Big Tech's Q3: Observations Made to Media

Big Tech's Q3: Observations Made to Media

Musings on the forward-looking outlook for Tesla, Microsoft, Amazon and more.

Over the past month, I’ve had a number of conversations with journalists from Reuters about ideas their desk was exploring. Given these ideas’ exploratory nature, it’s uncertain if they will be included in a finalized article. If they do, they’ll be linked here. Until then: here is the expanded background for my commentary, dear reader!

Late October 2023: Observations on Tesla as well as other EV companies

While new car sales have been falling YoY in the U.S. for nearly a decade now, sales of NEVs (“New Energy Vehicles”, of which EVs are a massive component) have been consistently rising. In the U.S., Tesla traditionally held a lion’s share of EV sales. However, Tesla’s market share is down from nearly 65% in 2022 to about 50% as of Q3 this year. This is despite the fact that Tesla has delivered as many vehicles in 9M 2023 as it did in the entirety of 2022. Overlaying the two data series together, it's clear that the U.S. EV market is growing and has an increasing number of players. As of Q3 this year, BMW, Mercedes and VW had witnessed over 265%, 145% and 338% growth in Year-on-Year (YoY) sales. While Toyota, Honda and Kia have smaller growth rates relative to the German carmakers, they have substantial potential to successfully deploy their EV offerings in the U.S. as well.

While American “pure play” EV carmakers Lucid, Rivian and Fisker are offering a variety of models around the same price range as the Model S/X (as do the three German carmakers), the non-Tesla Americans haven't registered nearly as much growth. Since these cars are primarily bought by buyers in the “premium” consumer segment, German carmakers have an advantage: they have been in the business for nearly a century, have long-established technical achievement high watermarks and also employ a number of luxury marques for brand distinction. Unlike its American compatriots, Tesla has a distinctive “first mover”/”legacy brand” advantage. However, while it has been in the business for a decade now, it doesn't have a luxury marque yet.

Longevity in the business, an established history of catering to “premium” segments, and the introduction of EV models that have already been doing well in similar consumer segments across Europe and Asia give the Germans a distinctive advantage over Tesla and a massive one over Lucid, Rivian, et al.

Furthermore, Lucid, Rivian and Fisker don't have as extensive a dealer and service network as the German/Japanese/Korean carmakers do or even Tesla (for that matter). This weighs against them in gaining traction. It isn't merely enough to produce an “EV that works” when dealing with “premium” segments; a pedigree of achievements is key. Legacy German/Japanese carmakers have this in spades. In the S/X segment, Tesla's deliveries are running under par relative to 2022. Overlaying this with German sales trends in the U.S. suggests that “premium” segments are identifying strong value propositions from German carmakers.

There have been some commentary that Fed rates being higher for longer would hurt EV sales in the U.S. These concerns aren’t completely off the mark when it comes to Tesla, which has been selling the diminutively priced Model 3/Y like hot cakes. The associated buyer demographic could be considered as the equivalent of a “basic” consumer segment which will likely be hurt more if Fed rates stay high, since auto loan rates will also stay high (or even climb). The “premium” segment, however, isn’t nearly as sensitive to financing difficulties — which both German carmakers and the likes of Toyota, Honda and Kia will likely continue to cater to, at cost to the likes of American EV carmakers.

Rates remaining higher for longer also is an impediment for non-Tesla American EV carmakers. Dividing Lucid’s current losses by the number of cars it has sold so far, losses stand at nearly half a million dollars per car delivered. It's likely that Lucid, Fisker and possibly even Rivian will try to secure financing via paper issuances. This will be a costly affair since the effective interest rate of said paper should beat both Treasury issuances and offer a “premium” for being unsecured with shaky free cash flow trends. Tesla, meanwhile, does have substantial free cash flow (albeit reduced in 2023) that will cover a large part of its “Gen 2 platform” groundwork. However, a bond issuance isn't completely out of bounds in 2024.

Mid-November 2023: Observations on Big Tech: cloud businesses and digital ad spends

In Q3 2023, Microsoft beat expectations in Intelligent Cloud and Business Processes by a 2-3% margin. With Azure-driven revenue growing 29% from the prior year and Oracle committing to making its databases available on Azure, the company has a strong opportunity in capitalizing on ongoing modernization of legacy businesses; for example, 85% of the Fortune 100 companies already use Azure AI. Microsoft has committed to boosting GPU capacity and utilization, which means that a growth of Azure revenues by 27-29% over the next year isn’t out of the question.

Azure's developing suite of best-in-class open-source AI models will also prove to a draw for startups and digital-first businesses who would find value propositions in being “upsold” cloud solutions. This is in addition to OpenAI platforms ChatGPT and DALL-E getting deeper embedding in all of the company' various offerings.

While Azure holds about 23% of the cloud market leader, they trail Amazon’s AWS which is at 35%. Unlike with Microsoft — a ready-made bridge between AI and cloud isn't available to AWS customers, despite the bedrock of America's corporate cloud essentially being AWS solutions. Amazon’s entry into the generative AI space in April 2023 could be considered a late start. However, the company's recent tie-up with Anthropic gives it a potentially interesting “regulatory” edge over the ever-popular OpenAI models: “safety”. The E.U. passed the AI Safety Act that is intended to be implemented before June 2024 while the White House has recently issued an executive order on “Safe, Secure, and Trustworthy Artificial Intelligence”. Given that some observers have noted that Anthropic's Claude AI is observed to as being less likely to give wrong answers and less susceptible to jailbreaking — in contrast to ChatGPT — there are definite grounds to assume that the AWS-Anthropic partnership could be an opportunity in an evolving market. Amazon Bedrock already offers pre-trained language models from a variety of third-party companies; so it's fair to conclude that these two companies will be running neck and neck in the “AI + Cloud” market.

An interesting factor to consider would be the “anti-trust” principle. Both companies are American while business is global. With American companies facing rising competition in pretty much every sector from companies all over the world — particularly China and India — there is ample scope to assume that an America-centric corporate oligopoly in a key sector won't fly for very long. If an anti-trust-driven impetus is given to amplify indigenous companies in the “AI + Cloud” market, both companies are looking at an upward ceiling on overall long-term growth.

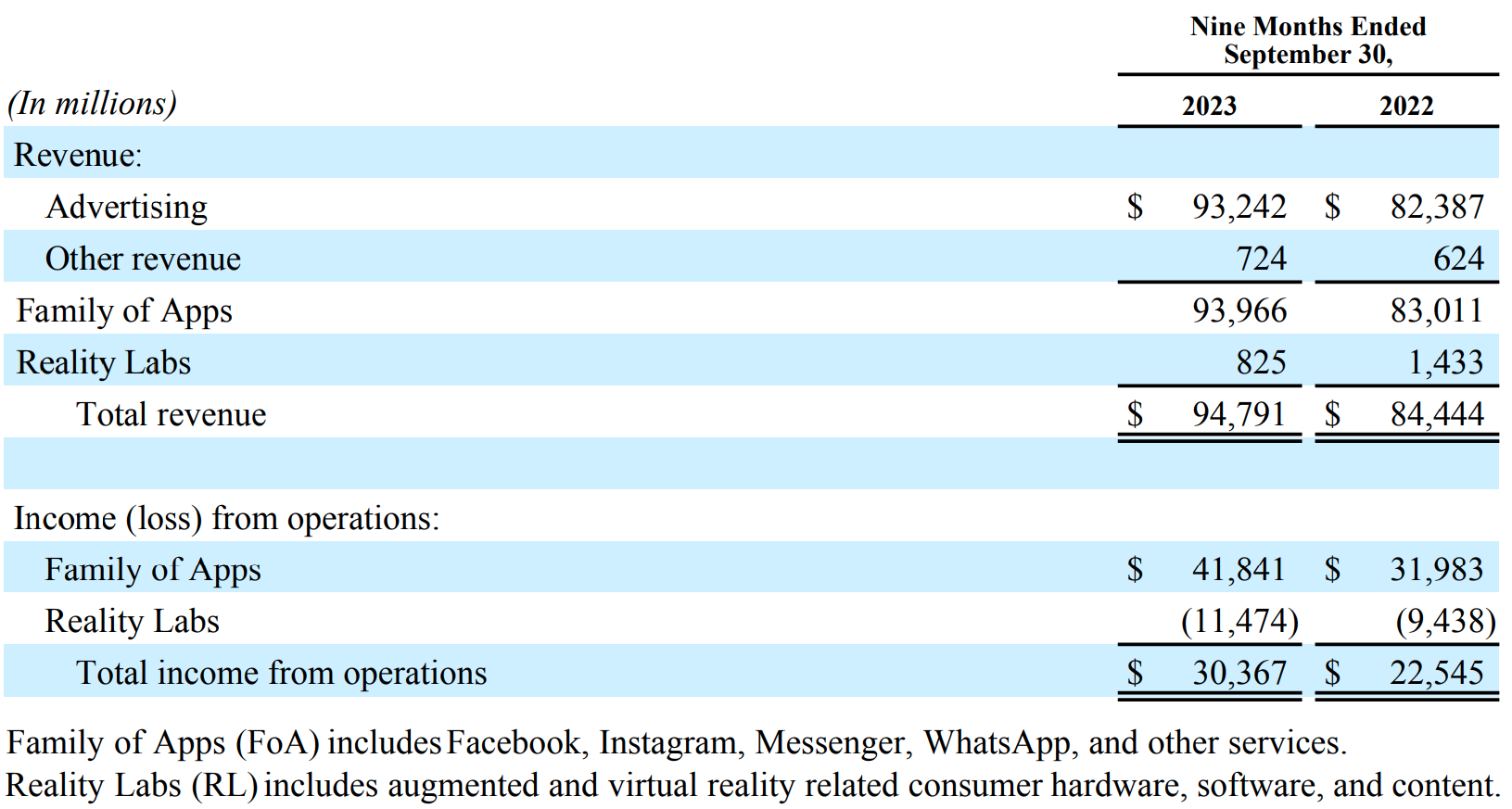

Now, with regard to Alphabet Inc. (or “Google”): Search and YouTube ad revenues were up 6% and 5% respectively in 2023 YTD versus the same period in 2022. This was achieved despite a 5.3% decline in its advertising network. Revenue by region is relatively unchanged.

Note: Google Cloud revenues, on the other hand, was up 26%. Like with Amazon, coming in late doesn’t mean a significant hurdle for growth due to rising demand.

In contrast, Meta (or “Facebook”) has registered more than 13% increase in revenue via its apps over the same period last year.

While Meta’s (this name does not roll off the tongue easily) ad revenues are decidedly lower than that of Google, the value of having “engagement” cannot be overstated. It also suggests that attention via social media apps is increasing on a per-minute basis. If the monetization of “engagement” can be done via “influencers”, it could be argued that Google has a higher potential for doing so via YouTube; both Google and YouTube are the world’s first- and second-most visited websites globally.

Of Meta’s FoA, it can be seen that Facebook trends higher in age while Instagram trends lower in a key region such as the U.S.:

This trend largely holds true in other Developed Markets (DM) regions such as Germany (for example):

The overall age of the average Facebook user, however, trended downwards going from DM to Emerging Markets (EM): the average U.S. Facebook user in the U.S. was 40.5 years old in 2013 while it’s 29 years old in Lebanon. With a growing footprint in EM countries since then, this average has trended downwards: today, 18-34 year-olds make up around 55% of all users. It could be argued that DM users are more likely to buy into ads via engagement with “influencers” than EM users. In terms of age demographics, however, Meta has it all covered via its FoA.

The idea of selling via “engagement” is certainly not out of the question, which brings into the forefront the Amazon-Snapchat deal. Given that TikTok Shop ostensibly provides a strong platform for sellers to target younger millennial and Gen Z users and that Snapchat users trend relatively lower in age relative to Meta’s FoA, the deal has both the potential to be transformative and synergistic for both companies’ revenues. (Of course, Amazon already has similar deals in place with both Facebook and Pinterest — which means the former has covered its bases quite nicely.)

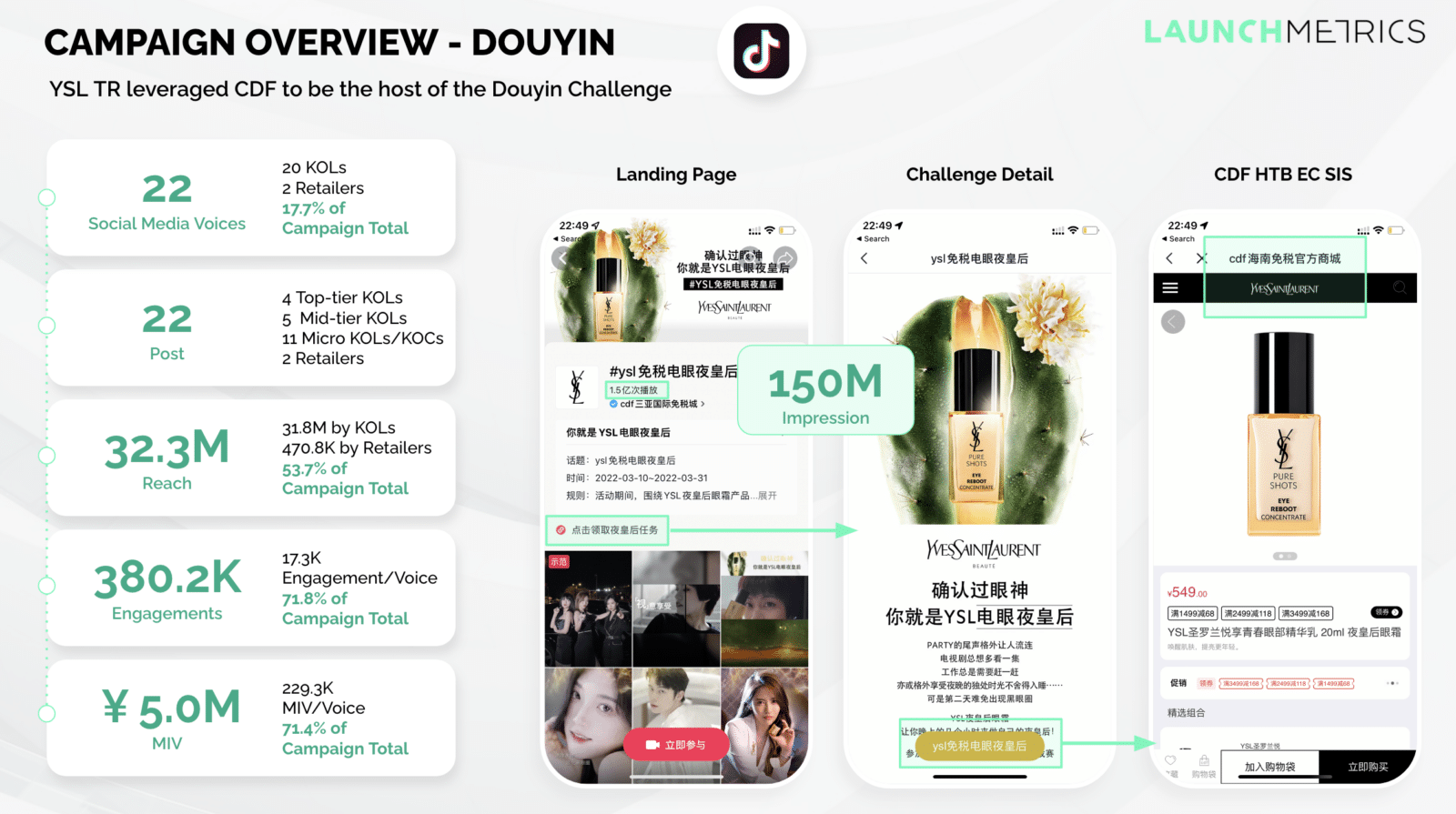

It’s very likely that any U.S./DM-centric strategizing is at least partially driven by “Key Opinion Leader (or KOL) marketing” success stories in China; “KOLs” are Chinese influencers. In this highly-networked part of the world, Douyin has been on the rise in recent years and giving chase to WeChat in terms of reach (which currently remains #1). However, it has been stated that Douyin has proven to be more effective in “moving product”: for instance, recent news indicated how one particular KOL earned $13.7 million in sales in 7 days via a promotion lasting only 3 seconds per product. Another marketing company reports achieving 150 million impressions for Yves Saint Laurent (YSL) using a blended approach using both KOLs and retailers on Douyin.

Speaking of EMs, “EM King” India has been covered a lot over the current year. Click here to read more on overall macroeconomic trends that point to the coming few years becoming “New India’s” decade. Click here for a list of all articles published, India-centric or otherwise.

For a “Big Read” on other matters, the ever-popular “Dharma” series traces the evolution of Eastern faith and philosophy. Here’s Part 1, Part 2, Part 3, Part 4 and Part 5, followed by the ancillary Part 6 and Part 7 discussing Malaysia’s and Indonesia’s spiritual history.