India's Economy: Shackles Off, Marching Upwards

Decomplexifying regulations and rising competencies highlights growing maturity within the world's most populous (and arguably oldest) nation.

Many asset managers play a zero-sum game in asset allocation strategy: an outlook on Developed Market (DM) economies rising is automatically assumed to imply that Emerging Markets (EM) economies will fall (and vice versa). In macroeconomic terms - backed by empirical observations throughout history - this is simply not true. The greatest case in point in the present (and arguably even in the past) is India.

Presumably much to the chagrin of amateur India-watcher “permabears” among the global commentariat, the International Monetary Fund (IMF) estimates that the Indian economy’s GDP in real terms will display a growth rate to outstrip that of most Emerging and Developing Asian countries as well as that of all Advanced Asian countries over the course of this year and the next (at least):

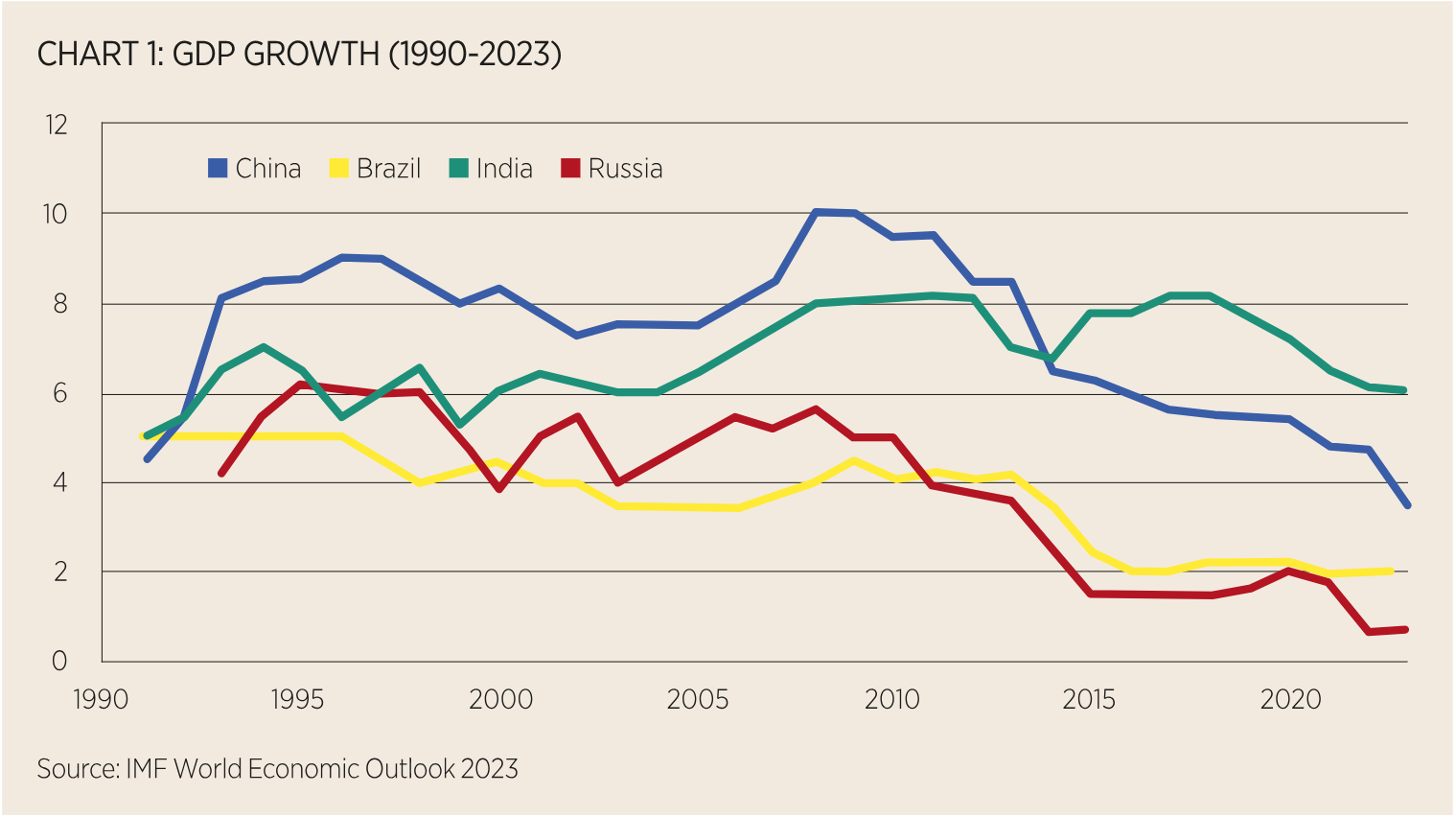

Among the former category, Vietnam and the Philippines are estimated to have a marginally higher growth rate. However, both countries with a much smaller base (in terms of economic, geographic and population sizes) than India. The expectation is that India will grow by 5.9% in FY 2023–24 and by an average rate of 6.1% over the next five years. This growth story isn’t necessarily a novelty. Long-time India watchers who aren’t “permabears” have long noted that India’s growth rate was second only to that of China among BRIC countries since the early nineties until around 2014 - when India’s growth rate skyrocketed to first place.

2014: A Turning Point

Morgan Stanley’s India Desk, in a study titled “How India Has Transformed in Less than a Decade” released to clients on May 29th of this year, highlighted ten factors that have been boosting growth. Chief among them are “Supply-side Policy Reforms” with two components:

A corporate tax rate that was already competitive against nearly every Advanced Asian and most Developing Asian economies is projected to be further liberalized for companies commencing manufacturing before 2024 ends

Infrastructure completion progress have been at all-time highs for the past eight years

Other factors include the fact that Indian companies are at 12-year lows in impaired loan ratios (with corporate debt expected to moderate down from 62% in 2014 to 50% of GDP by the end of the current year), digitalization of social spending easing transfers to beneficiaries while whittling down waste and losses due to fraud, flexible inflation targeting since 2014 which effectively decoupled the Federal Reserve’s rate hike cycle from that of the Reserve Bank of India (RBI), and strong multinational corporate sentiment leading to increasing share of exports.

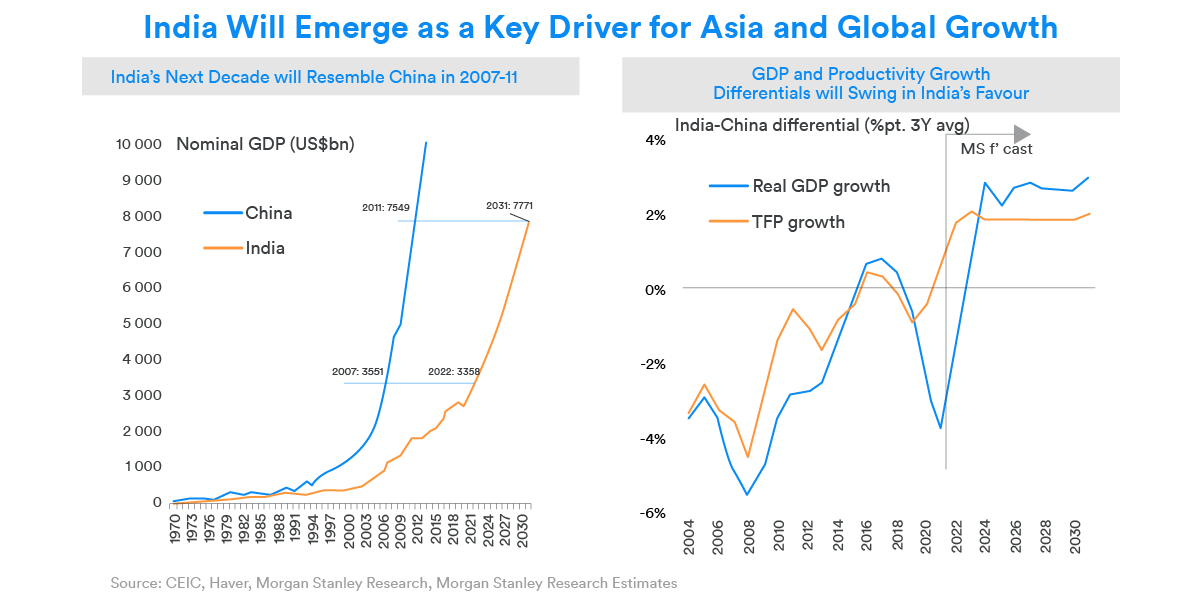

Morgan Stanley goes on to state that the decade to come will resemble that of China during the five years around the Global Financial Crisis (GFC), with GDP and Productivity differentials heavily in India’s favour.

Unlike China’s growth story - which was largely fueled by the benefits of exports having a leading action on domestic consumption - India’s manufacturing exports seem to be led by increasing domestic consumption trends, which is estimated to have a nearly 9.2% Compounded Annual Growth Rate (CAGR) over the next decade.

In parallel, credit growth is expected is expected to have a 17% CAGR over the next decade.

Overall, Morgan Stanley declares that “New India” will drive a fifth of global growth for the rest of this decade.

Almost a month prior to Morgan Stanley’s report, Deloitte noted some fairly substantial revisions in its forecasts regarding the Indian economy:

Deloitte also noted that while India’s GDP trajectory was impacted by restrictions necessitated by the global COVID pandemic in the more immediate term, the growth rate of growth is estimated to continue staying strong under both optimistic and pessimistic scenarios.

A “Tight” Equity Universe

As of the end of this past week, the Indian stock market’s total market capitalization has been comfortably been breaching all-time highs for some time now.

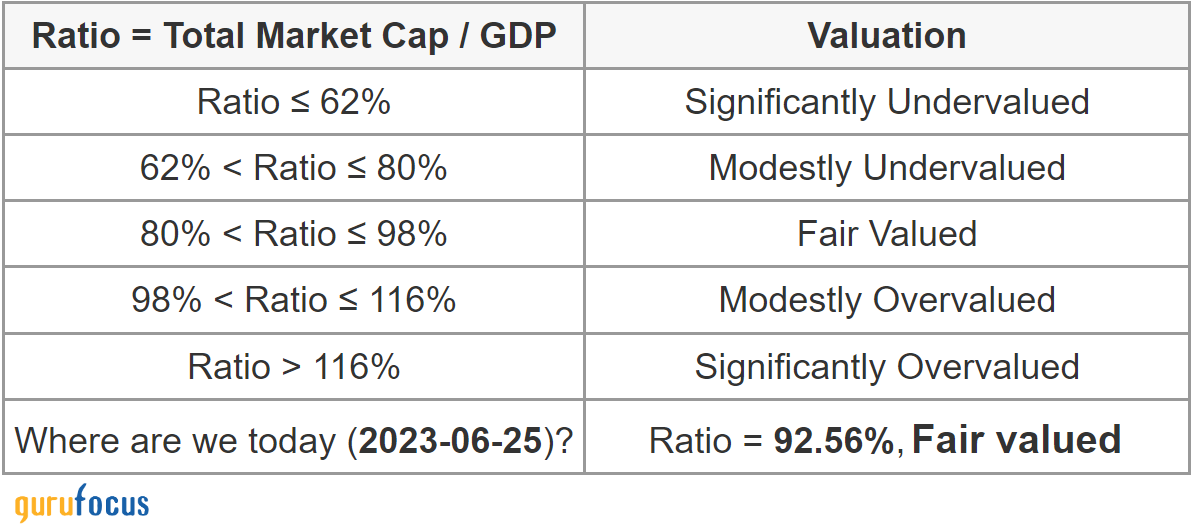

What’s quite interesting is how tight the relationship of the market has been with respect to the total GDP of the republic, both with or without the RBI’s assets factored in, over the past decade as well as the current one.

The market valuation zone diagram indicates that the Indian stock market is fairly valued in both the classical method:

as well as the modified method:

In terms of price performance, this market discipline remains evident. From 2018 till the present, the NIFTY 50 (Large Cap), MidCap 150 and SmallCap 250 indices show nearly identical convictions - with the MidCap inching forward and close to surpassing the performance of the NIFTY 50 benchmark.

In addition, the Price to Book (PB) Ratio for all three indices have been 3-5X range for this year - as compared to the nearly 10-11X for the Nasdaq-100 and 3-4X for the S&P 500.

Arguably, the most striking aspect of the Indian stock market has been its Price to Earnings (PE) Ratio discipline. The benchmark NIFTY 50 has mostly remained in the 20-26X range for most of this current century.

Excepts for dips during the GFC and other key points of the noughties as well as an earnings drop (while stock valuations remained high) during the course of the pandemic causing ratio inflation, the benchmark has displayed a particularly strong tendency for reversion back into this ratio range over the past eight years.

Opportunities Beyond Compliance Perils

Some portfolio managers contend that the Indian stock market is heavily “underweight”, i.e. it performs below its potential. A oft-cited cause is the massive web of regulations originally set up when post-Independence India was conceived to be developed as a command economy and subsequently built upon - leading to a massive “parallel” system fueled by graft. Earlier this year, the Indian government did away with a massive 39,000 points of regulatory compliance and 3,400 legal provisions to promote ease of doing business. In late 2021, it had done away with 22,000.

This somewhat explains the growing confidence in the MidCap and SmallCap segments - as these companies have the strongest inherent potential from increasing business ease. In May, Amundi Asset Management (a unit of Credit Agricole) estimated that capital expenditure (CapEx) outlays for a vast array of manufacturing indstries - ranging from batteries and food products to pharmaceuticals and semiconductors - will be massive and variegated in the years to come.

At the same time, the government is also working on developing the world's largest healthcare and housing systems for the underprivileged while making a massive push for renewable energy generation infrastructure. All in all, an ambitious, intricately-designed and well-balanced plan is in motion (or set of plans, given the massive scale).

On the 23rd of June, during Indian Prime Minister Narendra Modi’s address to a joint session of the U.S. Congress (which received 15 standing ovations and had to be stopped for an applause break 79 times), he said:

“When I first visited the U.S. as a Prime Minister, India was the 10th largest economy in the world. Tenth. Today, India is the 5th largest economy. And… India will be the 3rd largest economy soon. We’re not only growing bigger but we’re also growing faster. When India grows, the whole world grows.”

As far as the author knows, no Indian has ever aimed to just be 3rd.

There’s a lot more to be said about the sheer scale and ambition of a nation that knows all too well the perils of concentration risk. But more on that next time… soon.

As it turned out, the next few articles end up highlighting a common theme: a “New India”. Click here for a full overview of how the race for making a jet engine in India is shaping up in light of a big announcement by GE Aerospace. Next, click here to read about India’s burgeoning edge in the AI race that could propel the country into the Top 3 podium soon.

A deep dive on India is incomplete without a discussion of its millennia-spanning spiritual and philosophical roots which lent its hand in shaping an entire continent (and beyond). The 5-part “Dharma” series - with two additional parts specifically for Indonesia and Malaysia - does just that. Click here for the first part and read on.

An argument could be made that the East and West are delinking. In fact, such an argument has been made in the 3-part “Great Delink” series which goes deep into the actions of Chinese and Indian officialdom in securing their place in the future, just as they had in history. Click here for the first part and follow the trail. Finally, click here for a list of all articles published.