Korea's EcoPro Has a "Tesla Stock" Problem

Korea's EcoPro Has a "Tesla Stock" Problem

Much like with the EV carmaker's stock, popular narratives delink the stock's valuation from the underlying company's fundamentals.

An article I wrote for the Korean edition of Investing.com discusses problems within the “K-Battery” sector’s valuation. During the prep, the article’s translator wondered if the tone should be that of a “hyeong” (형) or a “seonbae” (선배). I very helpfully suggested “oppa” (오빠) which was completely disregarded. The translator went with “ajeossi” (아저씨). Oh well. Click here for the Korean-language article. Here is the English-language version.

EcoPro’s EV battery subsidiary EcoPro BM is literally going places. The first phase of its factory in Hungary’s Debrecen is scheduled to complete by the second half of 2024; when complete, it in the second half of 2024, and the second phase a year later. When complete, the plant can produce 108,000 tons of cathode material that will be used by the Samsung SDI battery factory (located nearby) to make batteries for 1.35 million EVs (“Electric vehicles”) per year. It is also set to begin production in a new plant in Canada is expected to begin production via a Canadian subsidiary in the second half of 2025.

The stock’s performance in the course of this year, however, is running far ahead of long-term outlook and macroeconomic factors.

The Bigger Picture

Cathodes make up about 40% of a battery cell and are one of four key materials used to make them; the other three are anodes, separators and electrolytes. The cathode accounts for up to a third of a battery cell’s cost, with EV battery packs typically ranging in cost from $10,000-$12,000.

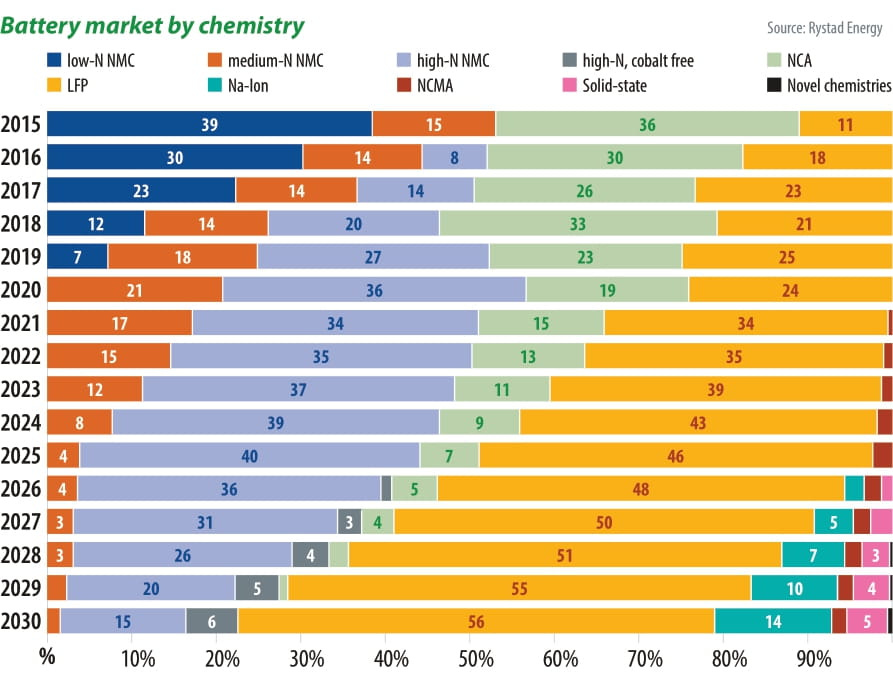

Currently, EVs run on lithium ion batteries — mostly made with lithium, cobalt, manganese and high-grade nickel. Cobalt, once a dominant element for the production of batteries, have significant supply chain bottlenecks: nearly 75% of the world’s cobalt are mined in the Democratic Republic of Congo, and over 70% of it is processed in China. Due to its relatively high cost and scarcity, the overall consumption outlook for lithium cobalt oxide (LCO) batteries is bearish, with cobalt-free lithium-iron phosphate (LFP) expected to become the dominant chemistry in the medium term.

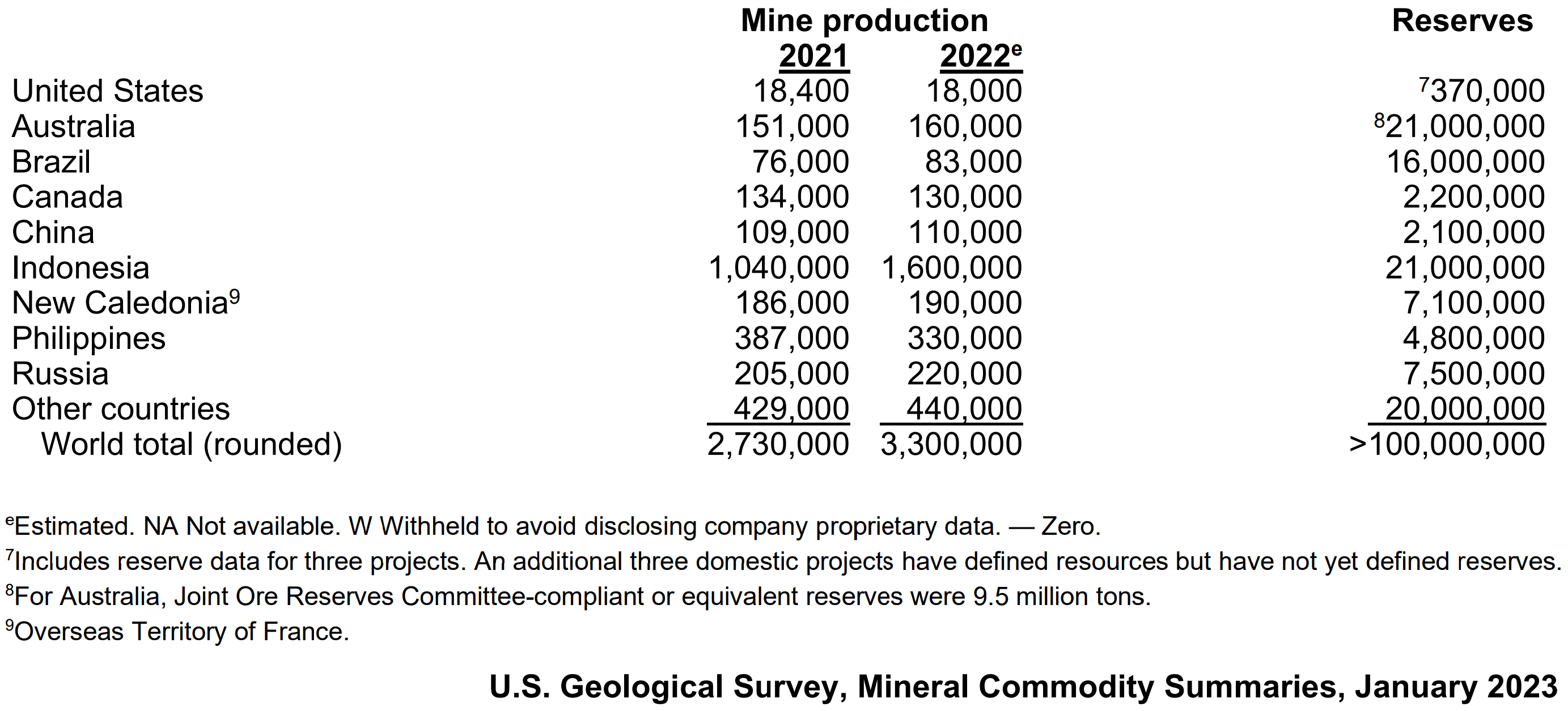

With cobalt increasingly relegated to consumer electronics, nickel — which is relatively more abundant — has been rising in importance and usage. Indonesia, Philippines and New Caledonia are the estimated to have the largest production volumes, with Brazil and Australia expected to become major sources in the near future.

Samsung SDI, a key partner for EcoPro BM, currently produces “Gen.5”, a high-nickel content battery featuring a nickel-cobalt-aluminum (NCA) cathode comprising of 88% nickel. It plans to mass produce a number of high-nickel content products such as the Gen.6 (91% nickel content) from 2024, the Gen.7 (94% nickel content) by 2026 and an all-solid-state battery by 2027. EcoPro BM’s North America partner SK On (the world’s fifth-largest electric cell maker) already produces the NMC9 battery with 90% nickel content for Ford’s all-electric F-150 Lightning, with the next-generation NMC9 planned to take the nickel content up to 98% by 2029.

It bears noting that none of these are completely free of cobalt. Nickel-based cathodes are capable of storing more energy but the materials used (i.e. nickel and cobalt) are more costly. LFP cathodes, on the other hand, typically don't hold as much energy but are safer and tend to be less expensive owing to the more-abundant materials being used. China’s SVOLT has been bridging the gap between the two extremes in some way via its proprietary cobalt-free nickel-manganese (NMX) battery cells that have recently commenced serial production. Some analysts predict that the market share of cobalt-free chemistries, on a GWh demand basis, will increase from 30% in 2022 to 57% by 2030.

The high cost of cathode materials such as nickel and cobalt is widely considered to be a limiter to addressable market growth, especially in the build-out of stationary power storage solutions and budget EVs. The spike in LFP batteries is at least partially attributable to the steadily growing market share of the latter.

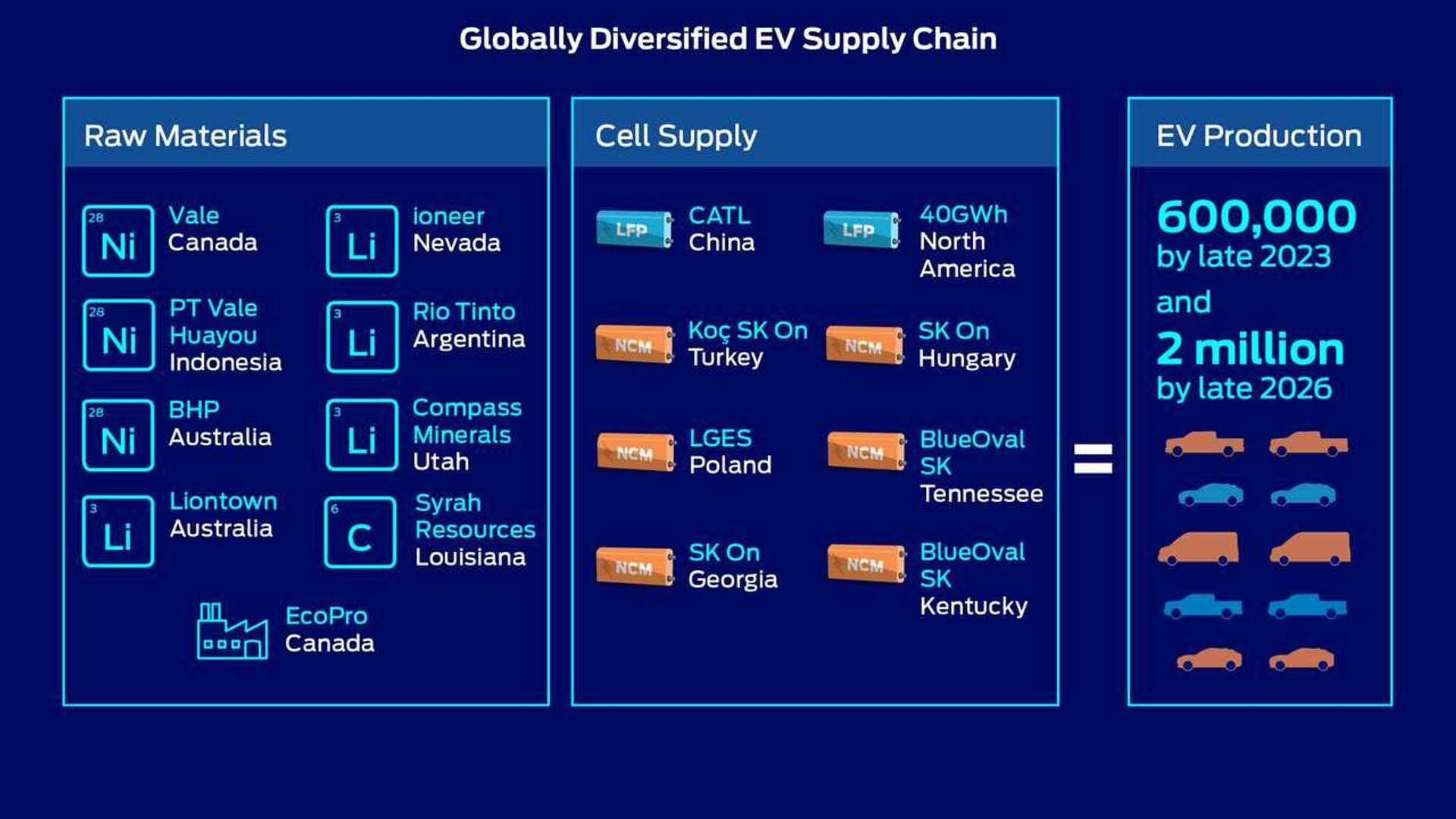

It could be argued that the likes of Samsung NDI, SK On and EcoPro BM building production facilities outside of their homelands is reflective of growing demand. However, on a realistic basis, cost of labour tends to be lower in Asia while adding on production lines to existing facilities tend to be cheaper propositions. The European Union had announced the approval of €2.9 billion in subsidies in 2021 (following €3.2 billion approved in 2019 across seven countries) in a bid to boost its share of world world battery cell production from the present-day 3% to 25% by the end of the decade, thereby ending its reliance on Asian imports. EcoPro BM’s Hungary plant has also been approved a subsidy under this scheme, the details of which have still not been published. Similarly, under the provisions of the recently-passed Inflation Reduction Act in the U.S., EVs using batteries produced in Canada — a country with which the U.S. has a free trade agreement — would be eligible for a subsidy of up to $7,500.

It’s also pertinent to note that Ford is the biggest driver of SK On and EcoPro BM’s work in North America but Ford isn’t strictly bound to their output. By late 2023, Ford plans to have enough battery supply so that it can support the production of 270,000 Mustang Mach-Es, 150,000 Transit EVs, 150,000 F-150 Lightnings, and 30,000 units of a mystery all-new midsize SUV destined for release in Europe.

In an approach similar to that of Tesla, the company is adding LFP batteries made by China’s Contemporary Amperex Technology (CATL) for the Mach-E in 2023 and the F-150 Lightning in 2024. These will be available as an option alongside existing NCM batteries. While Ford currently sources its batteries from SK On and is even building EV battery assembly plants in Kentucky and Tennessee with them, it has entered into a separate non-binding Memorandum of Understanding (MOU) with CATL to “explore a cooperation” for building batteries across China, Europe, and North America. A $3.5 billion battery plant with CATL-licensed technology in Michigan can be assumed as the first step in this MOU. When complete in 2026, this will have an annual capacity of battery packs for 400,000 EVs. Critically, the $7,500 subsidy is available for vehicles with these non-nickel batteries as well. In essence, the benefits of EcoPro BM’s investments are very much dependent on consumer buying choices, with Ford essentially free to pivot in any direction.

Work continues in the replacement of nickel-based cathodes altogether as well. EVs arriving after 2025 could potentially shift to sodium ion or lithium sulphur battery cells that could be up to two-thirds cheaper than today's lithium ion cells if certain technological breakthroughs are achieved. Sodium ion batteries don't yet store enough energy, while sulphur cells tend to corrode quickly and don't last long.

Nonetheless, CATL has said it plans to begin producing sodium ion cells in 2023. Korea's LG Energy Solution aims to start making lithium sulfur cells by 2025. Michigan-based Amandarry and British startup AMTE Power are developing sodium ion batteries using sodium chloride (i.e. “table salt”) as the main cathode ingredient and completely free of lithium, cobalt or nickel. U.S-based Lyten and Conamix, Germany's Theion and Norway's Morrow are developing lithium sulphur cathodes that need small quantities of lithium but not nickel or cobalt.

Recent discoveries are closing the gap on issues like energy density and cycle life, lending to the expectation that sodium ion or lithium sulphur batteries taking market share in the near future. These alternatives are rapidly closing the gap in terms of feasible energy densities.

UK-based Faradion stated that its sodium ion batteries are also already competitive with LFP cells and it has formed a joint venture for energy storage with agribusiness giant ICM Australia. India’s Reliance conglomerate purchased Faradion for £100 million in January 2022.

India’s participation in the battery race is quite understated at the moment due to the relatively low penetration of EVs in the car market. However, sales of electric 2-wheelers (E2Ws) have been witnessing double-digit percentage growth for over two years now. With green energy investments intensifying and infrastructure being laid out, this is a substantial growth opportunity for Korean battery tech giants. However, the technologies of producing cathodes with a nickel content of over 80% are classified as among 75 key technologies under strict government control due to their technological and economic value, as well as the growth potential of the semiconductor, electrical and electronics and steel sectors.

Much like SK On and EcoPro, POSCO Chemical Co. has pursued cathode plant expansions via joint ventures with General Motors in Canada as well as with Huayou Cobalt in China. POSCO is conceivably seeking to establish vertical integration with mineral supplies in Canada, much like EcoPro, SK On, Ford, etc. since Canada has the world’s second biggest reserves for nickel, while the country’s cobalt production is the eighth largest worldwide. In India, POSCO has already inked a $10 billion deal with India’s Adani conglomerate to set up a variety of projects covering renewable energy, hydrogen, and logistics early last year. The company also operates a 1.8-million-tonne cold-rolled and galvanized mill in the western state of Maharashtra. Significantly, earlier this year, POSCO Chemical secured permission to transfer the technology to design, manufacture and process cathode materials used in high-nickel batteries to its overseas plants earlier this year. Whether this translates to a nickel cathode plant in India remains to be seen.

It’s certainly not possible to establish vertical integration with cathode material minerals in India: outside of some laterite deposits of nickel in the eastern state of Odisha, the country doesn’t have substantial reserves of either cobalt or nickel. However, the republic’s doctrine of self-reliance (“aatmanirbharta”) creates grounds for innovation: India’s Epsilon Carbon — India’s leading producer of graphite materials for lithium-ion battery anodes — has entered into a MOU with U.S.-based The Metals Company (TMC) to explore means of producing 30,000 tons per annum of product usable NMC and other nickel-rich cathode chemistries via a commercial-scale deep-sea nodule processing plant in India. This will be the first plant of its kind in the world, if found feasible.

Towards the end of June, the Indian government identified a list of 30 “critical minerals” that it intends to encourage public and private investments in as well as facilitating the adoption of advanced technologies and international collaborations. Nickel, cobalt and lithium feature in this list — thereby implying the possibility of subsidies and other production-linked incentives being unveiled soon.

Given that — unlike EcoPro BM, SK On, etc. — POSCO already has infrastructure and deals in place, this could be an advantage for both POSCO at the cost to those not involved right now. However, production-linked incentives typically require a transfer of technology to an Indian partner. How the Korean government maneuvers and fosters the entry of Korean companies here remains to be seen.

Down to Brass Tacks

Outside of cobalt, nickel — despite being relatively more expensive — hasn’t shown quite as much historical price performance volatility as lithium carbonate has.

Therefore, in terms of raw material costs, EcoPro BM isn’t expected to face a significant cost challenge. The challenge, instead, rests on technological longevity. Given that substitution potential is high in the mid- to long-run, the forward financial ratio outlook ideally shouldn’t be disproportionate.

Examining the performance of EcoPro BM’s three primary financial ratios — Price to Earnings (PE), Price to Sales (PS) and Price to Book Value — versus volumes traded yield some interesting insight.

High volumes traded since the end of 2019 had propelled the stock’s PE Ratio into the triple-digit range, with subsequent lesser spikes pushing it even further in Q3 2021. Large volumes continue to have the same effect since then until the present day. While the PB Ratio remains elevated, the PS Ratio has been rather low. This leads to the conclusion that earnings and book value aided by expansions are leading to an overstating of trajectory as compared to the company’s revenues.

A similar phenomenon is seen in a more extreme fashion in the parent company’s stock.

In the present (as of Monday), Price Ratios for both EcoPro BM and its parent have been in decline for the past couple of months. There’s likely a long way to go, given that these ratios stand well above industry averages in both cases.

Key Takeaways

The problem of “irrational valuation” has been an ever-present feature of American equity markets where “buying the rumour and selling the news” has been a persistent feature. Many analysts attribute this persistence to (for example) Tesla’s sky-high valuations even at a time when EVs are increasingly comparable to ICE vehicles in terms of buyer preferences and the company facing strong competition in its U.S. market from European carmakers such as Mercedes Benz and BMW (whose U.S. YoY sales figures continue to impress) while NIO, XPeng, Li Auto and BYD are collectively doing the same in China. Overall, Asian markets tend to display far more pragmatic behaviour. This has not been the case at least as far EcoPro BM and its parent is concerned.

A case of “irrational valuation” is exhibited in the now-silent but highly influential ‘Battery Ajeossi’ Park Soon-hyeok, who argued that Korean battery companies will witness a stock price rise hundreds of times over as they become global companies. Mr. Park didn’t seem to account for the empirical observation of “deglobalization” — wherein global companies will be forced to compete on even terms with domestic companies across dominant economic regions, with the latter being given a leg up for the purposes of fostering economic health and indigenous technological growth. Mr. Park’s observations also didn’t seem to account for rapid innovation being a disruptor to the status quo. These empiricisms aren’t just impediments for Korean companies; they will inevitably affect other companies presently considered to be “global leaders”. Overall, “deglobalization” isn’t necessarily bad; it ultimately increases investor choices and rewards diligent research.

Instead, Mr. Park argued that institutional researchers have been distorting corporate valuations to benefit long-short funds. It bears noting that long-short funds aren’t always profitable. Furthermore, institutional investors have long been keen proponents of broad market instruments. Also, institutional players aren’t a council of conspirators; if one delivers a bad call, others take the other side of the bet. The actions of short players have always been central to accurate “price discovery”; not having them around leads to market distortion and catastrophic (and inevitable) downsides, which individual investors often end up paying dearly for.

By no means is Mr. Park a singular case; the conspiratorial bent is a common trope in many an online personality. While such ideas are instinctually attractive to many, they aren’t rationally explainable. As an American online figure famously (and frequently) quotes, “Facts don’t care about your feelings”.

One could also model EcoPro BM’s expected stock price in line with industry averages to derive a prospective price range over the course of the next 9-12 months that could be considered “less irrational”. The PE Ratio signifies the price an investor must pay per unit of current earnings (or future earnings, as the case may be). If the company doesn’t grow and the current level of earnings remains constant, this ratio can alternatively be interpreted as the number of years it will take for the company to pay back the amount paid for each share.

A simple model: if the current industry average of the PE and PS Ratios were to be a model for the stock’s current price, then the stock’s price range would be about ₩130,037 (PE Point of the valuation plane) to ₩236,895 (PS Point of the valuation plane). However, the entirety of the K-Battery sector has been in decline from overblown valuations for some time now.

If the “less irrational” end of the price spectrum were to assume a PE Ratio of 10 (the turnaround time for an alternative battery chemistries to become prevalent) and a PS of 3 (the premium paid by investors per unit of revenue), the price range becomes ₩25,308 - 184,115. Adopting the inner band of prices between these two ranges (and rounding out) yields the “median range” of ₩130,000-184,000 and an “all-band” average of ₩144,000.

When overvaluation steps in, the stock prices witnessed are more a reflection of investor choices and less about the company’s performance (or the lack of thereof). In other words, the two are effectively divorced. It becomes incumbent upon such investors to reflect and pivot; the simple fact is that a movement towards the “less irrational” is virtually inevitable. The only question is “When?”

The correct answer can pay off or save millions.

On the matter of Korea, an earlier series compared the military aircraft industries of Korea and India (here’s Part 1 and Part 2) which highlighted several points of synergy for the two countries.

For a “Big Read” on other matters, the ever-popular “Dharma” series traces the evolution of Eastern faith and philosophy. Here’s Part 1, Part 2, Part 3, Part 4 and Part 5, followed by the ancillary Part 6 and Part 7 that discussed Malaysia and Indonesia’s spiritual history. Finally, click here for a list of all articles published.