"500 Unicorns" in India's Fintech Revolution

E-commerce democratization in India lays the groundwork for massive upheaval in fintech and Big Tech's standing

Two companies that are rather prevalent in Indian e-commerce are both foreign owned: Amazon and Walmart-owned Flipkart. Of the two, Amazon is a rather unwieldy mess. In my article titled “Amazon Should Be Three Separate Stocks But It Won't Do That” written for SeekingAlpha in October 2021, the conclusion laid out was an e-commerce company that largely carried a cloud infrastructure company has gone on to become a cloud infrastructure company that is carrying an e-commerce company and a media company, with the latter having a particularly nebulous relationship in showcasing its revenue potential.

Being a “tech” company also meant that Amazon’s corporate bonds can have a lower rate but still be in demand (unlike the higher cost incident upon, say, a media company). Meanwhile, by being such a massive (messy) company, a large proportion of the company’s stock is held by institutional investors — predominantly ETF issuers — thus insulating the management from reform-demanding activist investors. This protection is readily apparent: around Q3 2021, activist investors led a call for large conglomerates to break up into separate stocks so that investors can see each value propositions more clearly. Some caved, some did not. Amazon was one of the latter.

Another article on SeekingAlpha in December of that same year titled “Amazon And Walmart Face Problems With Their India E-Commerce Businesses” highlighted a host of other issues in India with Amazon, in particular, being the worst offender. Problems included: Amazon programmatically pricing the products of a partially-owned merchant lower than its competitor and providing it free/discounted shipping, using legal shenanigans under dubious means to hold off the formation of a rising challenger through a Reliance-Futures Retail merger, a number of regulatory scandals (not least helped by a whistleblower revealing Amazon India executives having a protocol to enable the disposal of financial documents if raided by tax authorities), and so forth.

Flipkart too had the “partially-owned merchant” problem until its sale to Walmart. However, what’s evident in the examination of the financial trends in both companies’ businesses in India had been that it has brought virtually no benefits. In fact, taking forward the financial metrics in the December article into the most recent Financial Year for which data is available, it can be seen that the situation isn’t very different in the present.

Over the past seven full Financial Years alone, both companies have lost billions of dollars in India — with Amazon being the worse for wear. Outside of legal fees from shenanigans of their own doing, this is due to the business model they inhabit. E-commerce companies act as “aggregators”, i.e. they negotiate a deal between the buyer and the seller and manage everything in between such as warehousing and logistics. Of course, this deal-making isn’t free for the seller: on an aggregated basis, it is expected that the seller side of the ecosystem will eventually recompense the deal-maker for the costs incurred and participate in market-building activities via discounts to propel volumes that will rationalize costs.

Given that granular and last-mile delivery can be expensive loss-making propositions, an essential part of market-building would be to eliminate/supplant the offline store as a shopping destination of choice. While this could be considered a fait accompli in most well-populated parts of the Western Hemisphere, the prospect of retail depopulation is reflexively not palatable in the Eastern Hemisphere - particularly India with its vast tapestry of “kiranas” (neighbourhood stores) and dealer networks. While it could be argued that the latter imposes extraneous costs on the buyer, it also generates employment for millions. No business model changes on its own volition. Thus, while the current model of “Big E-Commerce” would prefer this system gone or reduced, an evolution would have to be forced to compel change in both.

Enter the Open Network for Digital Commerce (ONDC)

“Make E-Commerce Irrelevant” (Again)

The ONDC has a circuitous origin. Initiated by the Department for Promotion of Industry and Internal Trade within India’s Ministry of Commerce and Industry, it was incorporated at the end of 2022 and seeded by a pubic-private association of quality standards called the Quality Council of India as well as an e-governance promotion company spun out of NSDL, India’s largest central securities depository. Since then, it has been seeded with millions of dollars in capital (in exchange for stake) by India’s leading banks — both state-owned and private-sector — as well as the Reserve Bank of India’s national payments settlements subsidiary and the National Stock Exchange of India.

This entity (for lack of a better term) went on to champion the “Beckn protocol” (the fruits of an open-source collective organized a non-profit company in Bengaluru), an interoperable protocol designed to de-centralize digital commerce by dismantling each phase of the commercial transaction into individual sub-environments.

In barebones terms, “buyer” apps provide the buyer with a variety of choices available on “seller” apps such that the the buyer can make a choice after considering logistics and other requirements through other apps. The protocol demands a level of standardization in the interfacing of these apps so that any number of buyers and sellers — representing both along all walks of life — can be onboarded with maximized choice and opportunity for buyer and seller respectively.

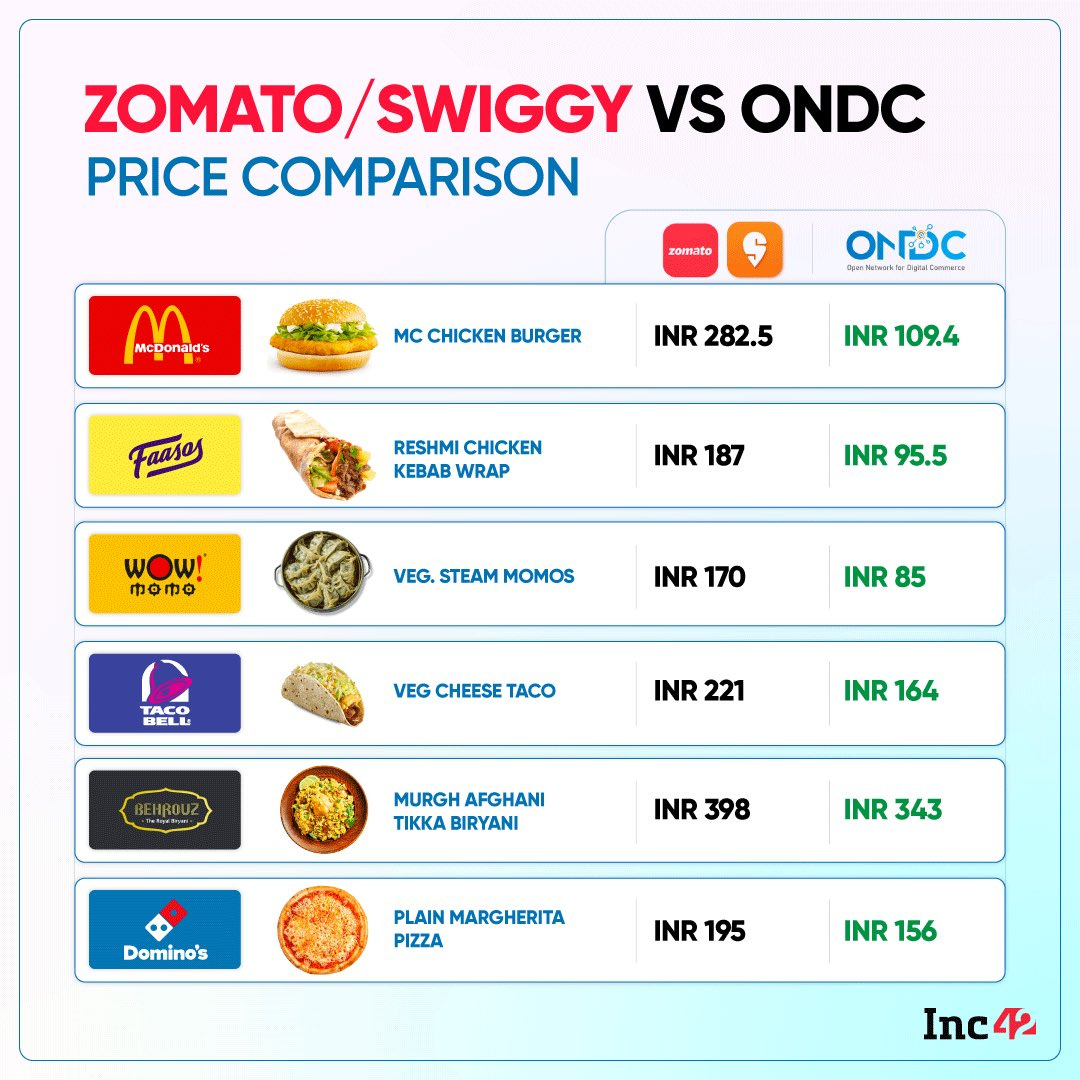

With a small selection of apps, pilot testing was initiated on the 29th of April 2022 in five cities: New Delhi, Bengaluru, Bhopal, Shillong and Coimbatore. By January, the testing phase had expanded to 85 cities. Conversation around initial results, while encouraging, have tended to leave the public misinformed. For instance, this viral comparison between popular food delivery apps Zomato and Swiggy versus ONDC results in Chennai seemed to show a massive price differential:

However, the price of logistics adds context for the price on the ONDC column. Given that food delivery apps charge around 18-24% of the order’s cost on the restaurant, many of the restaurants on ONDC offered free delivery since that worked out cheaper than paying the food delivery apps. Ordinarily, buyer matching and delivery costs can be expected to be around 8% of the order value on ONDC. Logistics is a significant bottleneck for the system: it takes time and strong participation to populate all locations with delivery partners and effectively rationalize costs.

By March, however, a number of Logistics Network Partners (LNPs) had joined the fray as part of a significant rush into ONDC that saw, for example, venture capital firms pushing their portfolio firms into the ecosystem as well.

In March, ONDC’s infrastructure was employed to develop “Namma Yatri”, a ride-hailing app focused on India’s ubiquitous 3-wheeled autorickshaw taxis with virtually marketing costs being impressed upon the riders. By April, 31,000 merchants selling 3.7 million products were in the network and an average of 20,000 rides were being booked on “Namma Yatri” in its two test cities. Since ONDC is a Section 8 non-profit, any and all fees levied on sellers would be used for the maintenance and development of the network.

As of May, ONDC is continuing with expanded tests in 236 cities in India, while averaging around 13,000+ delivery orders per week and 36,000+ rides per day. As per a compilation of ONDC promoters’ responses by venture capital firm Antler, this decentralized network is making e-commerce visible in Tier 2/3 cities where growth is low for Big E-Commerce and demand is niche, shall cross 900 million buyers over the next five years, over $100 billion in commerce can be expected to happen and is already resolving nearly 1 million disputes per month. In June, ONDC launched a B2B network, with some startups immediately onboarding on to it.

In an interview dated September 2022, ONDC’s CEO Thampy Koshy was unperturbed over the fact that Amazon and Flipkart had (at the time) not engaged with the network. “In the future, anybody who has got anything to sell—products or services—will make their catalogues visible in this common network (ONDC), either by themselves or through a third-party aggregator or a technology service provider”, he said. “Ecommerce (as it is practised now) will become irrelevant.”

In February this year, Amazon announced that it will be joining ONDC — where seller costs are one-fourth that of what they and rival Flipkart charge. On the 28th of June, Google Cloud announced an accelerator programme for ONDC by releasing an open-source implementation of the ONDC infrastructure and core API to foster scalability and enhance security. Additionally, developers working on connectivity with ONDC will be given access to Retail Search and Discovery AI to elevate both buyer and seller experiences on the network.

Valuation Models Glitch in India

Overseas private equity/venture capital interest has tended to focus heavily on India’s burgeoning fintech sector. After all, with a long history of successful valuations and placements in the rest of the world, similarly-styled ventures in India can be valued in similar vein after adjusting for India’s massive population and consumer trends.

As a result, it’s being estimated now that a number of fintech majors — chief among them Walmart-owned PhonePe — might be overvalued.

The Indian government has long been interested in a high adoption rate of digital payments by citizens. Towards this end, the Reserve Bank of India (RBI) funded the development of the United Payments Interface (UPI), which connects the country’s banks and financial institutions (along with the likes of Google Pay) together so that users can transfer cash among themselves within seconds. To further this, RBI even oversaw the development of a single app called BHIM that users can download and configure to link with their bank accounts.

In this environment where all barriers to entry by financial institutions both big and small have been reduced or altogether eradicated, analysts should have questioned what the unique selling point inherent in PayTM — or indeed most other fintechs — would be. The answer would have been either “none” or “a low differentiator requiring further work”.

However, analysts set PayTM’s IPO price at ₹ 2,150, which PayTM has never achieved since it listed.

“Wall Street” analysts couldn’t even model the landscape which PayTM operates in and the very low orders of differentiation between it and existing legacy systems/similar competitors while Dalal Street's street-smart traders ate the former's lunch by utterly rejecting the proposed valuation. Wall Street houses' analysts often bemoan that the Indian equity market is “too conservative” but the fact is Dalal Street has come a long way in the past 30+ years; it simply doesn’t need Wall Street’s playbook on its turf.

That wasn't even the last time Dalal Street got one over Wall Street in that year: on the 21st of December 2021, CE InfoSystems (better known as “MapMyIndia”) had a listing debut on the Indian bourses with a 53% premium over issue price and was oversubscribed by 154.7 times the number of shares. Institutional houses allegedly started panic-selling the very next day, which didn't fool Dalal Street: they correctly read the positive fundamentals of a debt-free and heavily specialized company that's been around for nearly a quarter-century. As a result, traders and retail investors bought up premium-value shares at a discount.

These two incidents, among others, should indicate that there seems to be a massive knowledge gap in Wall Street when it comes to the East’s equity markets — particularly India. Not understanding India’s unique landscape and modelling for it would lead to ruin more and more often.

Blue Sky Thinking?

Given the heavy tilt afforded to flattening barriers to favour innovation and foster adoption, there is plenty of cause to assert that “classical” methods of valuation favoured by Silicon Valley investors and Wall Street houses don’t really work in the environment being fostered in “New India”. A fair bit of “Blue Sky” thinking would be be in order.

At a conference held at Stanford University in September 2022, India’s Commerce Minister Piyush Goyal was asked how could India ever hope to stand up to Big Tech and the potential they bring in. He replied that instead of one or two players becoming trillion dollar companies, ONDC will bring about a fintech revolution that will enable 500 small companies to become unicorns. If Wall Street and Silicon Valley found such an assertion a little tough to chew on at the time, it should be a proposition that should be somewhat easier to swallow now.

This article is effectively a coda to the “New India” theme explored in the past few articles. Click here to read more on overall macroeconomic trends that point to the coming few years becoming “New India’s” decade. Next, in light of a big announcement by GE Aerospace, click here for a full overview of how the race for making a jet engine in India is shaping up. After that, click here to to read about India’s burgeoning edge in the AI race that could propel the country into the Top 3 podium soon.

In other India-relevant articles, the 5-part “Dharma” series - with two additional parts specifically for Indonesia and Malaysia - traces the spiritual history of the East and its indelible roots in India. Click here for the first part and read on. Finally, click here for a list of all articles published.