Stablecoins: An Evolving Tool Against Remittance Costs

Stablecoins: An Evolving Tool Against Remittance Costs

Coinbase's metrics indicate potential to transform FX costs for the global diaspora

In a recent conversation with CoinDesk, I discussed Coinbase and stablecoins’ inherent potential in tapping, reducing and transforming the high costs faced by the global diaspora in transactions involving multiple currencies, including but not limited to remittances. Here’s the bulk of the background research behind my commentary. If/when they’re included in an article, it will be linked here. Read on!

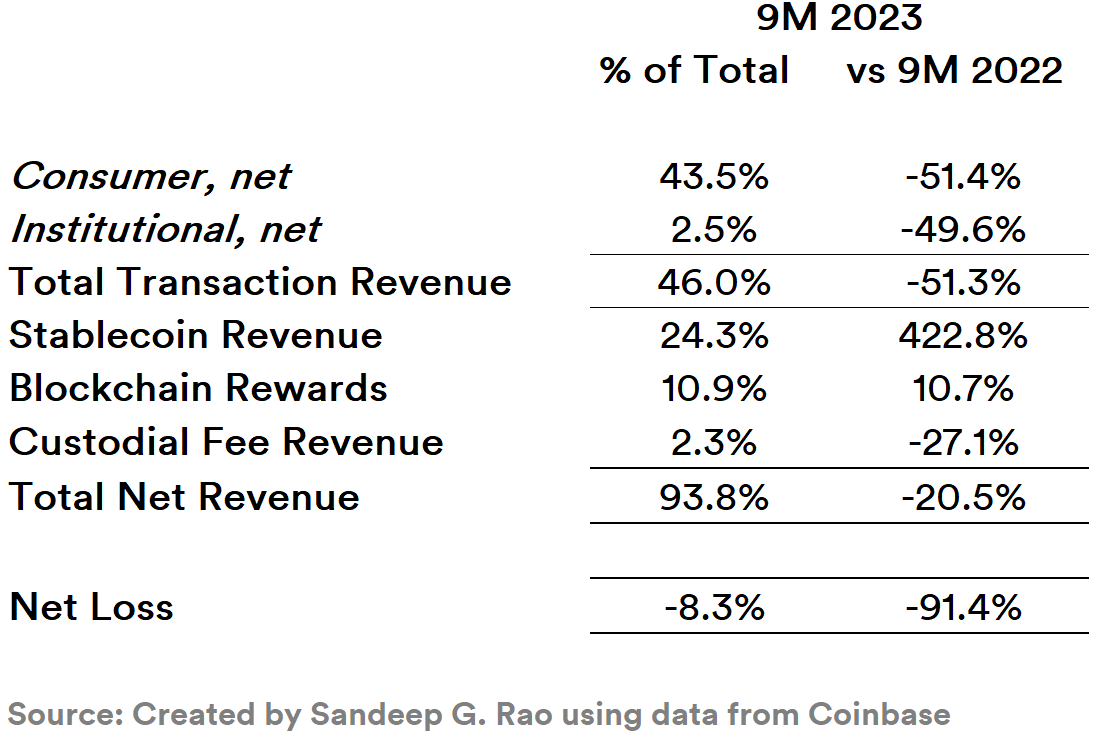

Relative to the same period last year, Coinbase has seen a 16% decline in Monthly Transacting Users (MTUs) — defined as consumers who actively or passively transacts in one or more products on the platform at least once during the rolling 28-day period ending on the date of measurement — and a 54% decline in trading volume in the 3 quarters of 2023 so far. Consumer trading volume is down 69% while institutional volume is down 50%.

Revenue and income breakdowns show a halving of transaction revenue along with a substantial reduction of net losses relative to net revenue.

While the company registered a loss in trading volume in virtually every crypto asset except for Bitcoin — wherein the share of trading volume registered a 28% increase — stablecoin USDC witnessed a 400% increase on the back of a strong dollar continuing to throttle the competitiveness of American goods and services and a flight of capital from broader equity markets into a narrow band of instruments that includes Treasury bills, high-quality corporate paper, and dollar-backed assets.

Overall, there are 5 types of stablecoins in play all over the world:

Commodity-Backed Stablecoins: Generally pegged against (and collateralized by) the likes of “hard assets” such as commodities (e.g. gold) or real estate.

Crypto-Backed Stablecoins: Collateralized by cryptocurrencies. Since the reserve cryptocurrency are generally volatile, these stablecoins are “over-collateralized”—that is, a larger number of cryptocurrency tokens is held in reserve for issuing a lower number of stablecoins.

Fiat-Backed Stablecoins: Collateralized via a fiat currency reserve (such as the U.S. dollar), they are extremely popular mainly because they are akin to a printing machine for the cryptocurrency economy. USDC is an example of this.

Algorithmic Stablecoins: Driven by algorithms to automatically increase or decrease digital currency reserves like central banks, these are vulnerable to regulations.

Central Bank Digital Currency (CBDC): Backed by a government’s central bank and akin to a banknote, they are regulated under a central authority.

Coinbase’s stablecoin business is a pretty straight-forward business with enormous potential since they imply “real world value” onto various crypto chains and is expected to continue to capture and develop interest in the future. Across the entirety of 2022, a variety of dollar-backed stablecoins has witnessed a concentration of interest — to the benefit of USDC and Binance USD (BUSD).

As of December 2023, stablecoins are already at 8% of total “alt-currency” market capitalization.

While stablecoins are estimated as being used as “off-ramp assets” by crypto players during periods of volatility, there is one key area of present relative underutilization: international payments with very low transaction fees and fast settlements.

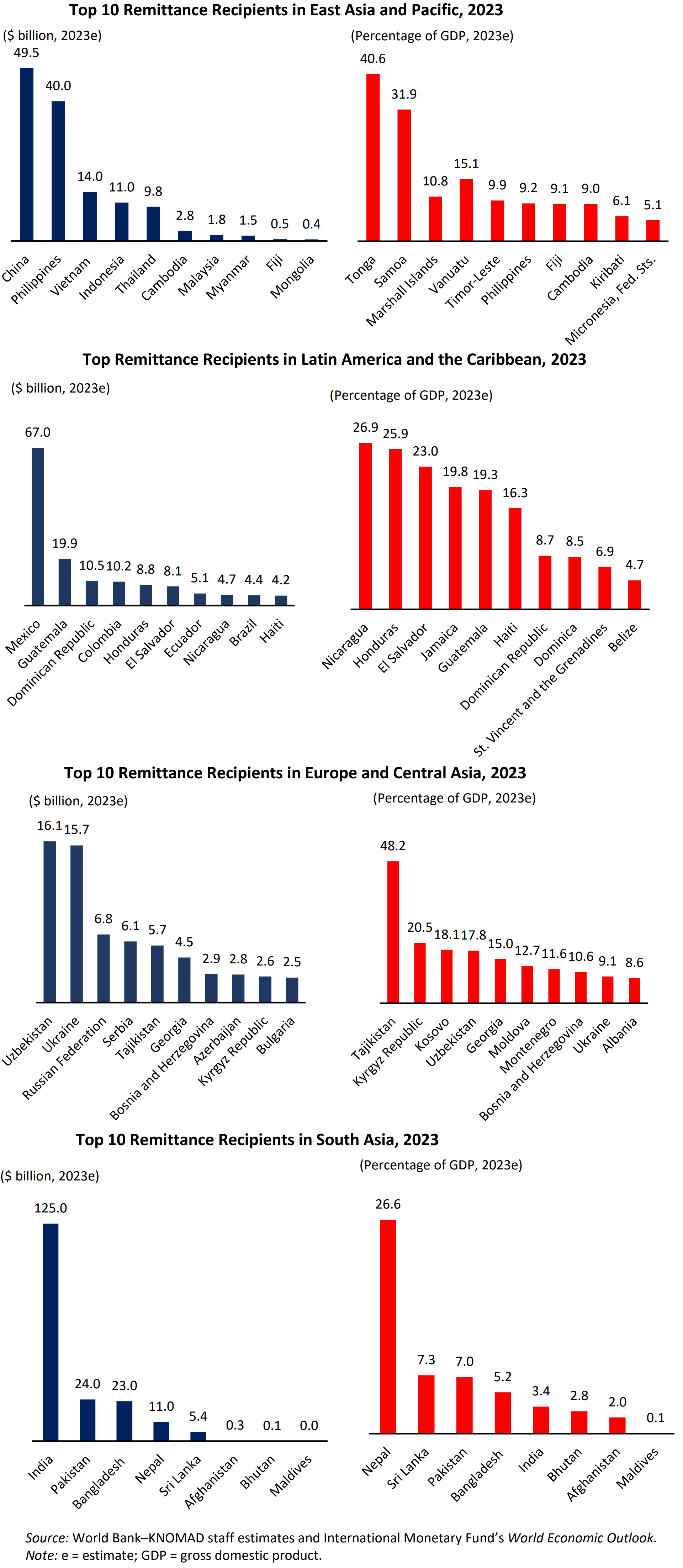

As per the “Migration and Development Brief” on Diaspora Finance released in December this year by the World Bank under the Global Knowledge Partnership on Migration and Development (KNOMAD), the top five remittance recipient countries in 2023 are India ($125 billion), Mexico ($67 billion), China ($50 billion), the Philippines ($40 billion), and Egypt ($24 billion). Economies where remittance inflows represent substantial shares of gross domestic product (GDP) — highlighting the importance of remittances for funding current account and fiscal shortfalls — are Tajikistan (48%), Tonga (41%), Samoa (32%), Lebanon (28%), and Nicaragua (27%).

However, the bank notes that, as of Q2 2023, it costed 6.2% on average to send $200. Banks continued to be the costliest channel for sending remittances with an average cost of 12.1%. The range of costs were extremely wide — with as little as 0.5% between some channels (i.e. a unidirectional payment network between two countries) and a little over 40% in others. The crux of this wide disparity in costs — and the overall dearness of said services — lies in how foreign exchange (FX) is handled.

FX trading — unlike equities via exchanges — is conducted electronically over-the-counter (OTC) via computer networks between traders situated all over the world. The market is open 24 hours a day, five and a half days a week and averages over $5 trillion in volume every day. The supply/demand dynamic that is divided between different OTC networks creates a divergence in rates between currencies that is quite different from the ‘consensus’ rate that is often quoted on a screen. On a standalone "transactional" basis, the differences may seem quite miniscule. But over the course of the massive volumes exchanged every day, these add up to a very hefty sum.

FX specialists have long held that the complexity of foreign markets are inconducive to further cost reduction or stabilization. Many proponents of Distributed Ledger Technology (DLT) – such as Dr. Markus Merz from the University of Tuebingen – have argued that complexity can be rationalized economically by the use of a shared network based on a permissioned DLT which enables an efficient and direct transfer of funds instead of relying on specialized "correspondents", i.e., intermediaries that complete transactions on behalf of banks and who add to the costs felt by the end user.

Stablecoins offer a path out for bringing out further cost optimization for the end user’s benefit. For instance, as of October this year, a $200 transfer to countries in Sub-Saharan Africa would have costed upwards of 7.8%. A similar transfer would have costed just 0.02% on an Ethereum Layer 2 network, with settlement occurring in a matter of minutes.

Coinbase’s meteoric rise in stablecoin revenues - regardless of reason - is an indicator of the inherent potential accessible. Current, the U.S. is the largest source of global remittances.

Dollar-denominated stablecoins, at the very least, could form the first leg of many FX transactions underpinning a remittance. Since CBDCs are already under development by central banks in China, India and Japan, many more CBDCs or fiat stablecoins can be expected in due time to form subsequent legs of the remittance into the desired fiat. In fact, Deutsche Bank’s DWS and Flow Traders are already working on establishing a Euro stablecoin.

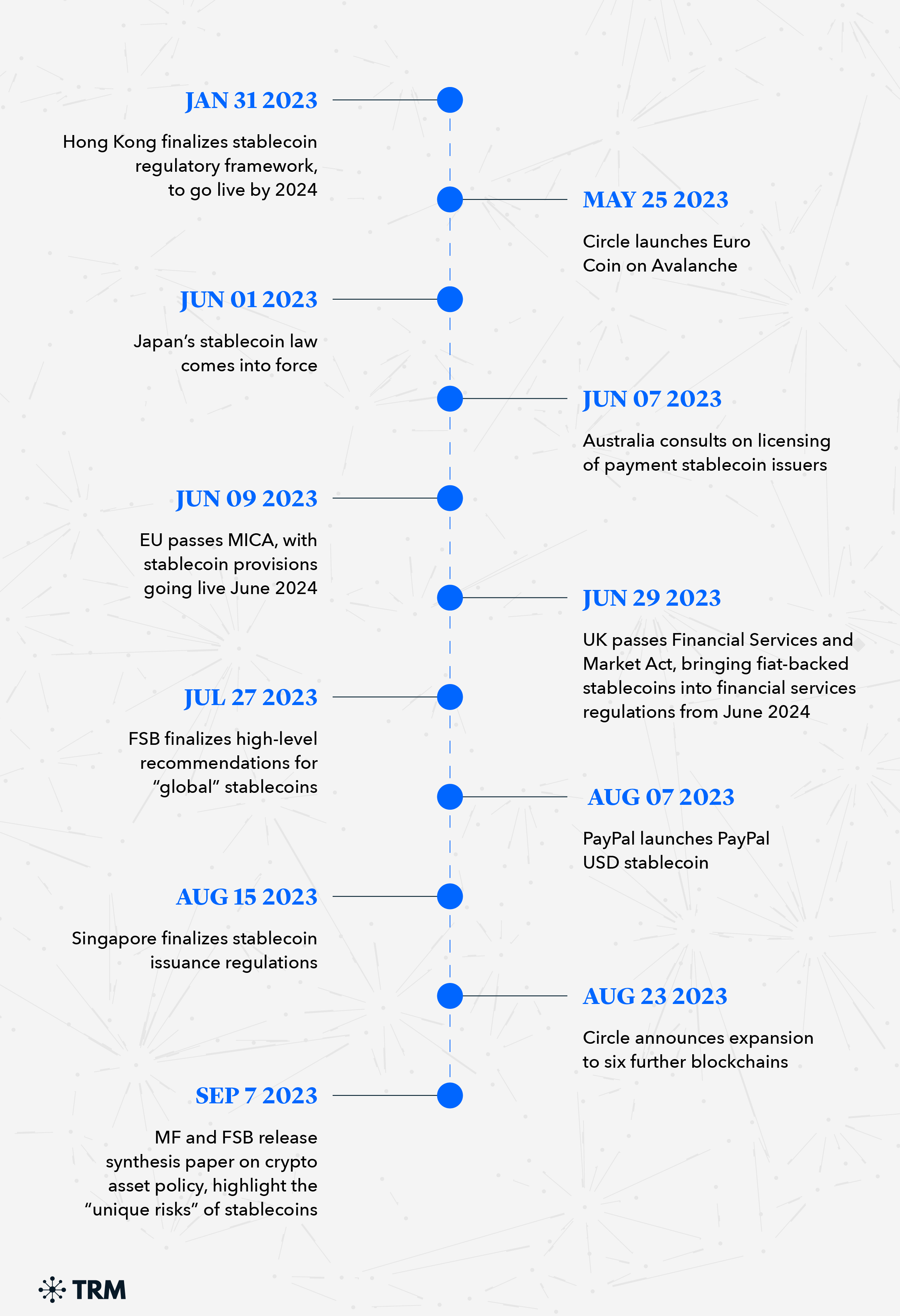

Coinbase receiving a full business license to operate in Singapore could be construed as a bid to attract international business (predominantly institutional players). The U.S. accounts for 89.5% of the business in YTD 2023, which is up from 82.8% in the same period last year. The Singapore connection might prove to be transformative for the company’s bottom line in the future. It could also become one of many key triggers that will establish cost-efficient networks for remittances to/from proximate countries in the region. As it stands, a “Stablecoin Summer” is already underway with key provisions and notifications being made by a number of regulators.

Earlier this month, the Basel Committee for Banking Supervision proposed a series of modifications to the criteria governing stablecoins such that their reserve assets have the requisite short-term maturity, high credit quality and low volatility to meet holders' expectations for redemption.

All in all, there are signs that stablecoins (and CBDCs) might gain greater renown as the bearer of new cost/processing efficiencies for the global remittance market (bringing with it a new set of players) than as an “off-ramping” asset class for the cryptocurrency market. However, rising usage patterns indicate that stablecoins are very likely to remain prevalent in the latter as well.

Note: Some of the arguments were already covered in an article I had published on Leverage Shares in late November (click here) as well as in SeekingAlpha a little over two years ago (click here).

2023 is poised to close out with the “Dharma” series — which traces the evolution of Eastern faith and philosophy — remaining the best-received articles so far. Here’s Part 1, Part 2, Part 3, Part 4 and Part 5, followed by the ancillary Part 6 and Part 7 discussing Malaysia’s and Indonesia’s spiritual history.

Click here for a list of all articles ever published.