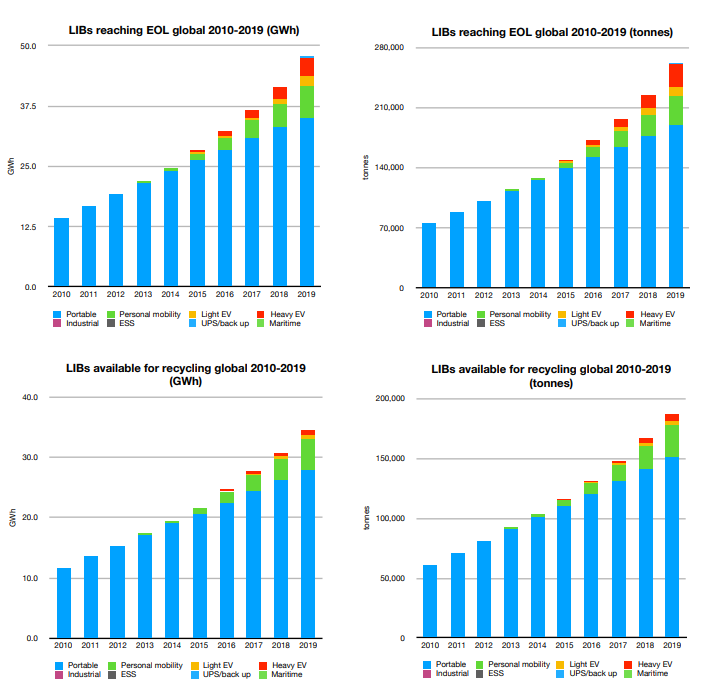

There are a LOT of batteries floating around in mobile devices, power backup systems, etc. By 2019, it was estimated that around 270,000 tonnes of lithium-ion batteries (LIBs) had reached their End of Life (EOL). About 80% of these are from portable electronic devices. Clearly, as battery tech improves or an alternative is found to be commercially viable, lithium recycling is the need of the hour for the EV industry in particular and the environment in general.

In 2018, China recycled around 67,000 tonnes of LIBs last year (or 69% of all the stock available for recycling worldwide) with South Korea processing about 18,000 tonnes. Both China and South Korea have emerged as preferred destinations for battery waste since the waste receives much higher prices there than from businesses in Europe or the U.S. Interestingly, studies find that the recycling industry of virtually market has overcapacity built in – including in China – primarily because of a lack of solutions to efficiently collect batteries.

North America and Europe have also woken up to this need, with a number of startups rising to the challenge. Tata Chemicals Ltd became the first major mover for recycling in India after commissioning a lithium-ion battery recycling plant in Maharashtra in 2019, with the recycling market in India estimated at being at least a billion dollars.

But what of technologies based on material other than lithium? Well, in that regard, the sky is bluer than it is with LIBs.

In 2019, Oxford-based startup ZapGo reported developing a battery with solid-state carbon-ion cells and no lithium or cobalt, along with the ability to charge this battery 100 times faster than other LIB-compliant superchargers. The company went belly-up in 2020.

In 2020, India-based startup Gegadyne Energy announced developing a carbon-based battery built around non-lithium based proprietary technology that can fully charge an EV in less than 15 minutes. In January 2021, V-Guard - a leading Indian Fast Moving Electrical Goods (FMEG) company - acquired a minority stake in Gegadyne for a sum of $4.5 million to incorporate Gegadyne-derived technology in future products.

In March this year, France-based NAWA Technologies announced developing technology based on a vertically-aligned carbon nanotube (VACNT) design which it states will boost battery power ten-fold, increase energy storage by 3X and increase the lifecycle of a battery by 5X, with charging times cut to 5 minutes to get to 80 per cent. The technology could be in production as soon as 2023.

The battery space is filled with possibilities in the future and a near-constant drive to optimize the present. Regardless of whether SSBs become the norm or carbon-based batteries do, it is certainly hoped that the technology will be backward-compatible with present-generation BEVs and high-end PHEVs.

If not, that’s probably yet another multi-billion dollar industry waiting to form!

So How Are You Wrapping This Series Up, Sensei?

… you, dear reader, asked with misty eyes. Well, lets get right into it (for the last time in this series).

In Part 1, I mentioned that nearly all foreign brands are manufactured in partnership with a Chinese firm, with Tesla being an exception. In mid-2020, after looking at flattening consumption patterns for automobiles, the Chinese government amended this to stipulate that it is willing to consider proposals by foreign carmakers to set up production facilities without a Chinese firm as a partner, in a bid to promote the country as an export destination for automobiles. India already had this arrangement in place and, as we uncovered in Part 2, actively competes with China for export volumes. So, all things considered, its status quo in terms of choices for foreign carmakers: these two countries frequently end up on the list together.

Taking in Part 3 and Part 4 together, I essentially dismissed commentators and journalists going “ohmigawd China you gaizzz” with respect to China’s EV numbers as just clickbait (Yes, I know, journalists! Clicks make bucks nowadays, jeez!). China’s EV majors are struggling to bring in cost-effective innovation and performance into their indigenously-made products and the Chinese Government is likely highly aware of the issues, regardless of what they tell the media. However, outside of Chinese companies, leading carmakers from outside of China seem to have developed higher-quality EVs that aren’t just in the “high-end” segment. The struggle lies in making an EV that is cheaper than or as cheap as discount gas-guzzlers but with equivalent or better performance. This struggle is real for every EV carmaker.

In Part 5, I had mentioned that, as far as Tesla’s current catalogue is concerned, there would be plenty of competition in-place by the time the company hovers its way into India. Now, make no mistake: Tesla has done more for “mainstreaming” EVs than, say, Ford. It’s almost like how Ford enabled people to move on from horse-buggies. But, just like it did with Ford, the competition has caught up.

With its current catalogue in a world that now embraces BEVs, Tesla is a mid- to high-end carmaker. For it to connect with the masses, it’s long-cherished dream has been the sub-$25,000 EV - a dream that has eluded it ever since it was spoken out loud. To make meaningful inroads, it might be necessary to bring this dream into fruition.

In Part 1, I had mentioned how Tata Motors’ Advanced Modular Platform had a significant cost advantage over VW’s MQB-A for designing new models. A potential for collaboration with Tata Motors might help bring economies of scale around. Given that its likely that Tata considers India it’s turf, this is very, very unlikely.

In 2015, while being inducted into the Automotive Hall of Fame in Detroit, Mr. Ratan Tata, Chairman Emeritus of Tata Sons, said:

“The greatest pleasure I’ve ever had is trying to do something that everybody says could not be done. I’ll just share a moment in time that I will always cherish: I decided that India could produce its own car. Everybody - my friends overseas, in the automobile business - said, “This couldn’t be done. We had to go through a collaboration to get know-how, to get technology”. But we undertook to produce this car. It was called the “Indica” and we produced it in India. Totally of Indian content.

As we got close to putting it in the market, my friends in India somewhat distanced themselves from me… otherwise known as “distancing yourself from failure”. When the car came out, I suddenly felt that I didn’t have a friend in the world and all the warnings that people had given me were probably going to come true. But the car did come out, did earn a 20% market share and we showed that we can do something.”

The next contender for an alliance would be Mahindra & Mahindra, which runs with the same sentiment. It has come a long way since the time it had to import used Peugeot engines for its Willys Jeeps made under license. Also, there are at least 4 new EVs being launched by the company in 2021. Depending on which segment each of the EVs fall under, it could very well be that Tesla is a competitor for the home turf.

Another option could have been the likes of Toyota. However, the company recently (3 days ago!) announced the launch of 70 electrified models by 2025, including 15 BEVs.

In December 2020, Hyundai unveiled its ElectricGlobal Modular Platform EGMP - a dedicated BEV platform - to form the basis of the 12 BEVs its planning to launch by 2025. So that one’s out too.

It’s a prickly situation for Tesla. While India may not be its saving grace as it seeks new markets to expand into, it’s entirely possible that it would find some buyers based on its brand equity. While said equity isn’t nearly as high as that of India’s enduring/endearing “local heroes”, it will certainly be better than nothing.

As for China’s “local heroes”, there are rivers to ford and bridges to build. But for the sake of the world and the environment, let’s hope their journey never falters.

This brings us to the end of Part 6, i.e. “The Finale”. While each Part was launched within two days of the preceding one, rest assured that this will not be this newsletter’s frequency. I’m off for a couple of weeks or so to recharge my batteries before I return with a new less-wordy subject matter of interest. Rest assured: my next piece will not be about EVs. No, really.

Stay tuned and hit “Subscribe” here if you haven’t already!