Indian Markets: Solid Domestic Performers Need Protection

Part 3 of the "Great Delink" Series that highlights the increasing distance between the West and the East

So far, 2022 has been a very interesting year for Indian equity markets. Two representatives of the National Institute of Securities Markets (NISM) - a national apex body under the Securities and Exchange Board of India that’s also the de facto training institute for the civil service associated with India’s regulatory bodies - revealed a number of very interesting trends seen in the Financial Year FY 2021-22.

First, total “cash market” turnover on Indian stock exchanges by foreign portfolio investors (FPIs) reduced to 12% in 2021-22 from 15% in 2010-11. The “cash market” is the daily/intraday trading segment of the market. Considering the fact that market capitalization has grown substantially between the stated periods, it’s clear that while participation has increased in the aforementioned periods, they’re less significant as a driving force in this “secondary market” (markets where liquid securities are traded).

This gap has been filled by domestic retail investors. In Calendar Year 2021 alone, 32 million trading accounts were opened. Over the past three years, the net ownership trend has increased to 9.7% from 8.6%. In the cash market, these investors bought in with about ₹1.405 trillion in 2021, a level that is 274% that of the previous year. This is the same behaviour pattern that domestic institutional investors (DIIs) were exhibiting in the previous entry of this series.

Another interesting statistic was that FPI outflows for FY 2021-22 was nearly identical to the CY 2021 inflows by domestic retail investors: ₹1.22 trillion - which is about 45% greater than the sum of that seen in the three most recent years with net FPI outflows.

Second, total “Assets Under Custody” of FPIs in FY 2021-22 is the largest category as per market capitalization: ₹51 trillion. “Assets Under Custody” (AUC) denotes the market value of all client assets invested through FPIs, which is distinct from “cash market” turnover. Mutual Funds and insurance companies come second and third with a collective value of ₹57 trillion.

This is an interesting implication: India-focused (or “India-curious”, perhaps?) investors overseas are lockstep with domestic retail investors and DIIs and at odds with what outflows by FPI “day traders” suggests. In fact, FPI holdings in ownership trends - which is an even longer horizon than custodial holdings - has been in the 19-21% range over the past three years.

Third, a large chunk of FPI flows were diverted from the secondary market to the “primary market”, i.e. the market where new securities that weren’t previously traded are issued. This picked up substantially in the November-December 2021 period where a large number of big-ticket listings hit the Indian bourses. The total resource mobilization by FPIs was a rather modest (but nonetheless significant) amount of around ₹52 billion.

But this is where Western investment houses have a “knowledge gap” when it comes to Indian markets.

Knowing the Space

Among the list of successful IPOs at the National Stock Exchange (NSE)/Bombay Stock Exchange (BSE) in India in 2021 stood one outlier - at least for Western institutions: PayTM, whose IPO came a cropper.

PayTM was modelled along the lines of payment solutions such as U.S.-based Square and Venmo. Given this fact, “valuation guru” Mr. Aswath Damodaran - a Professor of Finance at NYU and a quotable figure among some business school graduates from India and overseas - stated in various media outlets and in his blog that the valuation of the company is around $20 billion while the company maintains “a dominant market share of the mobile payment market in India”. This is well in line with how Wall Street analysts went about evaluating the IPO and its listing price. What none of them did was understand the market in non-superficial terms. For one, they simply didn’t understand the United Payments Interface (UPI).

The Indian government has long been interested in a high adoption of digital payments by citizens. Towards this end, the country's central banking authority - the Reserve Bank of India (RBI) - funded the development of the UPI, which connects the country's banks and financial institutions (along with the likes of, say, Google Pay) together so that users can transfer cash among themselves within seconds. To further this, RBI even oversaw the development of a single app called BHIM that users can download and configure to link with their bank accounts. As a result, India's digital payments sector registered 10 billion more transactions in 2020 than China's 15 billion and is set to account for over 70% of all payments by volume by over 500 million users by 2025.

Furthermore, there are no transaction charges or limits on daily transactions. This is unlike with, say, Venmo and Cash App where a U.S. user will have to incur fees for cross-transfer of funds. The Indian government seems disinclined to allow fees to be introduced in this sector any time soon.

PayTM also hoped to become a primary destination for loan-seekers, with ambitions to have 1 million users in this category by the end of the fiscal year. Now, the company wasn't registered as a financial institution; it partnered with banks and other financial institutions who (in reality) offer the loan in exchange for the equivalent of a finder's fee. PayTM isn't the only “online business” that offered this facility nor was this practice introduced specifically by “online businesses”; India has long had an extensive network of independent loan agents who helped match loan-seekers with qualified lenders.

In this environment where all barriers to entry by financial institutions - both big and small - have been reduced or altogether eradicated, analysts should have questioned what PayTM's unique selling point was. The answer would have been: “None”. The payments landscape had been leveled to accomplish a larger and far more important national objective than mere shareholder value. This is a cultural differentiator between the East and West.

It's a problem when investment professionals simply copy a forecasting model known to work elsewhere instead of building a model from scratch that takes into account key landscape features and specific externalities. “Wall Street”-educated analysts couldn't even fathom this paradigm while Dalal Street's street-smart investors ate the former's lunch by utterly rejecting the proposed valuation. In fact, the closing price as of December 23 last year was 37% lower than the issue price of ₹2,150, which had received a bullish signal from Morgan Stanley the previous day after gaining approval to effectively become a bank for foreign fund transfers. However, even Morgan Stanley’s recommended target price was 13% lower than the issue price. Since its listing, the stock has reached neither the listing price nor the aforementioned target price; as of July 18, the closing price was 27% and 17% lower than each of these prices respectively.

Wall Street houses' India analysts sometimes bemoan that the Indian equity market is “too conservative”, but Dalal Street has come a long way in the past 30 years; it simply doesn't (and needn't) kowtow to Wall Street-style hoopla on its turf.

That wasn't even the last time Dalal Street got one over Wall Street’s India desks: on December 21, CE InfoSystems (better known as “MapMyIndia”) had a listing debut on the Indian bourses with a 53% premium over issue price and was oversubscribed by 154.7 times the number of shares. Institutional houses allegedly started panic-selling the very next day, which didn't fool Dalal Street: they correctly read the positive fundamentals of a debt-free and heavily specialized company that's been around for nearly a quarter-century. As a result, traders and retail investors bought up premium-value shares at a discount and were heavily bullish on the stock. In fact, as of July 18, the stock is down by only 7% relative to its listing price despite market conditions in the year till date.

Given the NSIM representatives’ considered opinion that the Indian market is a developed securities market, these two instances (among others) support the notion that the majority of its participants (largely) follow highly-nuanced objectives. The institutional selling activity from “MapMyIndia” example also showcases a critical aspect of the dynamics within the market microstructure: transaction volumes on a intraday/daily traded basis affects trajectories and valuations over the mid- to long-term horizons. While Western exchanges and regulators are loathe to address this issue, the East - to paraphrase Tovarisch Fyodor Ivanovich Sukhov in “White Sun of the Desert” (Russian: Белое солнце пустыни) - is a different matter.

Delineating Algo Trading: Separate and Not Necessarily Equal

As highlighted in Part 2, Indian regulators often seek opinions and signal their focus on important matters via “consultation papers”. One such paper that created a flutter in news media was published by SEBI in December last year titled “Consultation Paper on Algorithmic Trading by Retail Investors”.

The challenge said paper was addressing pertained specifically to the wealth-generation potential of the ascendant republic’s public companies:

…unregulated/unapproved algos pose a risk to the market and can be misused for systematic market manipulation as well as to lure the retail investors by guaranteeing them higher returns. The potential loss in case of failed algo strategy is huge for retail investors. Since these third-party algo providers/vendors are unregulated, there is also no investor grievance redressal mechanism in place.

Hence, in order to make algo trading safe for retail investors and also to prevent market manipulations, it is felt that there is a need to create a regulatory framework for such algo trading.

In the proposed measures to this problem, the Working Group constituted by SEBI proposes:

All algos run by clients must be approved by the Exchange, tagged with unique IDs and hosted on Indian brokers’ servers.

SEBI makes an interesting delineation here: it ostensibly states that it doesn’t consider the broker’s order fulfilment algorithm to be an issue. Instead, it addresses the easy (and often free-of-charge) availability of their APIs to their clients. SEBI notes that while brokers can identify which orders are emanating from an API, they are unable to differentiate between an “algo” and non-algo order emanating from said API. SEBI defines an “algo” to be “one that decides when to buy or sell based on a strategy” and seeks that such strategies be approved by the exchange prior to deployment.Developed and approved algos, by virtue of running on the broker’s server, accords the latter control over client orders, order confirmations, margin information etc. Brokers must have adequate checks in place so that the algo performs in a controlled manner.

It bears noting that this is not a sudden development: consultation papers going back over nearly a decade have been used to enhance the regulator’s understanding of this space to an extensive and exhaustive degree. For instance, one such paper in 2018 sought comments about the regulator’s observations that “algo trading is characterized by high daily portfolio turnover and high order-to trade ratio (OTR). High order to trade ratio naturally raises concerns regarding order flooding, clogging of the pipeline carrying orders to the trading engine, denial of opportunity to other traders to be in front of the order book, etc.”

Comments and feedback on the December paper were required to be submitted by the middle of January this year and it can be assumed that deliberations are underway. Given the several years that SEBI has spent on developing its view on this matter, it’s an even bet that rules will be announced soon.

In Conclusion

Without an extensive analytical framework applied on Tick-By-Tick (TBT) transaction data, it’s well-nigh impossible for those outside of SEBI to even theoretically quantify the effects that “algo”-driven speculative activity might have had on stock valuations. So, let’s try a broader view.

As highlighted in Part 2, the country - and its thousands of enterprises - are broadly in growth phase; thus it should make sense that the forward outlook should be favourable. A quick survey of some of the top-of-the-line publicly-traded companies in the U.S. and India reveals a rather interesting pattern:

* US data was pulled as of 31st of Dec and Indian data was pulled as of 3rd of Jan.

Now, this is a rather limited selection but it does give a quick “feel” for the broader equity markets known to many Indian market investors; namely, that the overall Indian equity market is relatively more bullish, particularly in recent years.

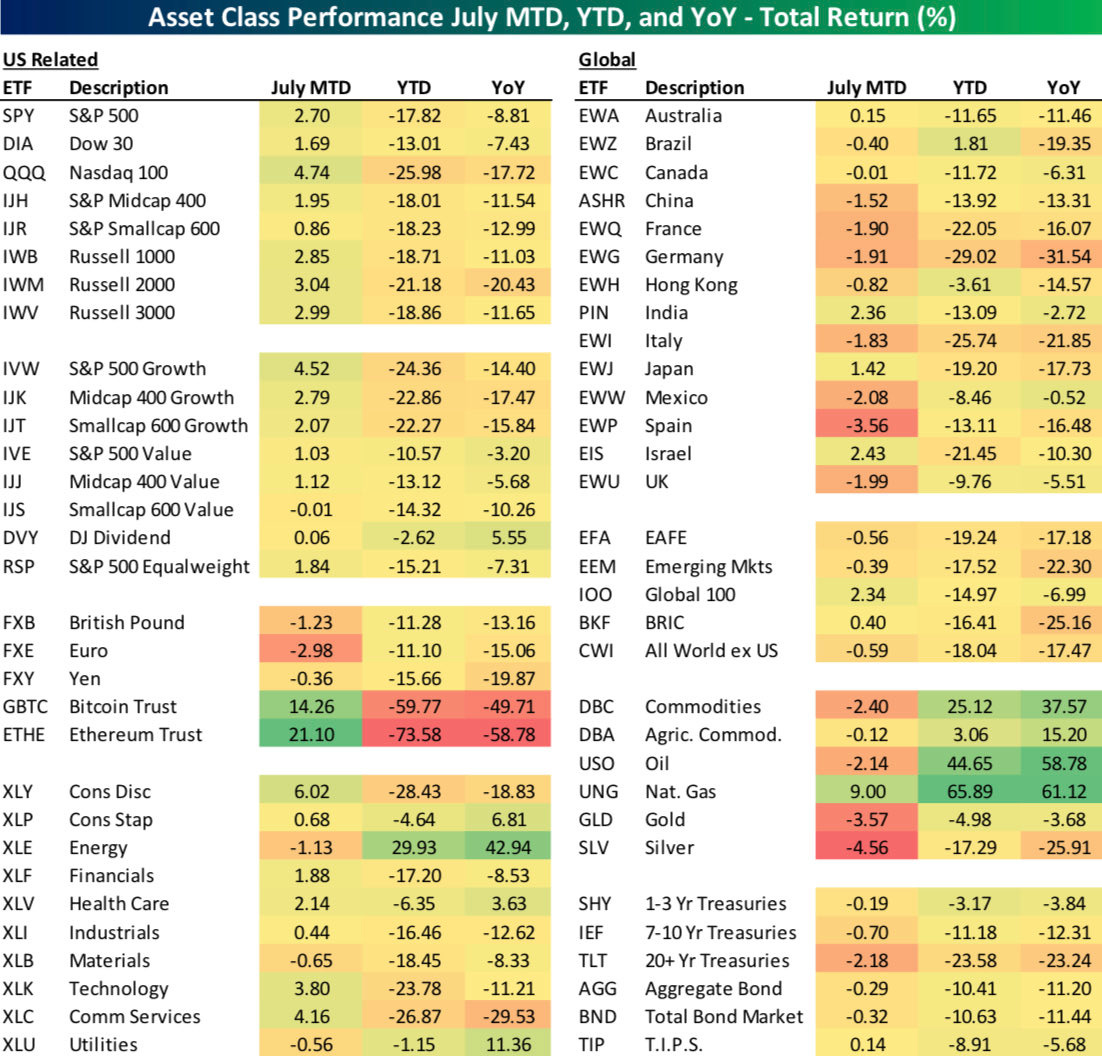

This is borne out by the strong Year-on-Year (YoY) performance that Indian market has shown till June relative to every other major market, except Mexico:

The NSIM representatives’ comments - rather tactfully - indicated that “exogenous factors” cause FPI outflows not just from Indian markets but other Emerging Markets (EM) too. This highlights a crucial limitation of all but the most trenchant of EM investors: if said investors are incurring losses elsewhere, they shall cover the same by exiting other holdings. However, as seen in the trends, the trenchant ones reign supreme outside of India’s cash market. Within the cash market, it’s likely that “day traders” (or “algos”) have had deleterious effects that might vex investors who have made a well-considered bullish stand over the course of years.

As stated earlier (and seen in a slightly different manner in the article on Chinese markets), in the East, national objectives matter more than the message of “caveat emptor” prevalent on participants in Western exchanges. One can’t help but wonder if the valuation deltas shown above wouldn’t be better on Indian equities if “day trader”/”algo” mechanics were more governed. If they were better governed, this would be a portfolio boost for the ever-growing numbers of India-focused investors, both within and overseas, both retail and institutional.

Thus ends the “Great Delink” series. There is a lot more to the East than meets the eye and few places more mysterious yet misunderstood as the vast republics of India and China. Coverage on other matters of interest will be coming soon!