Market Outlook for Week of July 14 + Beverage Stocks

A roundup of media commentary proffered and featured around the world

Last Friday, I made a number of comments regarding the outlook for markets in the week to come especially with regard to Trump’s policies, gold, bitcoin, Musk vis-a-vis Tesla’s stock, and potential large movers. Some of them appeared on the 13th of July in two Tel Aviv-based publications: financial news publication Globes (which was also featured in the back page of their newspaper issued that day), and business news portal ICE (“Information Communication and Economics”). Also requested was commentary on the state of global beverage stocks. If/when published, I’ll link them in the section down below. Here is the full rationale behind the commentary I made. Read on!

Trump’s Protectionist Trade Policies and Impact on Markets

By considering the fact that tariffs are being levied on countries such as Brazil against whom the U.S. is running a trade surplus, the Trump administration seems to be aiming to promote domestic production of goods and commodities at all costs. For this to be effective, the U.S. dollar and the relative attractiveness of its bond market will need to continue to decline in order to make production cost-effective even with the current tariff regime.

Note #1: The origins and rationale behind Trump’s tariff war doctrine was extensively discussed early in April this year on the Leverage Shares website (and can also be found on SeekingAlpha). Since the publication, the fact pattern has largely remained consistent.

Foreign investor outflows from Treasuries — or at least a stilling of demand of thereof — is on the cards, along with the continued rising interest in European equities. Market breadth in U.S. equities can be expected to shrink, with only a handful of tech stocks continuing to carry the market on their backs.

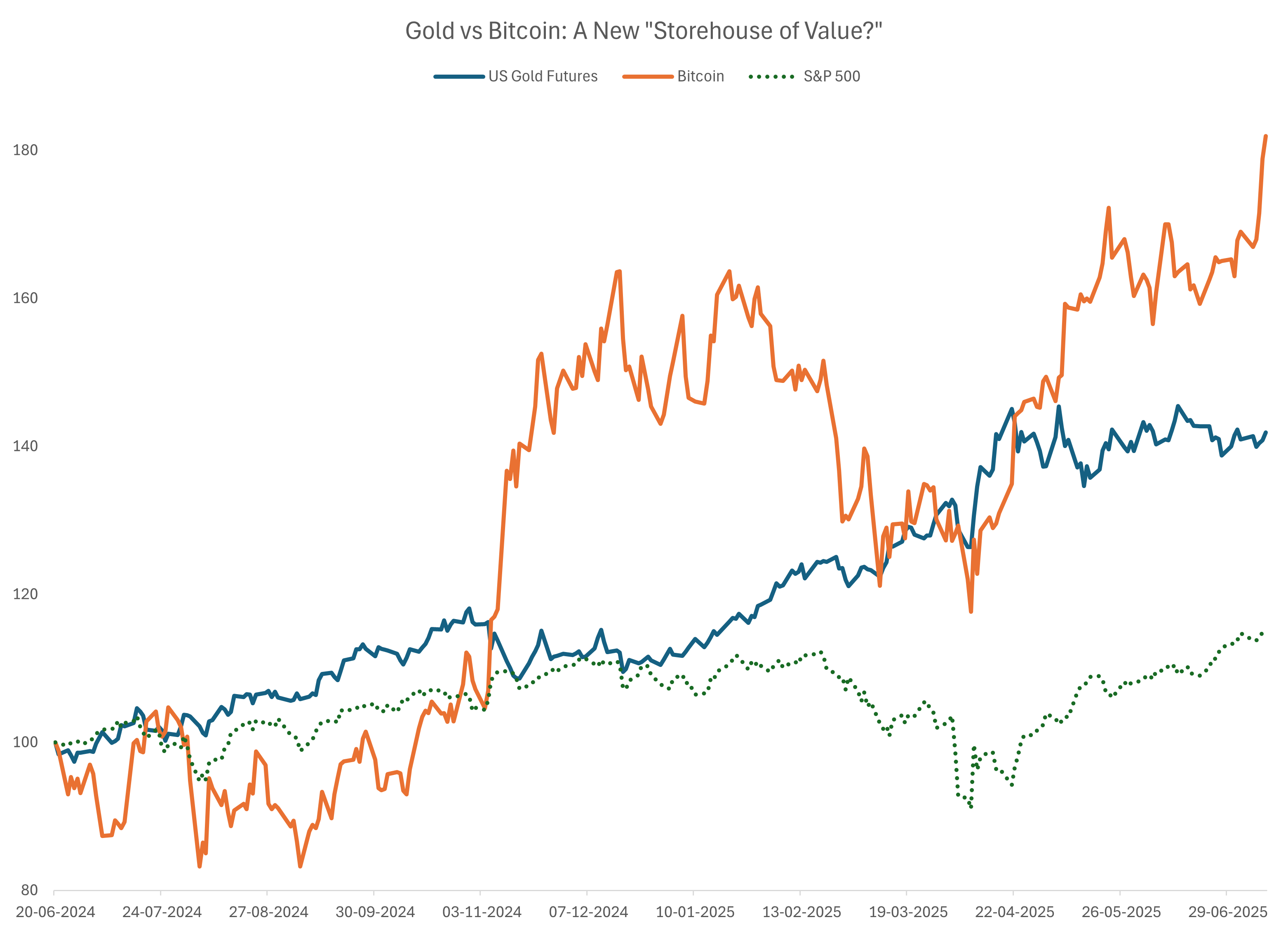

Gold Trends and Market Factors

With investors in the Western Hemisphere and China seeking safe harbour for at least a portion of their market wealth for well over a year now, gold had skyrocketed well in excess of the S&P 500 and the Nasdaq-100. Gold’s pricing is currently being tested and investors have been switching to the likes of silver, platinum and palladium instead – all of which have been spiking since May.

The meteoric rise of the latter two is cause for concern: both metals are extensively used in industrial processes and continue to be in increasing demand. Meanwhile, supplies are under strain due to ongoing sanctions against Russia. The pile-on by investors seeking an alternative to gold exacerbates the two metals' prices, with inevitable consequences for ordinary consumers when existing stockpiles run low.

Note #2: The factors behind platinum/palladium and the underlying implications for the forward outlook were discussed at length in a Substack article published in June this year.

It's unlikely that gold will break through to $3,400 in either spot or future markets and a slide back to $3,200 or even $3,100 can be expected by the end of the year. However, this might become a bonus for long-term holders: if gold becomes cheaper, “safe harbour” seekers might start to switch from silver, platinum and palladium back to gold and return it to the long-term bullish trend that it has always trudged. A drop in platinum and palladium, in turn, will bring some cheer to the automotive and chemical industries.

Bitcoin’s Short- to Medium Targets and Market Factors

Bitcoin is increasingly less correlated with the S&P 500 and speculative bursts seem to be tempered for now in favour of a steady rise. With current trends, Bitcoin could be piercing the $130,000 level by August and close out at the year with strong support at the $160,000-$180,000 level – regardless of fungibility issues with real-world transactions.

The key drivers for this have been two-fold. On the practical side is its steadily improving potential to be usable for tokenization of verification networks for real-world transactions. On the speculative side, it stands as a net beneficiary of gold’s rising levels being increasingly tested — leading to some investors switching to bitcoin as an alternative “storehouse of value”, which some bank analysts are positing as well.

Elon Musk’s Influence on Tesla’s Stock Performance

Tesla’s stock performance currently continues to carry a fair amount of optimism since Q2 deliveries were less worse than expected, its mostly-domestic ecosystem potentially translates to favourable tax benefits via the “One Big Beautiful Bill” for buyers of its products over most of the competition (barring Volkswagen and Hyundai/Kia) and early indicators of a sizeable price advantage of its in-development Robotaxi project versus that from the likes of Waymo.

However, the stock is significantly overvalued relative to its peers and that makes it susceptible to volatility, which Musk’s recent actions don’t help with. However, it bears noting that:

Musk’s gripes with the political system aren’t new, as the rise of Ross Perot – another tech tycoon – in the 1992 presidential election exemplifies. Voter disaffection has, in fact, been rising through most of the 21st century and had grown even stronger over the past two presidential elections. Numerous political outfits – such as the Working Families Party that had backed New York mayoral candidate Zohran Mamdani and the Democratic Socialists of America that had backed Representative Alexandra Ocasio-Cortez – a potential Senate contender – until 2024. In other words, “alternative” political outfits have largely been normalized.

The Grok controversy needs to be contextualized: like most LLMs (Large Language Models), the chatbot is trained with posts, comments, and images within X and other swaths of data collected from all over the internet. With the scaling back of content moderation on X in favour of freer expression – at least in the U.S. – the training data is bound to pick up some questionable ideations. This tendency can be fine-tuned with time and attention.

On its technical merits, Grok is increasingly being deemed as being strong by industry experts and has even earned praise from Sundar Pichai, the CEO of Microsoft, which has a fiercely competing product suite on offer. As it stands, the silent majority of investors find plenty of cause to be optimistic despite these issues.

Note #3: Tesla’s delivery numbers and Musk’s political foray was discussed extensively in an earlier article on Substack published earlier this month.

Major market events to be watched this week

The sinking of two vessels – the bulk carrier Seven Seas and the tanker Eternity C – in nearly as many days by the Houthis of Yemen along with a possibly symbolic single missile aimed at Ben Gurion Airport in Israel effectively dashes any hopes of calm in the Strait of Hormuz. The Houthis have remained a resilient adversary despite repeated strikes by both Israeli, British and American forces. Middle Eastern nations have found this to be true to their cost as well: from March 2016 till the cessation of open hostilities in April 2024, the Saudi-led coalition of nine countries from West Asia and North Africa had lost between around 2,000-7,000 soldiers — mostly Saudi and Sudanese — as well as a number of aviation assets (mostly F-16s) in the course of their military campaign in support of the Houthis’ political opponents.

While a nearly negligible volume of global container traffic pass through the strait, around a fifth of the world’s Liquified Natural Gas (LNG) and a fourth of the oceangoing oil supplies do. Insurance costs for Red Sea shipping have already doubled and shadows of the ruinous “tanker war” of the eighties – then waged between Iraq and Iran but with a massive impact on the logistics of uninvolved nations – loom large on Dubai Crude (“Fateh”) and Micro GME Oman Crude contracts. This will be a concern for the Far East – which has historically been prominent buyers – and inevitably lead to increased pressure on Brent unless additional supplies of Russian crude (“Urals”) is made available to the Far East. Shipping rates can also be expected to rise.

With both military action and retaliation inevitable, both oil and gas markets are particularly expected to be shaky in the week to come.

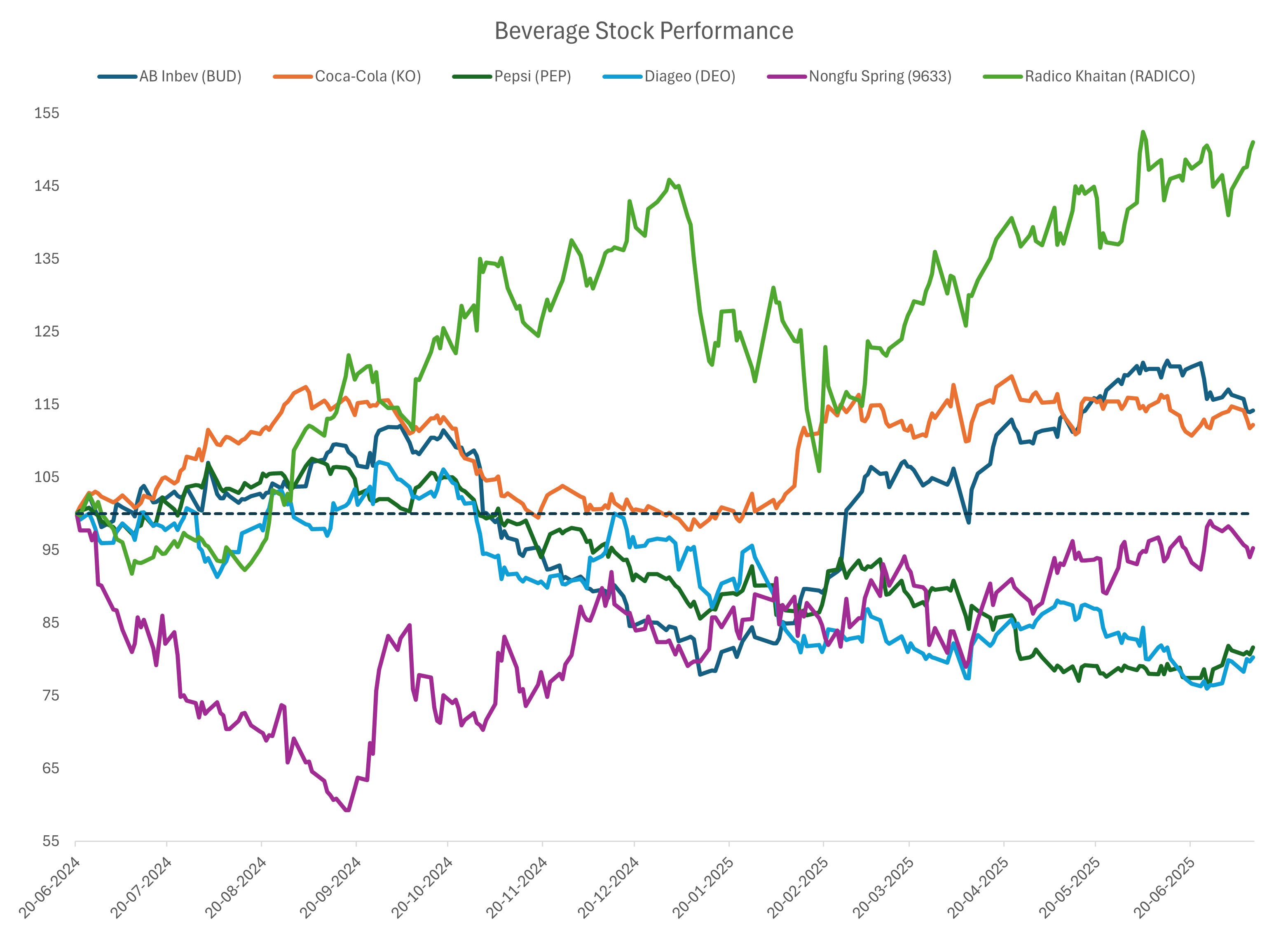

The Problem/Opportunity within Beverage Stocks

Beverage consumption is largely determined by brand equity established over years and decades. Over the course of the past few decades, there has been a large-scale consolidation of various brands from all over the world into a handful of publicly-traded stocks. This poses an interesting proposition: an investor can efficiently gain globally-diversified exposure to consumption trends within the Food & Beverage sector – and by proxy the hospitality sector. Achieving diversification is expensive and requires extensive study; the state of the beverage stocks space currently simplifies that.

The downside to global consolidation implies that the perception of a brand popular in a certain country can be diluted by management decisions made at corporate headquarters far away — thus imperiling consumption trends and stock value. This nuance is important and would require the investor to be vigilant. Another factor to pay attention to is M&A activity: if a number of brands offering similar products to the public in a certain region are being scooped up rapidly, this might imply that the sales strategies of the acquired brands are flailing. The whys and wherefores are important for an investor hoping to hold long-term exposure. An increasing number of consumers are decrying globalizations and switching out a beverage is a pretty simple proposition — given how crowded the space is around the world.

Among the leading (and most interesting) beverage stocks around the world, a number of intertwining themes are writ large. One overall theme to consider in beverage consumption worldwide is that a generational shift is afoot: alcohol consumption is on the decline among younger generations the world over. Another theme to consider is that non-alcoholic beverages are being scrutinized more closely by younger buyers for health reasons.

Coca-Cola (ticker: KO) has lately been downtrending on the back of lower case volumes being delivered on a quarter-on-quarter basis lately. This is largely on account of the second theme – young buyers are increasingly turning away from high-sugar beverages and other ingredients with health risks in favour of healthier alternatives. Coca-Cola has, in fact, made investments into new trends via investments fairlife milk (plant-based drinks) and BODYARMOR sports drinks. With the current downtrend in price, this might be an interesting point of time to buy in.

Another theme running through the Western Hemisphere has been inflation, which is also having an impact on consumption trends. Despite consumption declines, canned beer has been selling relatively better than the likes of whiskey, et al, and also has relatively lower production costs. Anheuser-Busch InBev (tickers: ABI/BUD) has done relatively well relative to Diageo (tickers: DGE/DEO), with the latter running negative in one-year performance.

The tendency for healthier consumption, however, is also predicated on spending behaviour. With over a year-long decline in spending over in China on account of economic headwinds, Nongfu Spring (ticker: 9633) has recently shown a sharp turn after a tenuous recovery trend since Q4 2024.

Diversification can take other forms too and one beverage company has achieved this in a rather interesting way. Radico Khaitan (ticker: RADICO) started out as a well-regarded regional distiller in India over 80 years ago and had since diversified into the production of industrial alcohol, PET bottle manufacturing for other beverage brands, and distribution of international liquors in India while developing a stable of liquors that have steadily been making inroads all over the world. This ticker’s performance has been explosive over the past year and is the clear champion among beverage stocks from all over the world.

For a list of all articles ever published on Substack, click here.